Advertisement

Jeff Mezger became the CEO of KB Home (NYSE:KBH) in 2006, and we think it's a good time to look at the executive's compensation against the backdrop of overall company performance. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for KB Home.

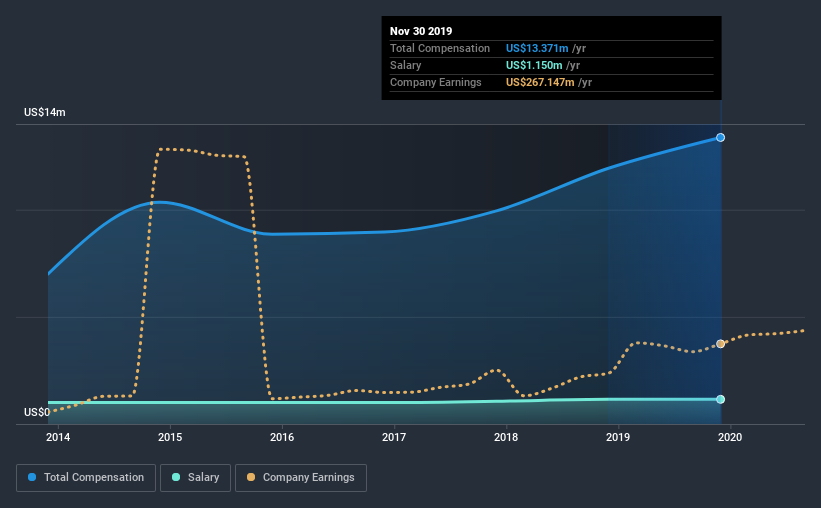

See our latest analysis for KB Home

Comparing KB Home's CEO Compensation With the industry

At the time of writing, our data shows that KB Home has a market capitalization of US$3.1b, and reported total annual CEO compensation of US$13m for the year to November 2019. We note that's an increase of 12% above last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$1.2m.

On comparing similar companies from the same industry with market caps ranging from US$2.0b to US$6.4b, we found that the median CEO total compensation was US$9.2m. This suggests that Jeff Mezger is paid more than the median for the industry. What's more, Jeff Mezger holds US$34m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | US$1.2m | US$1.2m | 9% |

| Other | US$12m | US$11m | 91% |

| Total Compensation | US$13m | US$12m | 100% |

On an industry level, around 27% of total compensation represents salary and 73% is other remuneration. In KB Home's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at KB Home's Growth Numbers

KB Home's earnings per share (EPS) grew 31% per year over the last three years. Its revenue is up 4.7% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's good to see a bit of revenue growth, as this suggests the business is able to grow sustainably. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has KB Home Been A Good Investment?

With a total shareholder return of 22% over three years, KB Home shareholders would, in general, be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

In Summary...

As we touched on above, KB Home is currently paying its CEO higher than the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. However, the EPS growth over three years is certainly impressive. We also note that, over the same time frame, shareholder returns haven't been bad. While it may be worth researching further, we don't see a problem with the high CEO pay, given the good EPS growth.

CEO compensation can have a massive impact on performance, but it's just one element. We did our research and spotted 3 warning signs for KB Home that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you’re looking to trade KB Home, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if KB Home might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NYSE:KBH

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor