Advertisement

- United States

- /

- Food and Staples Retail

- /

- NasdaqCM:WBUY

Webuy Global Ltd's (NASDAQ:WBUY) Shares Not Telling The Full Story

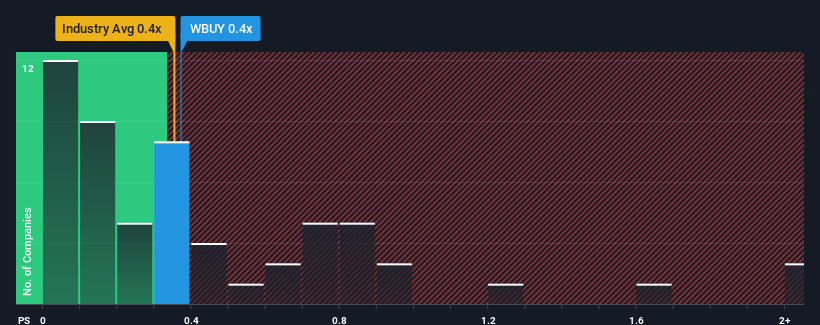

There wouldn't be many who think Webuy Global Ltd's (NASDAQ:WBUY) price-to-sales (or "P/S") ratio of 0.4x is worth a mention when the median P/S for the Consumer Retailing industry in the United States is very similar. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Webuy Global

What Does Webuy Global's Recent Performance Look Like?

Webuy Global certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. It might be that many expect the strong revenue performance to wane, which has kept the share price, and thus the P/S ratio, from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Although there are no analyst estimates available for Webuy Global, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.What Are Revenue Growth Metrics Telling Us About The P/S?

Webuy Global's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Retrospectively, the last year delivered an exceptional 38% gain to the company's top line. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, thanks in part to the last 12 months of revenue growth. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

This is in contrast to the rest of the industry, which is expected to grow by 3.9% over the next year, materially lower than the company's recent medium-term annualised growth rates.

In light of this, it's curious that Webuy Global's P/S sits in line with the majority of other companies. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

The Key Takeaway

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

To our surprise, Webuy Global revealed its three-year revenue trends aren't contributing to its P/S as much as we would have predicted, given they look better than current industry expectations. When we see strong revenue with faster-than-industry growth, we can only assume potential risks are what might be placing pressure on the P/S ratio. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to see the likelihood of revenue fluctuations in the future.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Webuy Global that you should be aware of.

If these risks are making you reconsider your opinion on Webuy Global, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Webuy Global might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:WBUY

Webuy Global

Operates as an e-commerce retailor with dual focus on grocery and travel in Singapore, Indonesia, and internationally.

Excellent balance sheet low.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor