Advertisement

- United States

- /

- Diversified Financial

- /

- NasdaqGS:DLO

DLocal (NASDAQ:DLO) Valuation in Focus as Investors Spotlight Growth and Scale Potential

Simply Wall St

Reviewed by Simply Wall St

Recent commentary around DLocal (NASDAQ:DLO) highlights its status as a favored small-cap pick among retail investors. This attention is driven by expanding payment volumes, strong management, and a large, growing addressable market. While growth continues, profitability remains under scrutiny as costs have increased with investments in scale.

See our latest analysis for DLocal.

DLocal’s share price has demonstrated solid momentum this year, with a 15% return year-to-date and a total shareholder return of 23% over the past twelve months. While the latest payment volume growth and attention from investors have helped fuel interest, the market remains focused on whether the company’s investment in scale can translate to sustainable profitability and further gains for long-term holders.

If you’re inspired by DLocal's resilience and investor buzz, this could be the perfect time to broaden your search and discover fast growing stocks with high insider ownership

But with shares already up this year and trading at a discount to analyst price targets, the real question is whether DLocal is still undervalued or if the market has already priced in its future growth potential. Is there still a buying opportunity?

Most Popular Narrative: 93% Undervalued

With DLocal’s last close at $13.44 and a narrative fair value positioned dramatically higher, expectations are rising for a meaningful re-rating if bold growth assumptions materialize.

The company’s core moat derives from deep integration with local payment methods in emerging markets, especially in Latin America, Africa, and Asia. Regulatory expertise and on-the-ground relationships are difficult to replicate for new entrants. The company also has the ability to serve both pay-in and pay-out transactions for global merchants, creating high switching costs for enterprise customers.

What is fueling such a significant valuation gap? The answer lies in ambitious projections about revenue growth, margins, and the type of profit multiples typically associated with a market leader. Interested in the key financial assumptions driving this notable fair value? Explore the narrative and review the numbers directly.

Result: Fair Value of $195.39 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, delays in launching new products or issues with third-party technology partners could challenge DLocal’s ambitious growth narrative.

Find out about the key risks to this DLocal narrative.

Another View: What Do Market Multiples Say?

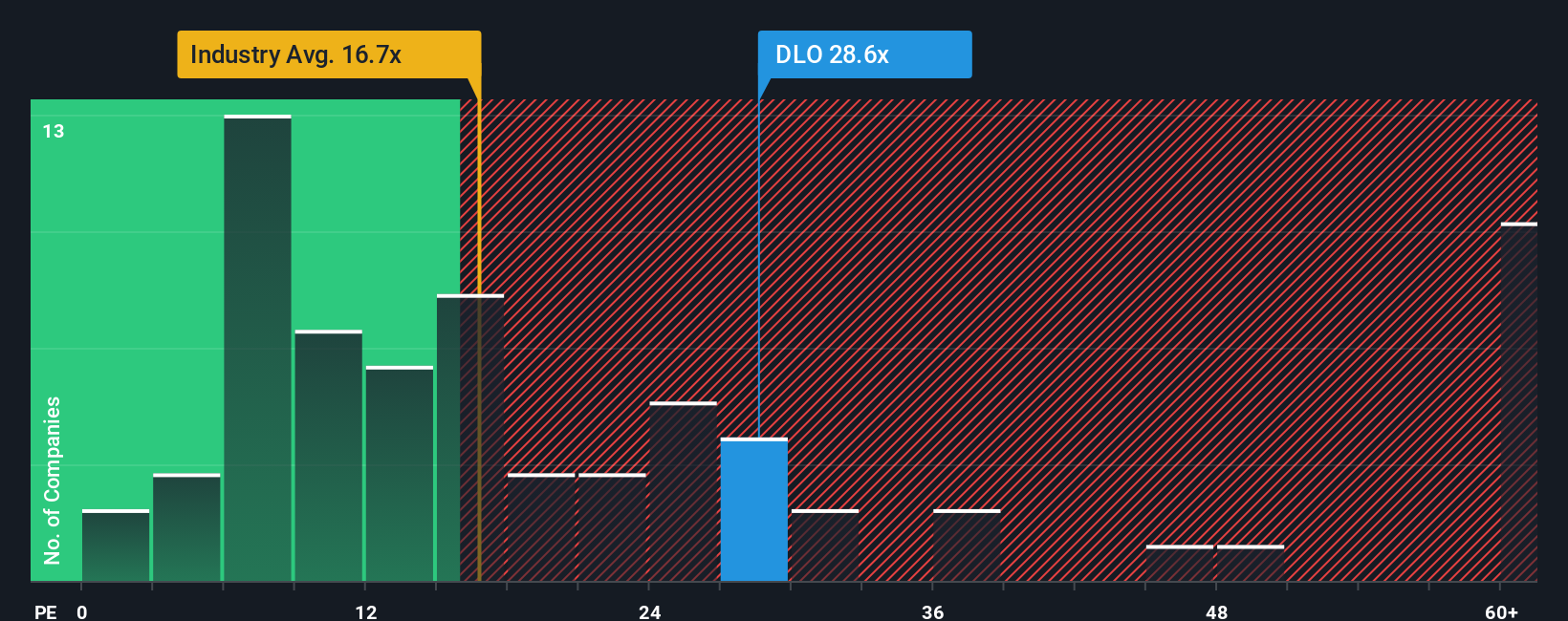

Looking at DLocal through the lens of its price-to-earnings ratio, the narrative changes. Shares trade at 23.2 times earnings, which is considerably higher than the US Diversified Financial industry average of 14 times. Compared with peers at 61.4 times, DLocal appears more affordable; however, its current valuation is above the fair ratio of 21.9 times.

This difference indicates some valuation risk because the market is already pricing in substantial growth. The question remains whether this premium can be justified or if expectations will need to be revised.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own DLocal Narrative

If you want to examine the data from a different angle or dive deeper on your own terms, crafting your personal outlook is quick and simple, typically taking under 3 minutes. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding DLocal.

Looking for More Investment Ideas?

Don’t let great opportunities slip past you. Power up your portfolio by checking out these compelling lists and give yourself the edge with expert-curated picks:

- Capitalize on breakthrough medical innovation by finding these 30 healthcare AI stocks driving real change in the healthcare industry and AI-powered diagnostics.

- Boost your passive income. Lock in reliable yields with these 15 dividend stocks with yields > 3% offering consistent returns that stand out in today’s market.

- Ride the cutting edge of finance and technology with these 81 cryptocurrency and blockchain stocks transforming how the world sees money and digital assets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DLO

Exceptional growth potential with outstanding track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative