Garmin (GRMN) shares have slipped around 24% over the past month, drawing attention from investors curious about the reasons for the downturn. While the company has experienced steady annual revenue and net income growth, recent performance suggests shifting market sentiment.

Garmin’s share price has taken a sharp turn this past month. However, when looking at the bigger picture, its three- and five-year total shareholder returns are still impressive, up 122.96% and 81.75% respectively. While recent momentum has faded, investors are considering whether this pullback presents new growth potential or signals changing sentiment.

With Garmin now trading about 15% below its estimated intrinsic value and nearly 22% under analyst price targets, the question remains: is this a genuine buying opportunity, or are current prices already factoring in future growth?

Advertisement

Most Popular Narrative: 18% Undervalued

The most widely followed narrative assigns Garmin a fair value well above its last close of $189.62. This illustrates that analysts see notable upside from current levels and frames the company’s growth story as far from over.

The launch of the Garmin Connect+ premium service, which offers AI-based health and fitness insights, is likely to boost subscription-based revenue growth and improve overall margins through higher-margin services. The new vívoactive 6 smartwatch release, with advanced features like an AMOLED display and enhanced sports apps, suggests potential revenue growth in the Fitness segment, supported by strong demand for advanced wearables.

Curious how much future success in wearables, innovative rollouts, and premium subscriptions could shift Garmin’s valuation? The big bet here is on surging demand for next-gen devices and new income streams. Want to see how bullish financial assumptions drive this striking upside versus today’s price? Read the full narrative to uncover what sets this fair value apart.

However, persistent market softness in Marine and higher operating expenses could compress margins, which may pose real hurdles to Garmin’s bullish projections.

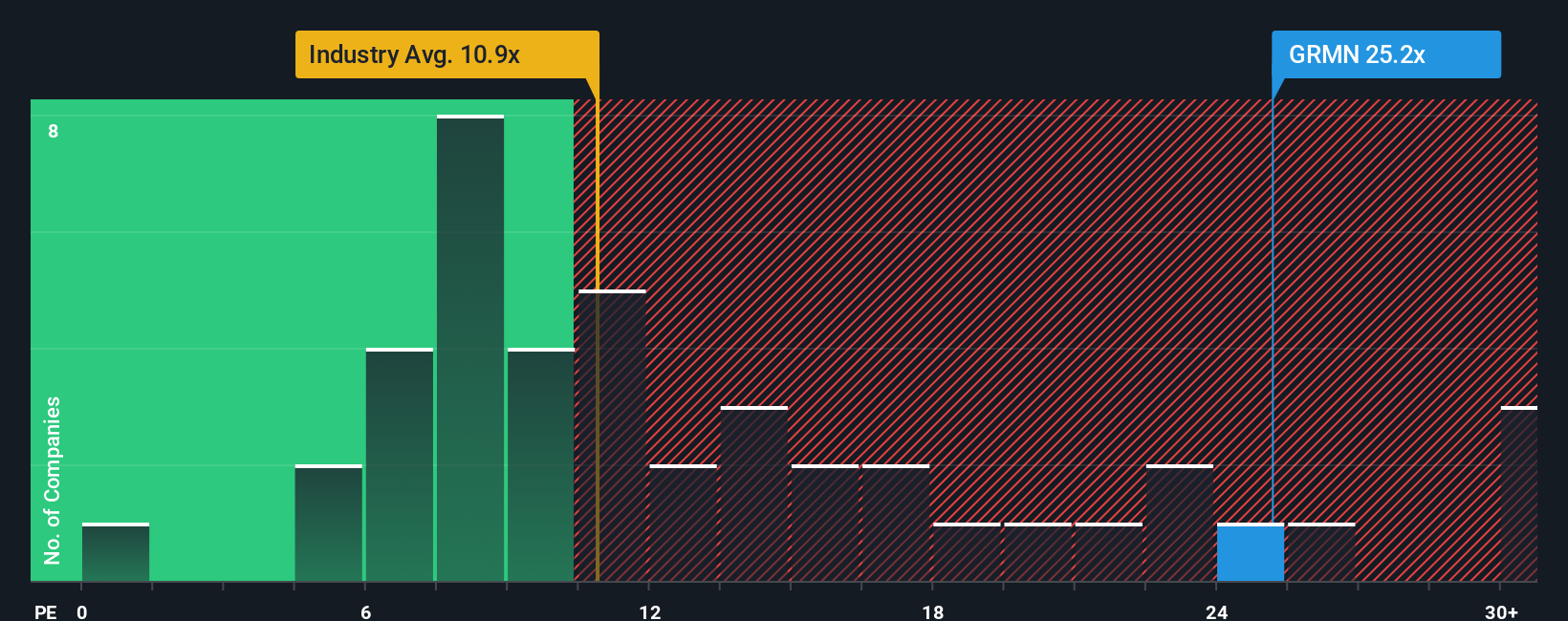

While some see Garmin as undervalued, a closer look at its price-to-earnings ratio tells a different story. Garmin trades at 23.2x earnings, which is noticeably higher than the industry average of 11.1x, its peer average of 21.8x, and the fair ratio of 18.3x. This premium pricing suggests the market is already including a good deal of optimism, increasing the risk that expectations may be set too high. Could this make future growth harder to realize, or is there something the multiples are missing?

You could be one smart move away from your next big winner. Turn market momentum in your favour with these powerful stock ideas. Don’t let opportunity pass you by.

Catch the AI wave and spot future leaders using these 26 AI penny stocks transforming industries with intelligent innovation.

Capitalize on emerging mega-trends by checking out these 26 quantum computing stocks that are advancing quantum computing breakthroughs right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks