Advertisement

- United States

- /

- Consumer Services

- /

- NasdaqCM:EJH

Earnings Working Against E-Home Household Service Holdings Limited's (NASDAQ:EJH) Share Price

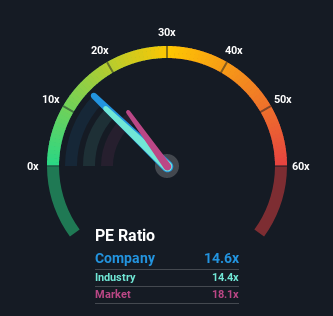

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") above 19x, you may consider E-Home Household Service Holdings Limited (NASDAQ:EJH) as an attractive investment with its 14.6x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

E-Home Household Service Holdings has been doing a good job lately as it's been growing earnings at a solid pace. One possibility is that the P/E is low because investors think this respectable earnings growth might actually underperform the broader market in the near future. If that doesn't eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

View our latest analysis for E-Home Household Service Holdings

Does Growth Match The Low P/E?

In order to justify its P/E ratio, E-Home Household Service Holdings would need to produce sluggish growth that's trailing the market.

Retrospectively, the last year delivered a decent 11% gain to the company's bottom line. However, this wasn't enough as the latest three year period has seen an unpleasant 45% overall drop in EPS. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

In contrast to the company, the rest of the market is expected to grow by 10% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

In light of this, it's understandable that E-Home Household Service Holdings' P/E would sit below the majority of other companies. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Bottom Line On E-Home Household Service Holdings' P/E

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of E-Home Household Service Holdings revealed its shrinking earnings over the medium-term are contributing to its low P/E, given the market is set to grow. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. If recent medium-term earnings trends continue, it's hard to see the share price moving strongly in either direction in the near future under these circumstances.

It is also worth noting that we have found 3 warning signs for E-Home Household Service Holdings (1 shouldn't be ignored!) that you need to take into consideration.

If these risks are making you reconsider your opinion on E-Home Household Service Holdings, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if E-Home Household Service Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:EJH

E-Home Household Service Holdings

Engages in the operation of household services in the People’s Republic of China.

Flawless balance sheet slight.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor