Advertisement

- United States

- /

- Capital Markets

- /

- NasdaqGS:HLNE

Assessing Hamilton Lane’s Value After a 35% Drop and Growing Private Market Interest

Simply Wall St

Reviewed by Bailey Pemberton

- Curious if Hamilton Lane is a hidden gem or an overhyped play? Here is a breakdown of what is really driving its current value and where the numbers may be pointing.

- The stock has seen some major swings lately, with a sharp drop of 35.4% over the past year. It is up nearly 93% in five years, which shows both its volatility and long-term potential.

- Markets have been reacting to shifting investor sentiment around alternative asset managers and changes in the macroeconomic backdrop, especially as private market allocations gain more attention. Recent headlines about fund flows and growing institutional interest in private assets have been especially relevant for Hamilton Lane’s positioning in the industry.

- According to our valuation checks, Hamilton Lane scores just 1 out of 6 for being undervalued. This is a figure to keep in mind as we review both the traditional metrics and, later on, a smarter method that could change how you see stock value altogether.

Hamilton Lane scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Hamilton Lane Excess Returns Analysis

The Excess Returns model evaluates a company by measuring how efficiently it generates profits from its shareholders’ equity, after accounting for its cost of capital. This method focuses on whether the business earns returns above what investors require, providing insight beyond simple earnings metrics.

For Hamilton Lane, the key Excess Returns metrics highlight strong historical profitability. The company’s Book Value per share is $18.78. Stable Earnings Per Share (EPS), based on the median return on equity from the past five years, is $3.84. With a Cost of Equity at $1.06 per share, the Excess Return is $2.78 per share. Hamilton Lane’s average Return on Equity is 29.64%. Its Stable Book Value, using the five-year median number, is $12.95.

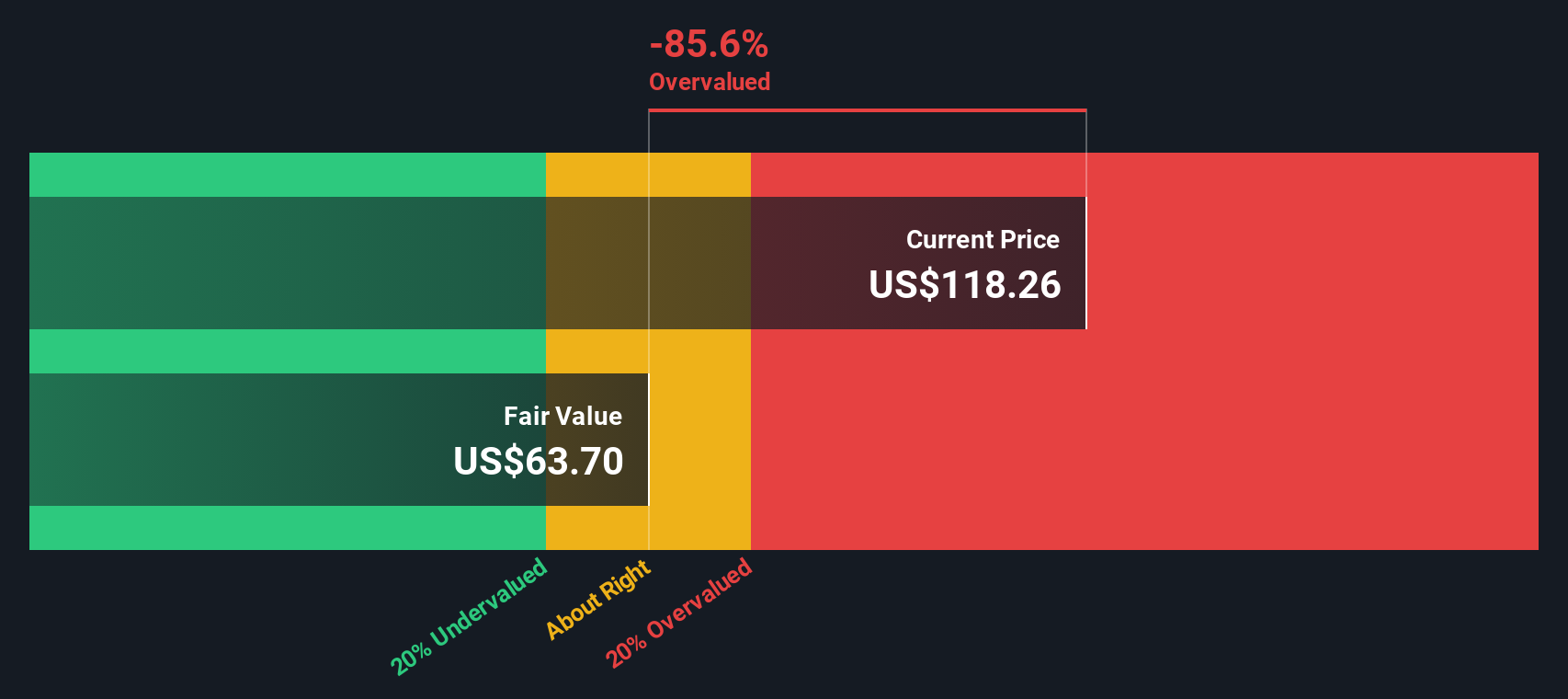

Despite these profitability figures, the Excess Returns model estimates Hamilton Lane’s intrinsic value is significantly below its current share price. This implies the stock is 76.7% overvalued based on this methodology.

Result: OVERVALUED

Our Excess Returns analysis suggests Hamilton Lane may be overvalued by 76.7%. Discover 927 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Hamilton Lane Price vs Earnings

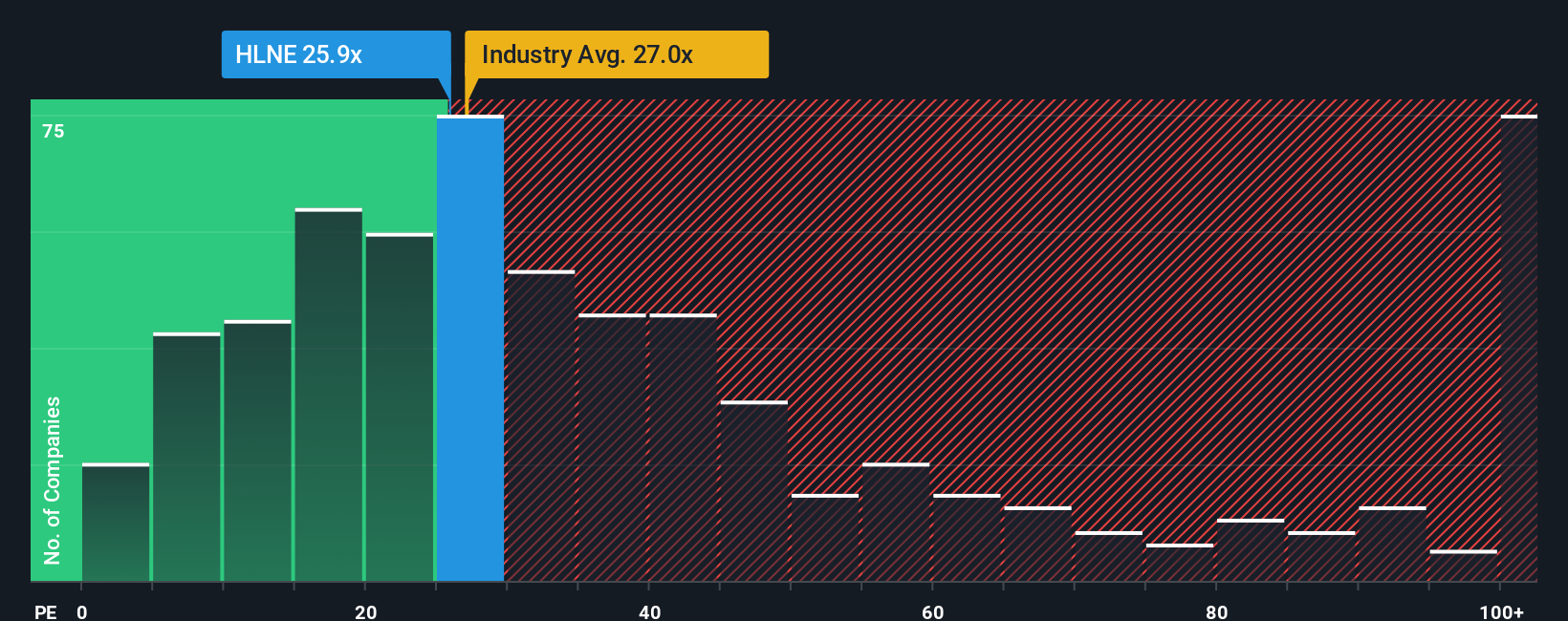

For a profitable company like Hamilton Lane, the Price-to-Earnings (PE) ratio is an effective way to gauge whether the stock’s current valuation makes sense. The PE ratio is widely used because it connects a company’s share price to its earnings, offering a straightforward look at how much investors are willing to pay for each dollar of profit.

What counts as a fair PE ratio largely depends on the company’s expected growth and risk levels. Companies with strong growth prospects or lower risk profiles usually deserve higher multiples, while those with more uncertainty or slower growth are typically valued at lower ratios. For Hamilton Lane, the current PE ratio stands at 23.6x. This is in line with the Capital Markets industry average of 23.5x, but noticeably above the peer average of 12.6x. At first glance, this could make the stock look expensive compared to similar firms. However, there are more factors to consider.

Simply Wall St’s proprietary "Fair Ratio" goes further than simple comparisons with peers or industry averages by factoring in the company’s unique mix of growth potential, risk, profit margins, industry conditions, and market cap. This holistic view gives a more tailored benchmark for what Hamilton Lane’s PE ratio should be and avoids the pitfalls of a one-size-fits-all comparison.

Since the Fair Ratio is unavailable in this case, we rely on the PE, industry, and peer context. Hamilton Lane’s current PE suggests its valuation is a bit stretched compared to peers but on par with its broader industry.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1433 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Hamilton Lane Narrative

Earlier, we mentioned there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal investment story for a company. It captures your beliefs about its future, including assumptions like growth rates, profit margins, and what you think it is truly worth.

These Narratives help you tie together a company's story, your own forecasts, and an estimate of fair value, giving you a powerful decision-making tool. They are available for free on Simply Wall St’s Community page, where millions of investors share and update their perspectives.

By comparing the Fair Value you set in your Narrative to the current price, you get an immediate sense of whether you think Hamilton Lane is a buy, hold, or sell. As new data or news arrives, Narratives update automatically so you stay current.

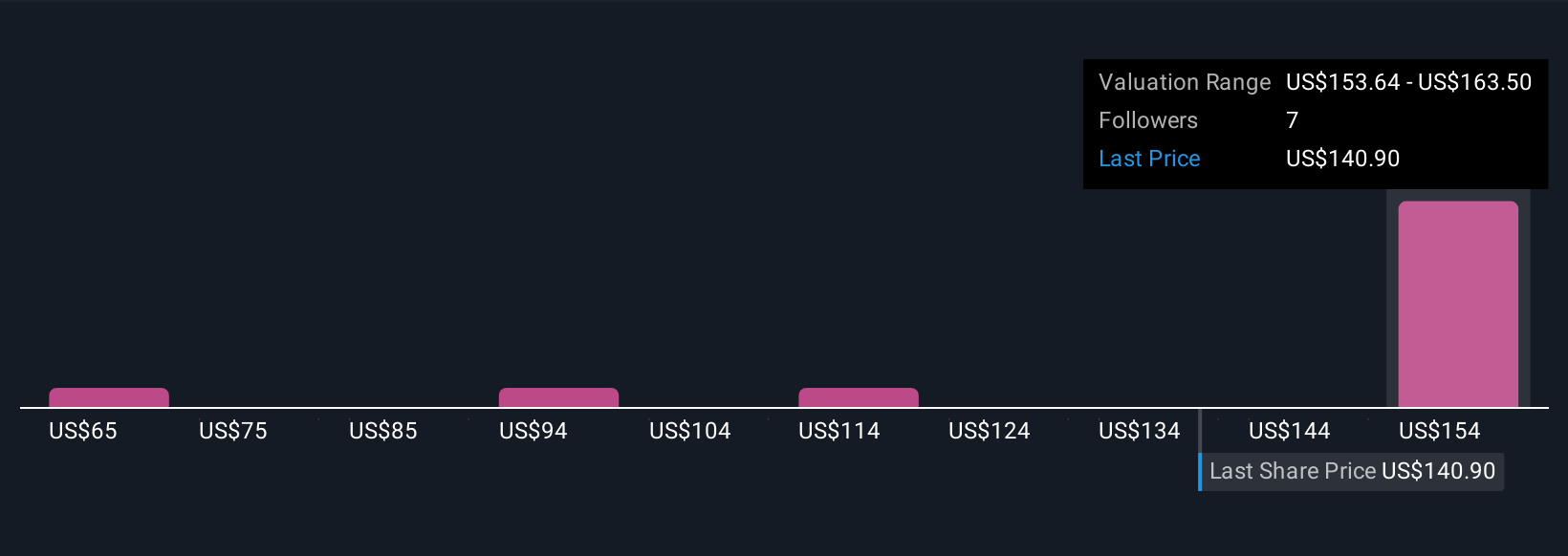

For example, some investors build bullish Narratives around Hamilton Lane’s rapid expansion in evergreen and global funds, projecting high revenue and margin growth with a fair value near $160. Others, focused on regulatory risks or rising competition, use lower estimates and calculate a fair value closer to $120 based on more modest assumptions.

Do you think there's more to the story for Hamilton Lane? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hamilton Lane might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HLNE

Hamilton Lane

A private equity and venture capital firm specializing in early venture, emerging growth, turnaround, middle market, mature, mid-venture, bridge, buyout, distressed/vulture, loan, mezzanine in growth capital companies.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

77 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative