TopBuild (BLD) has returned about 2% over the past month, and investors are watching closely as the company’s performance continues to reflect trends in the construction and building products sector. The stock’s trajectory raises some interesting valuation considerations.

TopBuild’s share price momentum has moderated a bit after some earlier gains, but the strong year-to-date price return of about 31% reflects persistent optimism around construction demand and the company’s execution. While the 12-month total shareholder return of roughly 9% is more modest, TopBuild’s long-term track record shows compounded strength, especially with a three-year total return exceeding 150%.

With TopBuild’s shares trading just below analyst targets and recent gains cooling, investors are left wondering whether the current price reflects all the company’s future potential or if there is still a compelling entry point.

Advertisement

Most Popular Narrative: 16.4% Undervalued

With TopBuild’s fair value set at $485.08 in the most widely followed narrative, and the last close at $405.71, followers see considerable upside from today’s price. The narrative’s case hinges on new revenue streams, ongoing acquisition momentum, and the durability of its margin story, all while discounting future cash flows at 8.92%.

The company’s disciplined M&A strategy in a highly fragmented industry, along with investments in operational efficiencies and supply chain optimization, is expected to unlock synergies, expand scale, and drive incremental EBITDA margin improvements, contributing to stronger future earnings growth.

This bold valuation is not just about surface-level growth. Hidden beneath are aggressive margin forecasts and reduced shares outstanding, which combine to produce a premium earnings multiple more similar to fast-growing technology firms. Ever wondered what blend of assumptions drives this high fair value? The full narrative uncovers the surprising math and pivotal projections supporting this price target.

However, ongoing weakness in U.S. home construction and challenges related to integrating recent acquisitions could quickly change TopBuild’s positive outlook in coming quarters.

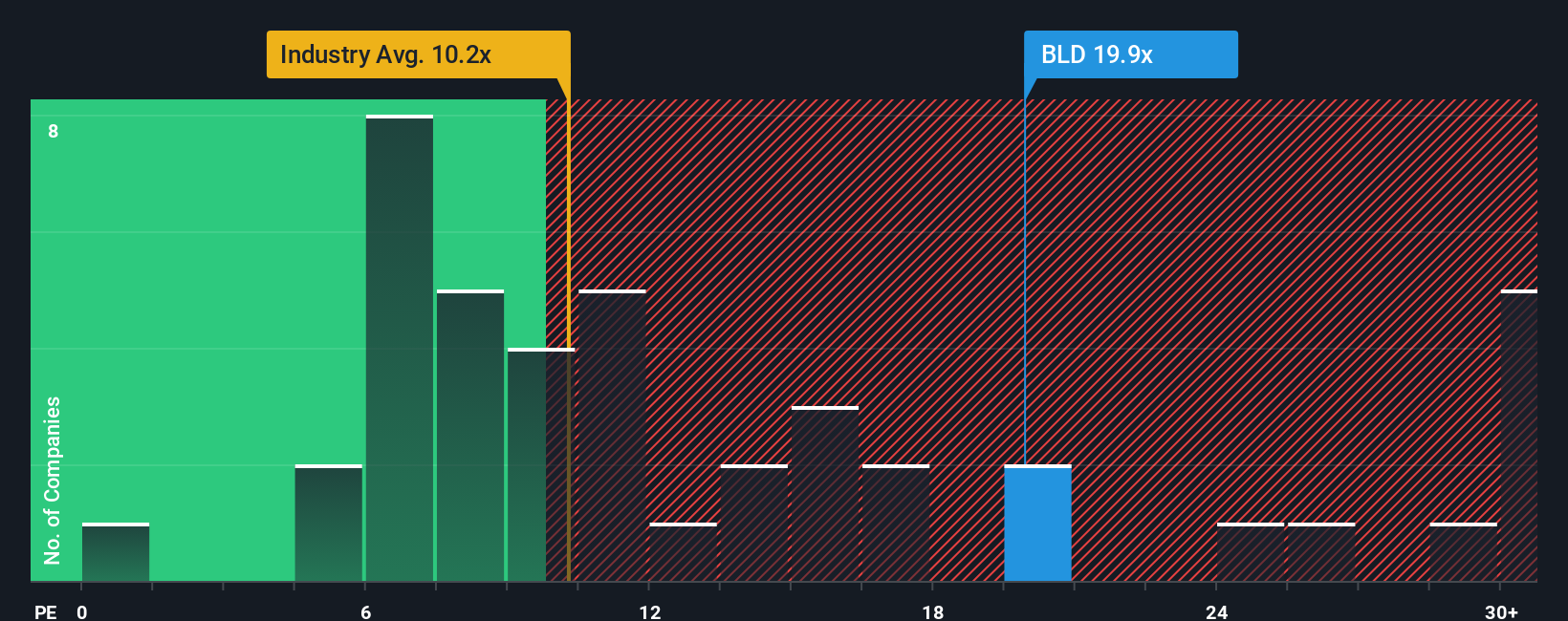

While some narratives point to upside, market-based valuation signals a different picture. TopBuild trades at a 19.9x price-to-earnings ratio, which is well above the industry’s 10.9x average and even peers at 14.8x. The fair ratio sits at 15.3x, suggesting investors may be paying a premium for growth that is not guaranteed. Does this premium heighten risk, or is the business worth it?

If you think the story could look different or want to dig deeper into the numbers yourself, it takes just a few minutes to build your own perspective. Do it your way

Don’t let opportunity pass you by. Unlock hidden gems and fresh angles with the Simply Wall Street Screener, and take your next step toward smarter investing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TopBuild might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.