Advertisement

- United States

- /

- Consumer Durables

- /

- NYSE:PHM

Should PulteGroup's (PHM) Persistent Share Buybacks Reframe How Investors Interpret Falling Profits?

Simply Wall St

Reviewed by Sasha Jovanovic

- PulteGroup, Inc. recently announced its third quarter 2025 financial results, reporting revenue of US$4.40 billion and net income of US$585.83 million, both down from the prior year, alongside a continued share repurchase program totaling 2,434,829 shares for US$300 million during the quarter.

- An interesting aspect is that the company has now retired more than 70% of its shares outstanding since 2013, reflecting an extensive and sustained commitment to returning capital to shareholders.

- We'll assess how lower quarterly earnings, in the context of ongoing share buybacks, affect PulteGroup's investment narrative and future earnings outlook.

Outshine the giants: these 27 early-stage AI stocks could fund your retirement.

PulteGroup Investment Narrative Recap

To be a shareholder in PulteGroup right now, you need conviction in the company’s ability to manage through near-term earnings pressure and softer homebuyer demand without eroding its long-term position in U.S. housing. The recent quarterly revenue and net income declines are in line with broader housing affordability challenges and do not materially shift the keys to PulteGroup’s outlook: the pace of new orders and the company’s margin resilience remain the most important catalyst and risk, respectively.

Among recent developments, the continued execution of PulteGroup’s share repurchase program stands out. With over 70% of its outstanding shares retired since 2013, including US$300 million repurchased last quarter, this remains highly relevant, as it supports per-share metrics even as absolute earnings contract, but does not eliminate core risks around regional demand and market volatility.

In contrast, investors should be aware of how elevated sales incentives, used to address affordability headwinds, could start to meaningfully impact profitability if they remain higher for longer than expected…

Read the full narrative on PulteGroup (it's free!)

PulteGroup's outlook forecasts $17.7 billion in revenue and $2.2 billion in earnings by 2028. This assumes revenue remains flat with a 0.0% annual growth rate and represents a $0.5 billion decrease in earnings from the current $2.7 billion.

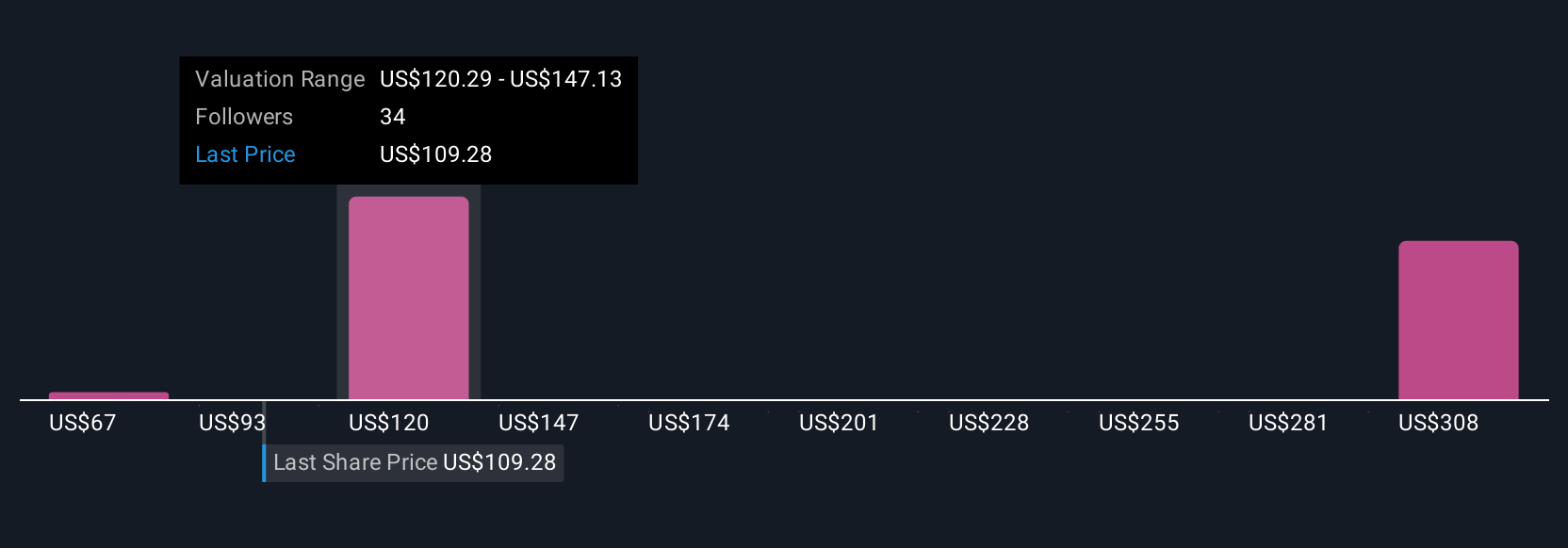

Uncover how PulteGroup's forecasts yield a $137.38 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Nine members of the Simply Wall St Community estimate PulteGroup’s fair value between US$88 and US$154.78 per share. In the context of recent earnings declines and ongoing margin risk, your own view on the company’s ability to withstand volatile housing demand can significantly shape your outlook, explore how these different perspectives might better inform your investment research.

Explore 9 other fair value estimates on PulteGroup - why the stock might be worth 27% less than the current price!

Build Your Own PulteGroup Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your PulteGroup research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free PulteGroup research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PulteGroup's overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PHM

PulteGroup

Through its subsidiaries, engages in the homebuilding business in the United States.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor