Advertisement

- United States

- /

- Consumer Durables

- /

- NYSE:NTZ

Companies Like Natuzzi (NYSE:NTZ) Can Afford To Invest In Growth

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, Natuzzi (NYSE:NTZ) shareholders have done very well over the last year, with the share price soaring by 503%. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

In light of its strong share price run, we think now is a good time to investigate how risky Natuzzi's cash burn is. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

View our latest analysis for Natuzzi

When Might Natuzzi Run Out Of Money?

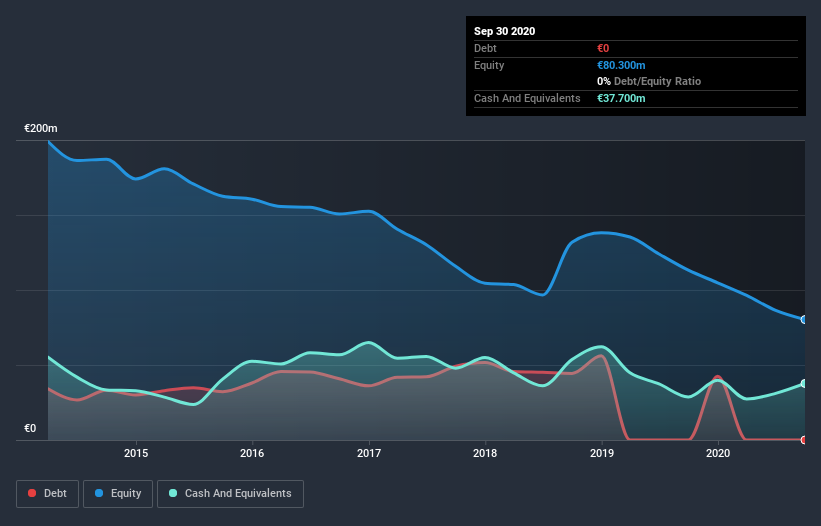

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. Natuzzi has such a small amount of debt that we'll set it aside, and focus on the €38m in cash it held at September 2020. Importantly, its cash burn was €2.6m over the trailing twelve months. So it had a very long cash runway of many years from September 2020. While this is only one measure of its cash burn situation, it certainly gives us the impression that holders have nothing to worry about. You can see how its cash balance has changed over time in the image below.

Is Natuzzi's Revenue Growing?

Given that Natuzzi actually had positive free cash flow last year, before burning cash this year, we'll focus on its operating revenue to get a measure of the business trajectory. Unfortunately, the last year has been a disappointment, with operating revenue dropping 18% during the period. Of course, we've only taken a quick look at the stock's growth metrics, here. This graph of historic earnings and revenue shows how Natuzzi is building its business over time.

How Hard Would It Be For Natuzzi To Raise More Cash For Growth?

Given its problematic fall in revenue, Natuzzi shareholders should consider how the company could fund its growth, if it turns out it needs more cash. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of €102m, Natuzzi's €2.6m in cash burn equates to about 2.5% of its market value. That means it could easily issue a few shares to fund more growth, and might well be in a position to borrow cheaply.

How Risky Is Natuzzi's Cash Burn Situation?

It may already be apparent to you that we're relatively comfortable with the way Natuzzi is burning through its cash. In particular, we think its cash runway stands out as evidence that the company is well on top of its spending. Although its falling revenue does give us reason for pause, the other metrics we discussed in this article form a positive picture overall. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. Separately, we looked at different risks affecting the company and spotted 2 warning signs for Natuzzi (of which 1 is a bit unpleasant!) you should know about.

Of course Natuzzi may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

When trading Natuzzi or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Natuzzi might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:NTZ

Natuzzi

Engages in the design, manufacture, and marketing of leather and fabric upholstered furniture.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|3.6% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor