Bank of New York Mellon (BK) shares have seen noticeable movement over the past month, gaining roughly 4% and building on a strong performance so far this year. Investors are weighing the bank’s solid revenue and net income growth trends.

Bank of New York Mellon's share price has climbed about 43% so far this year, reflecting solid momentum as investors take note of the bank’s execution and consistent earnings growth. Its 1-year total shareholder return of 44% and a striking 3-year total return above 170% show that long-term holders have been well rewarded recently. The short-term trend continues to point upward for now.

The big question now is whether Bank of New York Mellon's rapid gains mean its shares still trade at a discount or if investors have already priced in all the company's future growth prospects. Is there a real buying opportunity left?

Advertisement

Most Popular Narrative: 6.5% Undervalued

Compared to its last close at $110.48, the narrative projects Bank of New York Mellon's fair value at $118.10, suggesting the share price could still move higher if all their assumptions play out.

Accelerated investment in digital platforms (including digital asset custody, AI integration, and the NEXEN ecosystem), coupled with strong early adoption, positions BNY Mellon for improved operating leverage and net margin expansion over the coming years. Scalable technology reduces costs and increases cross-selling opportunities.

Curious what’s driving this bullish target? The linchpin is a forecast of enhanced margins and big leaps in digital operations. Find out how fresh innovation, changing earnings dynamics, and aggressive long-term bets underpin a fair value that stands well above today’s market price. Unlock the full story behind these projections.

However, sustained client outflows or unexpected market downturns could quickly challenge BNY Mellon's current growth trajectory and put pressure on long-term earnings momentum.

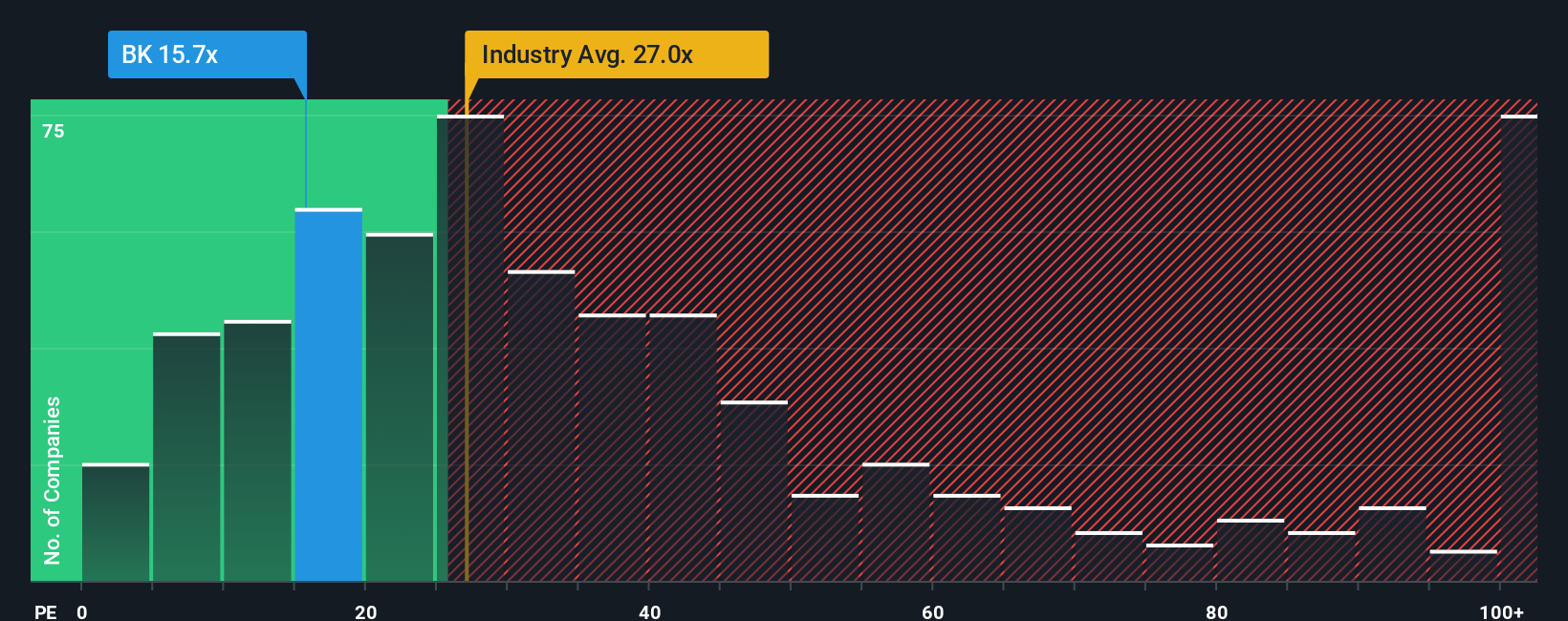

While the latest narrative targets a fair value above today’s price, a quick check of Bank of New York Mellon's current P/E ratio tells its own story. At 15.4x, it stands well below both the peer average of 27.4x and the US industry at 24.4x. The fair ratio, estimated at 16.2x, offers yet another benchmark close to the current level. This sizable gap hints at potential undervaluation, but market sentiment could shift quickly. Has all the opportunity been captured, or does the discount remain?

If you’re keen to dig deeper and put your own perspective to the test, you can easily build your own narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding Bank of New York Mellon.

Looking for more investment ideas?

Smart investors never stand still. Those who act quickly can secure exciting opportunities before the crowd catches on, and the right screener on Simply Wall Street makes it easy.

Stay ahead of financial innovation with these 82 cryptocurrency and blockchain stocks; see which public companies are accelerating blockchain technology and shaping the future of digital finance.

Tap into tomorrow’s breakthroughs by investigating these 32 healthcare AI stocks, featuring innovators fusing artificial intelligence with healthcare for game-changing growth prospects.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bank of New York Mellon might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.