Advertisement

- United States

- /

- Consumer Services

- /

- NYSE:GOTU

Gaotu Techedu (NYSE:GOTU) Net Loss Narrows Further, Supporting Bullish Turnaround Narratives

Simply Wall St

Reviewed by Simply Wall St

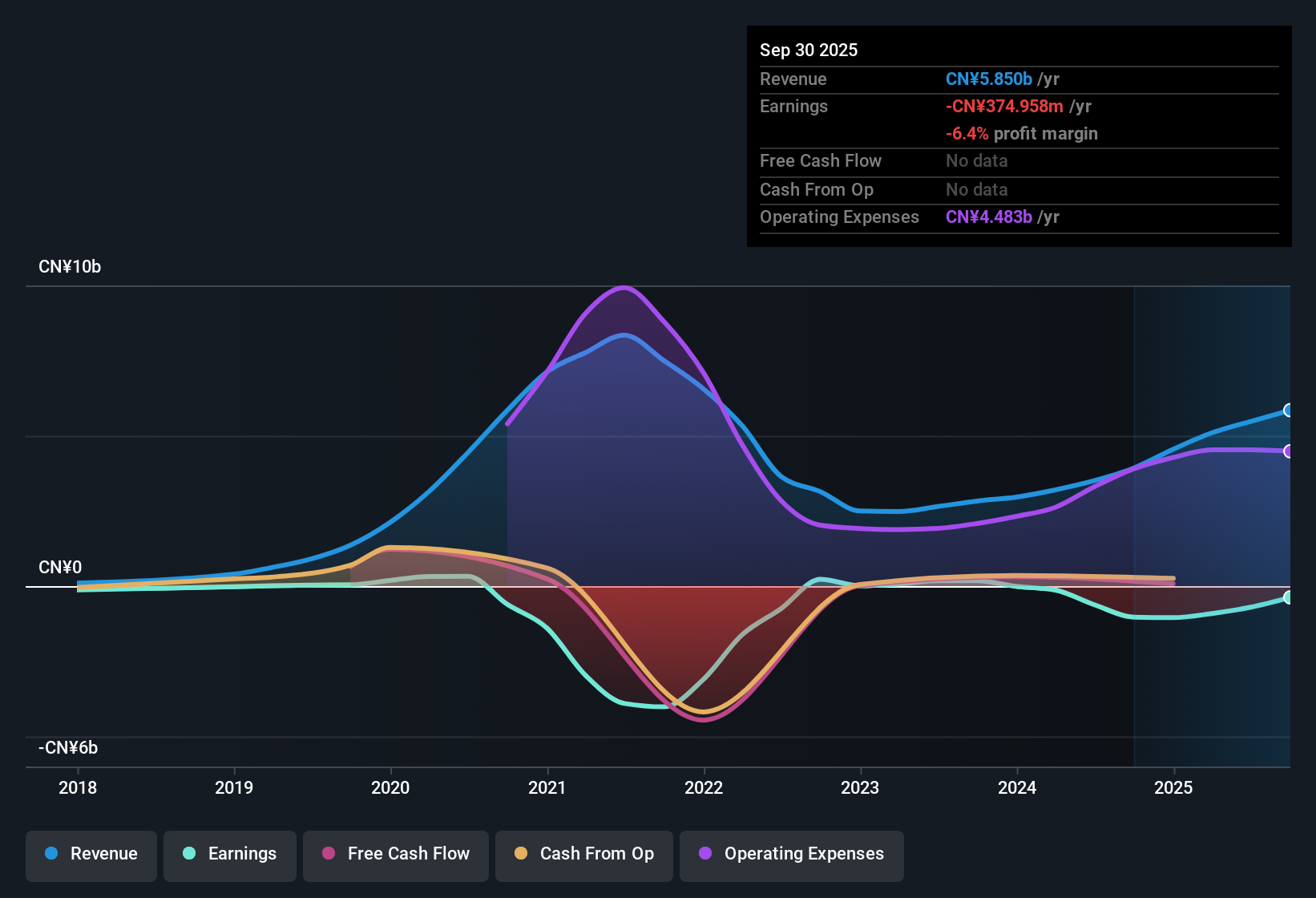

Gaotu Techedu (NYSE:GOTU) just released its Q3 2025 results, recording revenue of ¥1.6 billion and a basic EPS of -¥0.61. For context, the company’s revenue has climbed from ¥1.0 billion in Q2 2024 to ¥1.6 billion this quarter. Basic EPS has improved from -¥1.65 in Q2 2024. Investors will be watching how the company works to narrow its losses and maintain the current pace of revenue growth as margins remain in focus this quarter.

See our full analysis for Gaotu Techedu.Now that the headline numbers are in, we are comparing them against prevailing narratives to assess how market expectations align with the reported results.

Curious how numbers become stories that shape markets? Explore Community Narratives

Net Loss Shrinks to ¥147 Million

- Net income (excluding extraordinary items) improved to -¥147 million, up from -¥216 million last quarter, and a substantial improvement compared to -¥471 million in the same period last year.

- The AI narrative highlights the company's rapid reduction of annual losses, claiming a 38.2% per year improvement over the last five years. Recent quarters show continued progress towards profitability.

- Consistent reductions in net loss suggest profitability could be within reach. Forecasts anticipate a return to profit within three years.

- The ongoing trajectory challenges concerns about lingering unprofitability and supports the view that operational momentum is building.

Valuation Discount Widens Further

- Gaotu’s current price-to-sales ratio stands at 0.7x, which is lower than both peers (0.8x) and the broader US Consumer Services industry (1.4x). The share price of ¥2.40 trades 85.9% below the DCF fair value estimate of ¥16.99.

- The prevailing market perspective notes this pronounced discount. Bulls see the low trading multiple and deep fair value gap as supporting a recovery story if growth persists.

- The wide margin to DCF fair value gives valuation-focused investors greater confidence. Bears might argue the discount reflects persistent questions around sustainable profitability.

- Bulls counter that sector digitalization momentum and the absence of flagged risks suggest the setup for a meaningful share price catch-up if execution remains on track.

Revenue Growth Sustains Outperformance

- Trailing twelve-month revenue reached ¥5.9 billion, more than 15% above last year's ¥5.1 billion. Recent quarters have seen a steady climb from ¥1.0 billion in Q2 2024 to ¥1.6 billion in Q3 2025.

- The narrative underscores GOTU’s annual revenue growth forecast of 17%, notably ahead of the 10.5% expectation for the broader US market. Bulls highlight this as a rare growth premium in the sector.

- Rapid top-line momentum, paired with improving bottom-line trends, bolsters bullish arguments for a turnaround. This is especially true in light of sector headwinds that have stalled similar competitors.

- However, the growth emphasis is tempered by ongoing unprofitability. Top-line expansion alone may not be enough to trigger immediate re-rating without further earnings progress.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Gaotu Techedu's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Despite notable revenue growth, Gaotu Techedu continues to operate at a loss, raising concerns about how quickly it can achieve sustainable profitability.

If ongoing losses make you cautious, refocus on stable growth stocks screener (2073 results) for opportunities in companies with consistent earnings and revenue expansion, built for dependable long-term returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GOTU

Gaotu Techedu

A data-driven education company, provides learning services, educational content, and digitalized learning products in Mainland China.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative