Advertisement

- United States

- /

- Capital Markets

- /

- NasdaqGS:AVTA

Blucora, Inc. Just Missed Earnings; Here's What Analysts Are Forecasting Now

It's been a mediocre week for Blucora, Inc. (NASDAQ:BCOR) shareholders, with the stock dropping 11% to US$12.69 in the week since its latest first-quarter results. Revenues fell 4.2% short of expectations, at US$263m. Earnings correspondingly dipped, with Blucora reporting a statutory loss of US$6.60 per share, whereas the analysts had previously modelled a profit in this period. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Blucora after the latest results.

Check out our latest analysis for Blucora

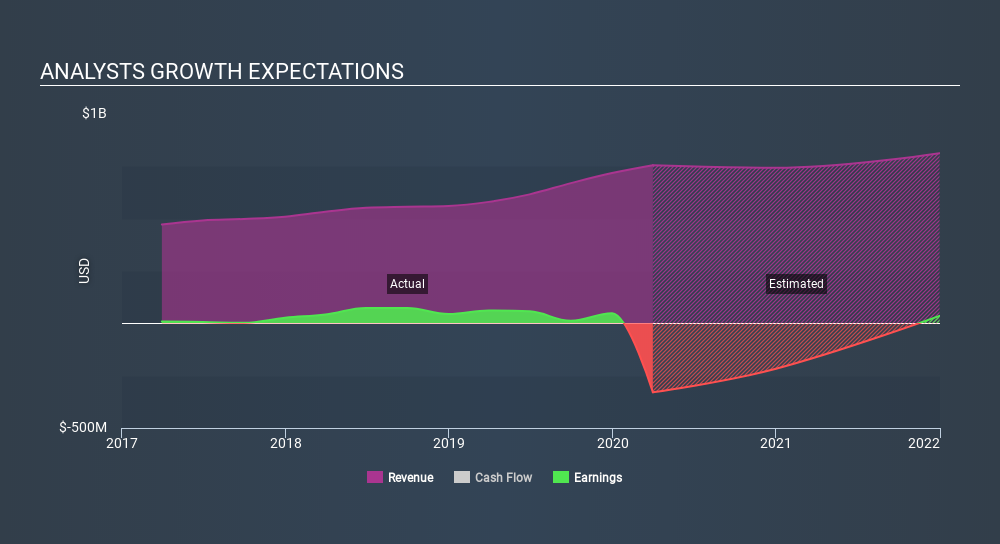

Following last week's earnings report, Blucora's three analysts are forecasting 2020 revenues to be US$743.4m, approximately in line with the last 12 months. Blucora is also expected to turn profitable, with statutory earnings of US$0.67 per share. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$798.9m and earnings per share (EPS) of US$0.33 in 2020. Although the analysts have lowered their sales forecasts, they've also made a sizeable expansion in their earnings per share estimates, which implies there's been something of an uptick in sentiment following the latest results.

The analysts have cut their price target 22% to US$21.50 per share, suggesting that the declining revenue was a more crucial indicator than the expected improvement in earnings. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic Blucora analyst has a price target of US$25.00 per share, while the most pessimistic values it at US$18.00. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. These estimates imply that sales are expected to slow, with a forecast revenue decline of 1.6%, a significant reduction from annual growth of 36% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 3.8% annually for the foreseeable future. It's pretty clear that Blucora's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Blucora's earnings potential next year. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. Yet - earnings are more important to the intrinsic value of the business. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple Blucora analysts - going out to 2021, and you can see them free on our platform here.

And what about risks? Every company has them, and we've spotted 2 warning signs for Blucora (of which 1 is a bit concerning!) you should know about.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:AVTA

Avantax

Avantax, Inc. provides wealth management solutions to consumers, small business owners, tax professionals, financial professionals, and certified public accounting firms in the United States.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor