Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:ACI

How Albertsons’ $1.5 Billion Debt Refinancing at ACI May Reshape Its Investment Story

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 10, 2025, Albertsons Companies and its subsidiaries issued US$1.5 billion in senior unsecured notes with maturities in 2031 and 2034, aiming to refinance existing debt and repay a portion of its revolving credit facility.

- This refinancing initiative is designed to provide Albertsons with greater financial flexibility and support its ongoing operational and growth objectives.

- We'll explore how Albertsons' large-scale debt refinancing may influence its future financial flexibility and the overall investment narrative.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

Albertsons Companies Investment Narrative Recap

To be a shareholder in Albertsons Companies, you need to believe in ongoing improvements in digital capabilities and operational efficiency, even as the grocery industry faces intense pricing competition and margin pressures. The recent US$1.5 billion debt refinancing is primarily about extending debt maturities and managing costs, with limited immediate impact on the most important short-term catalyst: profitable growth in e-commerce. The largest risk, rising labor costs amid ongoing union negotiations, remains unchanged by this announcement.

One of the most relevant recent announcements is the increased earnings guidance for fiscal 2025, projecting identical sales growth of 2.2% to 2.75%. While this supports confidence in near-term sales momentum, it does not materially alter the ongoing margin pressures the company faces from wage and benefit demands or the sensitivity to shifts in the digital and pharmacy segments.

In contrast, investors should be aware of the margin risks tied to labor costs, especially as...

Read the full narrative on Albertsons Companies (it's free!)

Albertsons Companies' outlook projects $86.1 billion in revenue and $1.1 billion in earnings by 2028. This is based on a 2.1% annual revenue growth and a $145.7 million increase in earnings from the current $954.3 million.

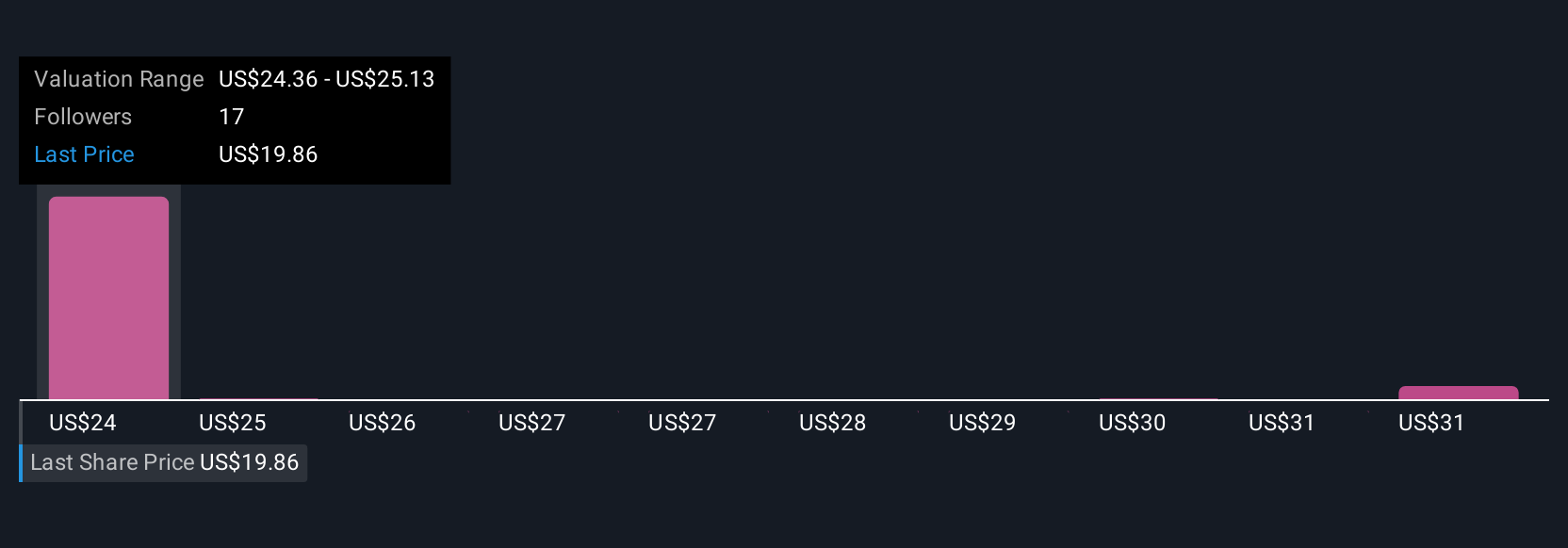

Uncover how Albertsons Companies' forecasts yield a $23.69 fair value, a 33% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community fair value estimates for Albertsons range widely from US$19.34 to US$38.57 across 7 viewpoints. While some forecasts assume operational improvements, the persistent risk of margin pressure amid rising labor and benefit expenses could impact future returns, consider how diverse these perspectives truly are.

Explore 7 other fair value estimates on Albertsons Companies - why the stock might be worth just $19.34!

Build Your Own Albertsons Companies Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Albertsons Companies research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Albertsons Companies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Albertsons Companies' overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ACI

Albertsons Companies

Through its subsidiaries, operates in the food and drug retail industry in the United States.

Very undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|24.0% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor