Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:WMT

Has Walmart Inc.'s (NYSE:WMT) Impressive Stock Performance Got Anything to Do With Its Fundamentals?

Walmart's (NYSE:WMT) stock is up by a considerable 19% over the past three months. We wonder if and what role the company's financials play in that price change as a company's long-term fundamentals usually dictate market outcomes. Specifically, we decided to study Walmart's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

View our latest analysis for Walmart

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Walmart is:

18% = US$16b ÷ US$91b (Based on the trailing twelve months to July 2024).

The 'return' is the profit over the last twelve months. So, this means that for every $1 of its shareholder's investments, the company generates a profit of $0.18.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Walmart's Earnings Growth And 18% ROE

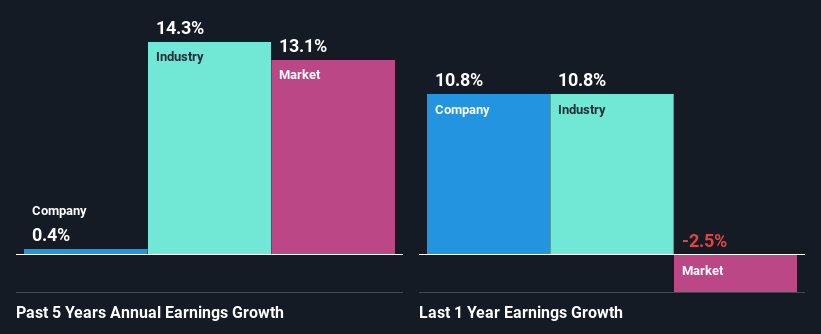

To start with, Walmart's ROE looks acceptable. On comparing with the average industry ROE of 11% the company's ROE looks pretty remarkable. However, we are curious as to how the high returns still resulted in flat growth for Walmart in the past five years. Therefore, there could be some other aspects that could potentially be preventing the company from growing. These include low earnings retention or poor allocation of capital.

As a next step, we compared Walmart's net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 14% in the same period.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. Has the market priced in the future outlook for WMT? You can find out in our latest intrinsic value infographic research report.

Is Walmart Using Its Retained Earnings Effectively?

Despite having a moderate three-year median payout ratio of 45% (meaning the company retains55% of profits) in the last three-year period, Walmart's earnings growth was more or les flat. So there could be some other explanation in that regard. For instance, the company's business may be deteriorating.

Moreover, Walmart has been paying dividends for at least ten years or more suggesting that management must have perceived that the shareholders prefer dividends over earnings growth. Our latest analyst data shows that the future payout ratio of the company is expected to drop to 32% over the next three years. The fact that the company's ROE is expected to rise to 22% over the same period is explained by the drop in the payout ratio.

Conclusion

In total, it does look like Walmart has some positive aspects to its business. However, given the high ROE and high profit retention, we would expect the company to be delivering strong earnings growth, but that isn't the case here. This suggests that there might be some external threat to the business, that's hampering its growth. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

Valuation is complex, but we're here to simplify it.

Discover if Walmart might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:WMT

Walmart

Engages in the operation of retail and wholesale stores and clubs, eCommerce websites, and mobile applications worldwide.

Outstanding track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

74 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative