Advertisement

- United States

- /

- Leisure

- /

- NasdaqGM:HERE

QuantaSing Group (NasdaqGM:QSG) Net Margin Expansion Challenges Concerns on Sustainable Profit Growth

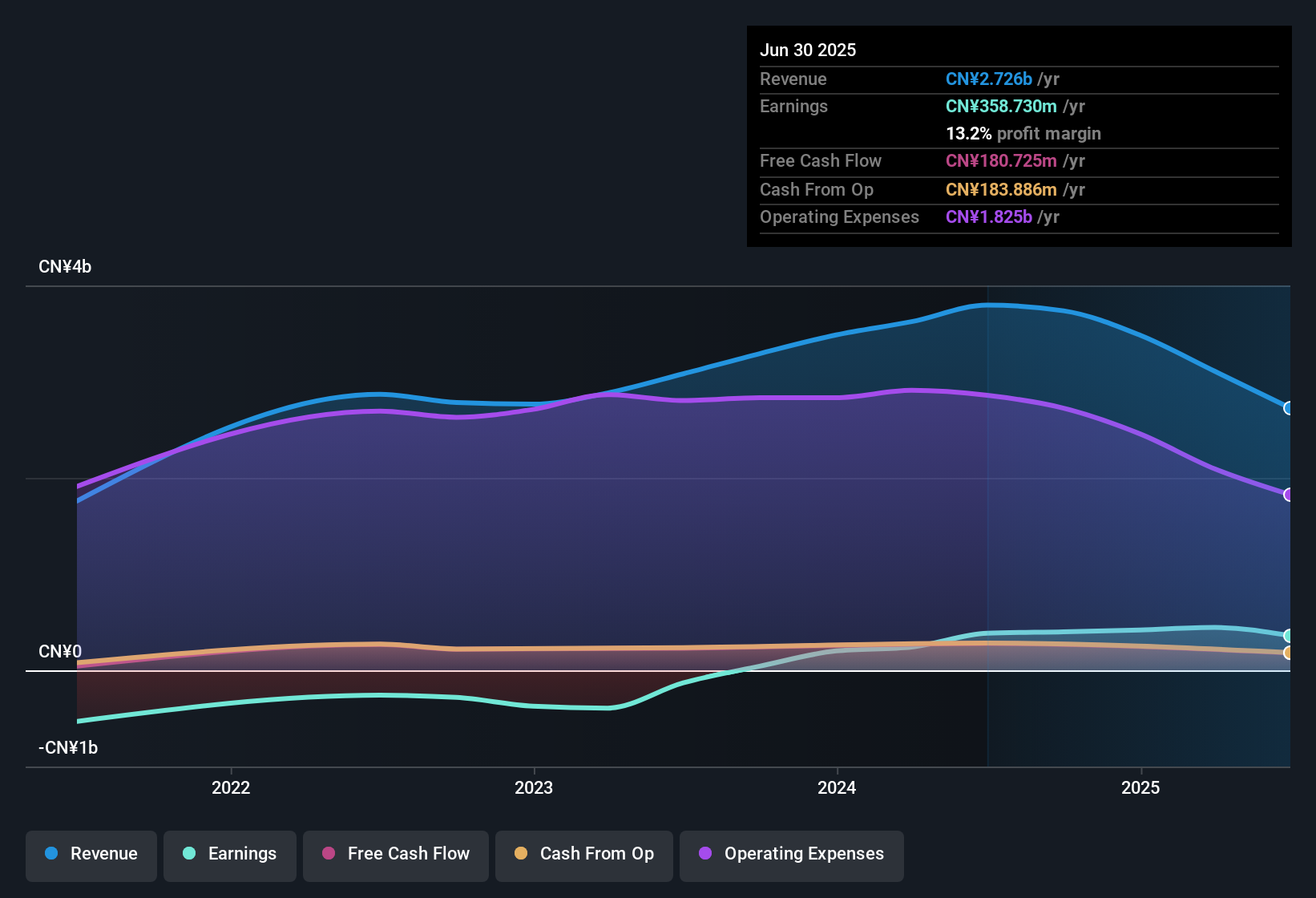

QuantaSing Group (NasdaqGM:QSG) posted robust numbers, with average annual earnings growth of 90.4% over the past five years and net profit margins rising to 13.2% from 10.2% last year. Revenue is expected to climb at 10.4% per year, while earnings are projected to grow 26.5% per year over the next three years. Both figures outpace US market averages. With shares trading at $7.16, below the estimated fair value of $8.21, and a price-to-earnings ratio of 7.3x that is well under industry peers, investors may see QSG's results as a compelling combination of value and strong growth outlook.

See our full analysis for QuantaSing Group.The next section will put these numbers side by side with the most widely discussed narratives to see which stories hold up and which get challenged by the data.

See what the community is saying about QuantaSing Group

Net Margins Climb Amid Cost Discipline

- Net profit margins grew to 13.2%, up from 10.2% last year. This reflects the company’s sharper focus on higher-value business lines and improved operational efficiency.

- Analysts' consensus view expects ongoing margin pressure from restructuring and initial outlays tied to new market entries. However, the margin advance this year strongly supports the move to high-quality growth.

- Consensus narrative highlights that improved cost discipline and strategic targeting of higher-value segments are the driving forces behind the margin gains.

- On the other hand, the consensus also flags a looming risk that initial costs and restructuring related to these shifts could drag on future net margins.

- Results this year provide a reality check to concerns about execution risk. Even so, the consensus narrative still advises caution as expansion costs may offset efficiency gains if not managed tightly.

📊 Read the full QuantaSing Group Consensus Narrative.

Revenue Volatility During Strategic Shift

- Revenue experienced a 25.9% decrease year-over-year during the recent pivot from traffic-driven to high-quality growth. This signals that the transition period poses real risks to revenue stability.

- Consensus narrative notes the decline stands in sharp contrast to the bullish argument for sustained top-line growth through business diversification.

- While expansion into wellness and senior-targeted offerings has added new revenue streams, the steep drop in core online learning billings, down 42.2% year-over-year, demonstrates that execution is not guaranteed to yield immediate benefits.

- The consensus further flags that ramp-up costs and the reliance on new business lines could lead to bumpy earnings as the company works to stabilize its base.

Valuation Signals Discount Versus Peers

- The current price-to-earnings ratio of 7.3x sits well below the US Consumer Services industry average of 18.8x and the peer average of 29.5x. This positions the stock at a notable discount even after recent performance swings.

- According to the analysts' consensus view, this discount is not simply a reflection of operational headwinds but also optimism that margin improvements and cost discipline may generate greater long-term value than the market currently recognizes.

- With shares trading at $7.16, both below DCF fair value ($8.21) and the average peer PE, the consensus suggests investors are underpricing QSG’s growth potential and emergent diversification in wellness and senior-oriented education.

- Nevertheless, the consensus narrative observes that volatility in revenues and fast-evolving market exposures warrant careful monitoring despite the value gap.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for QuantaSing Group on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have your take on the numbers? Share your perspective and craft a fresh narrative in just a few minutes. Do it your way

A great starting point for your QuantaSing Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

See What Else Is Out There

While QuantaSing Group’s net margins are improving, its volatile revenues during the strategic pivot expose risks to steady and reliable growth.

If you want companies that consistently deliver through ups and downs, check out stable growth stocks screener (2087 results) to find those with proven, stable performance across cycles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Here Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:HERE

Here Group

Designs and sells pop toys in China.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0777.3% undervalued

181 followersusers have followed this narrative

1 commentusers have commented on this narrative

27 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k10.9% overvalued

24 followersusers have followed this narrative

1 commentusers have commented on this narrative

25 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$50014.6% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

JO

Jolt_Communications on ZenaTech ·

ZenaTech: A big bet on the rise of AI drones and drones-as-a-service

Fair Value:US$6.8563.8% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Samsung Electronics ·

Samsung Electronics (005930): The "Silicon Renaissance" and the HBM4 Counter-Offensive

Fair Value:₩208k9.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Guan Huat Seng Holdings Berhad ·

Guan Huat Seng Holdings Berhad’s latest QR shows improving momentum, with stronger revenue, higher profit and first dividend

Fair Value:RM 0.3239.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SO

Souza123 on Inter & Co ·

Inter&Co - 60/30/30 Plan

Fair Value:US$33.374.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9827.9% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.7% undervalued

56 followersusers have followed this narrative

3 commentsusers have commented on this narrative

30 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6432.4% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative