Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:CNS

Need To Know: This Analyst Just Made A Substantial Cut To Their Cohen & Steers, Inc. (NYSE:CNS) Estimates

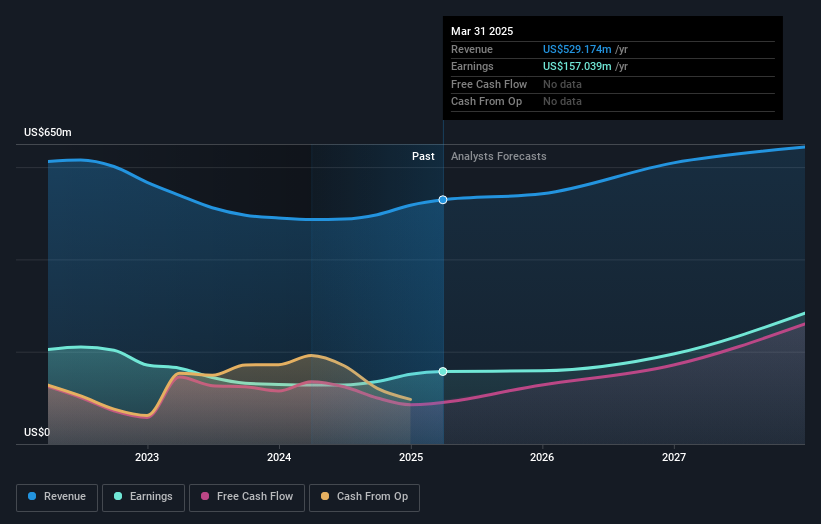

One thing we could say about the covering analyst on Cohen & Steers, Inc. (NYSE:CNS) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analyst has soured majorly on the business.

Following the downgrade, the current consensus from Cohen & Steers' sole analyst is for revenues of US$542m in 2025 which - if met - would reflect an okay 2.4% increase on its sales over the past 12 months. Statutory earnings per share are forecast to be US$3.13, approximately in line with the last 12 months. Previously, the analyst had been modelling revenues of US$608m and earnings per share (EPS) of US$3.88 in 2025. It looks like analyst sentiment has declined substantially, with a substantial drop in revenue estimates and a considerable drop in earnings per share numbers as well.

View our latest analysis for Cohen & Steers

The analyst made no major changes to their price target of US$81.00, suggesting the downgrades are not expected to have a long-term impact on Cohen & Steers' valuation.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's clear from the latest estimates that Cohen & Steers' rate of growth is expected to accelerate meaningfully, with the forecast 3.3% annualised revenue growth to the end of 2025 noticeably faster than its historical growth of 2.7% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 5.2% per year. So it's clear that despite the acceleration in growth, Cohen & Steers is expected to grow meaningfully slower than the industry average.

The Bottom Line

The biggest issue in the new estimates is that the analyst has reduced their earnings per share estimates, suggesting business headwinds lay ahead for Cohen & Steers. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. We're also surprised to see that the price target went unchanged. Still, deteriorating business conditions (assuming accurate forecasts!) can be a leading indicator for the stock price, so we wouldn't blame investors for being more cautious on Cohen & Steers after the downgrade.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Cohen & Steers going out as far as 2027, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks with high insider ownership.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:CNS

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor