Bank of New York Mellon (BK) has seen its share price fluctuate over the past month, with a recent slight dip. Investors may be watching the underlying trends to get a sense of where the stock could head next.

Zooming out, Bank of New York Mellon's share price momentum has eased a bit recently, but the stock’s overall trend remains positive. Its 38% year-to-date share price return speaks to revived confidence. Meanwhile, the 44% total shareholder return over the past year makes it a standout among peers, as investors factor in both capital gains and dividends.

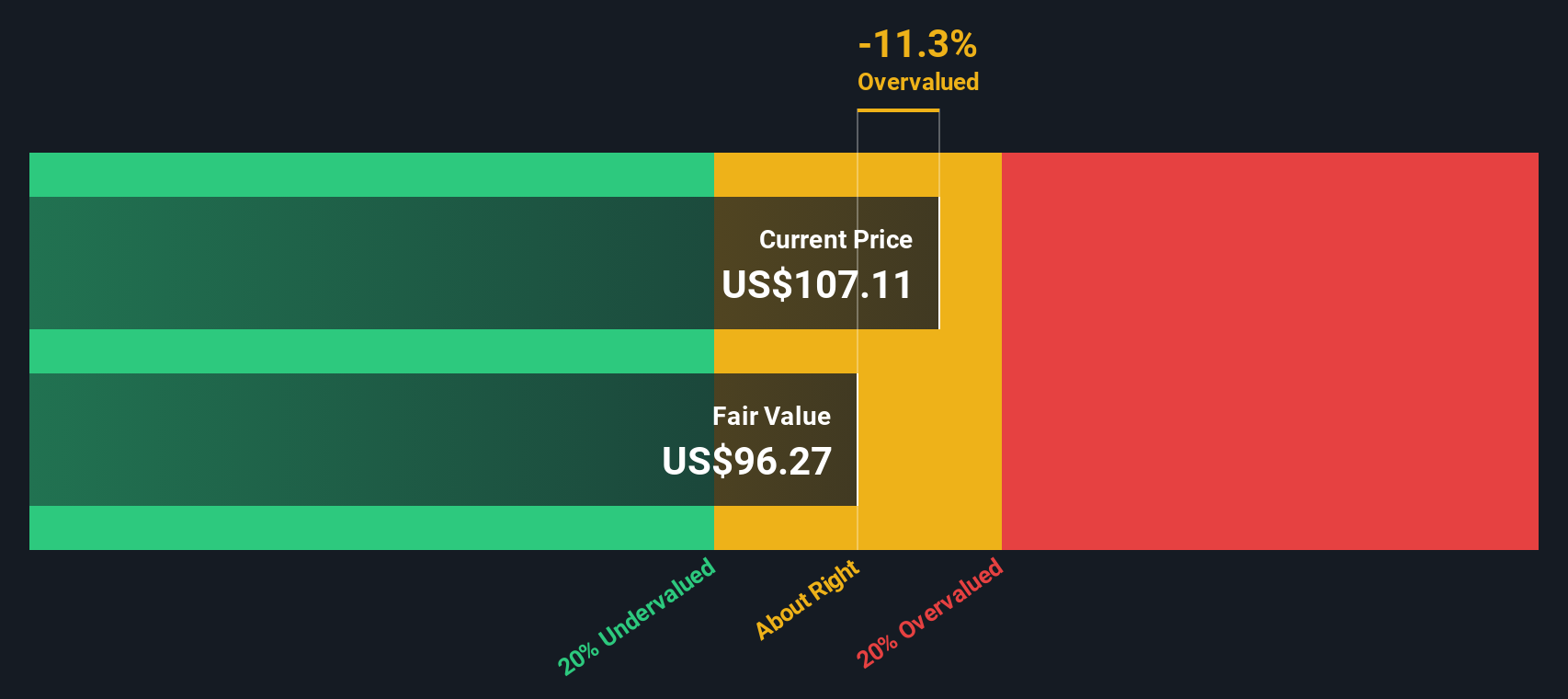

The big question for investors now is whether Bank of New York Mellon’s strong run leaves the stock undervalued, or if the current price already reflects all the expected growth ahead. This could make future returns harder to capture.

Advertisement

Most Popular Narrative: 9.3% Undervalued

With Bank of New York Mellon's fair value narrative at $118.07 per share versus a last close of $107.05, the market’s pricing falls behind the narrative's growth expectations. This forms the basis for a bold and forward-looking storyline.

Accelerated investment in digital platforms (including digital asset custody, AI integration, and the NEXEN ecosystem), combined with strong early adoption, positions BNY Mellon for improved operating leverage and net margin expansion over the coming years. Scalable technology is expected to reduce costs and increase cross-selling opportunities.

What fuels this higher fair value? The narrative points to a future shaped by advanced tech efficiency, margin expansion, and ambitious profit opportunities. The specific combination of growth drivers and analyst assumptions behind this price target may surprise you. Get the full breakdown inside the complete narrative.

However, a downturn in global markets or slower adoption of digital assets could quickly undermine these upbeat projections and reshape BNY Mellon's outlook.

Looking at Bank of New York Mellon through the lens of our DCF model, the numbers tell a slightly different story. Based on future cash flow projections, the SWS DCF estimate puts the fair value below the current share price. This suggests the market might already be factoring in most of the company’s upside. Which scenario do you find more convincing?

If you have a different perspective or want to dig deeper into the data yourself, you can easily develop your own narrative in just a few minutes. Do it your way.

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding Bank of New York Mellon.

Looking for more investment ideas?

Great investing means always staying one step ahead. Don’t wait to find out what you could be missing. Take action and see what other opportunities are out there.

Spot promising up-and-comers with potential by checking out these 3584 penny stocks with strong financials. These companies are shaking up their industries and attracting fresh investor interest.

Tap into the artificial intelligence wave by reviewing these 26 AI penny stocks. This list features businesses innovating faster than the market can keep up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bank of New York Mellon might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.