Stock Analysis

- United States

- /

- Luxury

- /

- NasdaqGS:COLM

We Think Columbia Sportswear (NASDAQ:COLM) Can Stay On Top Of Its Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Columbia Sportswear Company (NASDAQ:COLM) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Check out the opportunities and risks within the US Luxury industry.

What Is Columbia Sportswear's Debt?

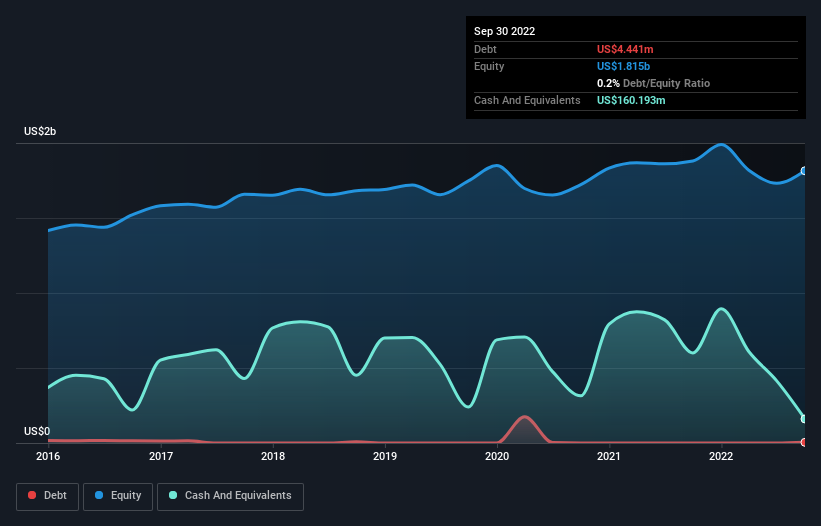

You can click the graphic below for the historical numbers, but it shows that as of September 2022 Columbia Sportswear had US$4.44m of debt, an increase on none, over one year. However, it does have US$160.2m in cash offsetting this, leading to net cash of US$155.8m.

A Look At Columbia Sportswear's Liabilities

We can see from the most recent balance sheet that Columbia Sportswear had liabilities of US$696.7m falling due within a year, and liabilities of US$378.7m due beyond that. Offsetting this, it had US$160.2m in cash and US$600.5m in receivables that were due within 12 months. So its liabilities total US$314.7m more than the combination of its cash and short-term receivables.

Of course, Columbia Sportswear has a market capitalization of US$5.01b, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Columbia Sportswear also has more cash than debt, so we're pretty confident it can manage its debt safely.

And we also note warmly that Columbia Sportswear grew its EBIT by 11% last year, making its debt load easier to handle. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Columbia Sportswear's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Columbia Sportswear has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last three years, Columbia Sportswear produced sturdy free cash flow equating to 64% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing Up

We could understand if investors are concerned about Columbia Sportswear's liabilities, but we can be reassured by the fact it has has net cash of US$155.8m. So we don't think Columbia Sportswear's use of debt is risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for Columbia Sportswear you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're helping make it simple.

Find out whether Columbia Sportswear is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:COLM

Columbia Sportswear

Designs, develops, markets, and distributes outdoor, active, and everyday lifestyle apparel, footwear, accessories, and equipment in the United States, Latin America, the Asia Pacific, Europe, the Middle East, Africa, and Canada.

Flawless balance sheet average dividend payer.