Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:MCRI

Assessing Monarch Casino & Resort’s (MCRI) Valuation Following Its New AAA Four Diamond Hotel Recognition

Simply Wall St

Reviewed by Simply Wall St

Monarch Casino & Resort (MCRI) just received the AAA Four Diamond hotel designation. This accolade highlights the company's upgraded standards for amenities and guest service. The recognition can enhance the company’s reputation and appeal among travelers.

See our latest analysis for Monarch Casino & Resort.

Alongside this recognition, Monarch Casino & Resort has enjoyed a strong run with a year-to-date share price return of 24.27% and a one-year total shareholder return of nearly 16%. Momentum appears to be building, and recent awards continue to reinforce the company’s growth story.

If Monarch’s momentum has you rethinking your approach, now could be a good time to uncover opportunities through our fast growing stocks with high insider ownership.

With strong returns and new accolades fueling optimism, the key question now is whether Monarch Casino & Resort’s stock is trading below its true value or if the market has already anticipated its future success, leaving little room for upside.

Price-to-Earnings of 21.3x: Is it justified?

Monarch Casino & Resort trades on a price-to-earnings (P/E) ratio of 21.3x, slightly above the US Hospitality industry average of 20.8x. With its last close at $96.61, the company’s shares are currently priced at a premium compared to sector peers, raising questions about whether investors are overpaying for future earnings.

The P/E ratio measures what investors are willing to pay per dollar of the company’s earnings and is often used to gauge whether a stock is expensive or cheap relative to others in the same sector. In Monarch’s case, the premium could signal that the market is pricing in an optimistic outlook, despite modest growth projections and a recently reported one-off earnings hit.

Compared to the industry average, Monarch's P/E multiple is elevated but not dramatically out of line. However, when viewed against its estimated fair price-to-earnings ratio of 17.2x, the current valuation appears stretched. This higher figure could indicate that some positive catalysts are already factored into the stock, reducing the margin for error for new investors.

Explore the SWS fair ratio for Monarch Casino & Resort

Result: Price-to-Earnings of 21.3x (OVERVALUED)

However, slower revenue growth and recent share price volatility could both weigh on Monarch’s premium valuation if positive momentum slows.

Find out about the key risks to this Monarch Casino & Resort narrative.

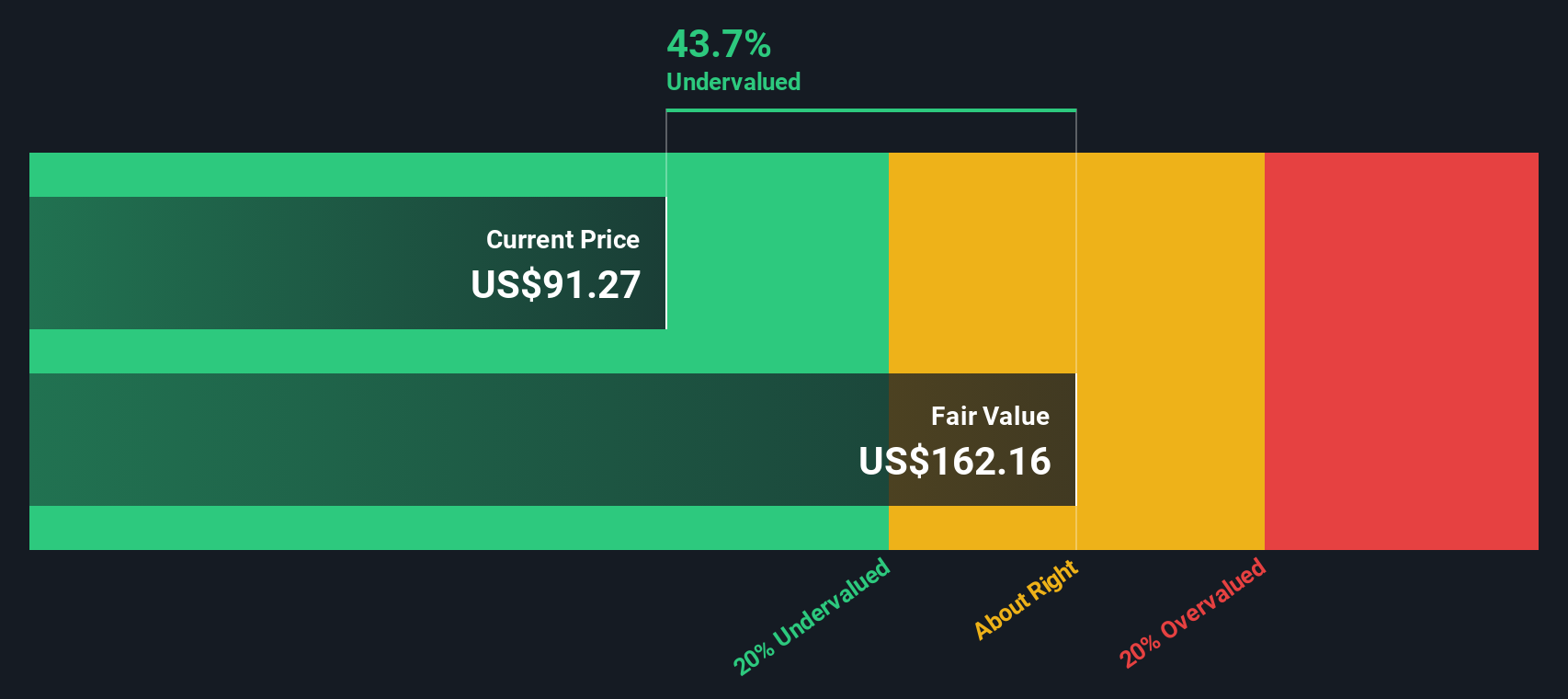

Another View: Discounted Cash Flow Offers a Different Perspective

While the price-to-earnings ratio suggests Monarch Casino & Resort is trading at a premium, our DCF model presents an opposing view. According to this approach, Monarch's shares trade roughly 41% below their calculated fair value. This hints at potential upside, even if the market seems cautious.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Monarch Casino & Resort for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 928 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Monarch Casino & Resort Narrative

If analyzing these figures sparks different conclusions or you prefer your own hands-on approach, you can craft a personal narrative in under three minutes, right here: Do it your way.

A great starting point for your Monarch Casino & Resort research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Level up your portfolio by tapping into stock trends that others might overlook. The best opportunities are often found by those who act decisively and think ahead.

- Capture reliable income with ease by checking out these 16 dividend stocks with yields > 3%, which offers yields above 3% and consistent cash returns.

- Accelerate your search for innovation by pinpointing industry disruptors among these 30 healthcare AI stocks as they change the future of medicine with artificial intelligence.

- Unlock unique growth prospects as you consider these 3594 penny stocks with strong financials, featuring strong financials and surprising potential in the small-cap space.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MCRI

Monarch Casino & Resort

Through its subsidiaries, owns and operates hotels and casinos.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor