- United States

- /

- Consumer Durables

- /

- NYSE:DHI

Need To Know: Analysts Are Much More Bullish On D.R. Horton, Inc. (NYSE:DHI)

Shareholders in D.R. Horton, Inc. (NYSE:DHI) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects. The market seems to be pricing in some improvement in the business too, with the stock up 9.1% over the past week, closing at US$109. Could this big upgrade push the stock even higher?

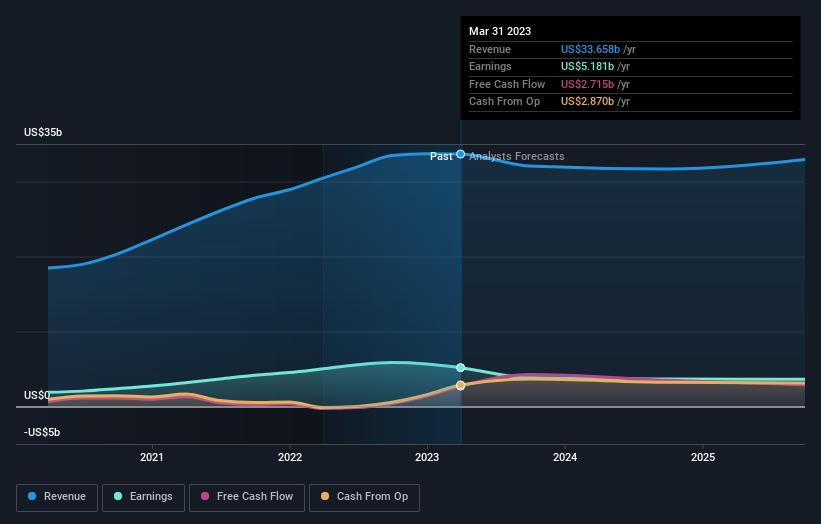

Following the latest upgrade, the 14 analysts covering D.R. Horton provided consensus estimates of US$32b revenue in 2023, which would reflect a noticeable 4.7% decline on its sales over the past 12 months. Statutory earnings per share are supposed to tumble 26% to US$11.17 in the same period. Prior to this update, the analysts had been forecasting revenues of US$28b and earnings per share (EPS) of US$9.15 in 2023. So we can see there's been a pretty clear increase in analyst sentiment in recent times, with both revenues and earnings per share receiving a decent lift in the latest estimates.

View our latest analysis for D.R. Horton

With these upgrades, we're not surprised to see that the analysts have lifted their price target 11% to US$121 per share. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic D.R. Horton analyst has a price target of US$148 per share, while the most pessimistic values it at US$98.00. This shows there is still some diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 9.2% by the end of 2023. This indicates a significant reduction from annual growth of 18% over the last five years. Yet aggregate analyst estimates for other companies in the industry suggest that industry revenues are forecast to decline 0.4% per year. So it's pretty clear that D.R. Horton's revenues are expected to shrink faster than the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for this year, expecting improving business conditions. They also upgraded their revenue estimates, with sales apparently performing well even though revenue growth expected to decline against the wider market this year. Given that the consensus looks almost universally bullish, with a substantial increase to forecasts and a higher price target, D.R. Horton could be worth investigating further.

Analysts are definitely bullish on D.R. Horton, but no company is perfect. Indeed, you should know that there are several potential concerns to be aware of, including recent substantial insider selling. You can learn more, and discover the 1 other concern we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:DHI

D.R. Horton

Operates as a homebuilding company in East, North, Southeast, South Central, Southwest, and Northwest regions in the United States.

Excellent balance sheet and good value.