Advertisement

- United States

- /

- Commercial Services

- /

- NYSE:WCN

A Fresh Look at Waste Connections (WCN) Valuation After Strong Q3 Results and Double-Digit Dividend Growth

Simply Wall St

Reviewed by Simply Wall St

Waste Connections (NYSE:WCN) just delivered Q3 results that topped both revenue and adjusted EBITDA forecasts, driven by tight cost controls and ongoing strategic mergers. The company also approved its 15th straight year of double-digit dividend growth.

See our latest analysis for Waste Connections.

Waste Connections has kept investors on their toes this year, not just with strong quarterly results and another impressive dividend hike, but also through steady buybacks and reaffirmed guidance. Despite these shareholder-friendly moves, the stock has faced some short-term pressure, with a recent 1-year total return of -4.6%. Its five-year total return remains a robust 63%. Momentum has faded a bit in recent months, but the company’s long-term track record and ongoing activity suggest there is still plenty for patient investors to watch.

If you’re curious where else strategic buybacks and operational upgrades are making an impact, take the next step and discover fast growing stocks with high insider ownership

Yet with shares still trading noticeably below average analyst price targets and a hefty intrinsic discount to fair value, investors now face a key question: Is Waste Connections undervalued and on sale, or is future growth already baked into the stock price?

Most Popular Narrative: 18.9% Undervalued

With Waste Connections closing at $167.68, the current narrative values the company’s fair worth almost 19% higher. This gap is fueled by bold growth assumptions and margin improvements that may surprise many investors.

Enhanced safety performance and strategic recycling facility integration contribute to cost savings and expanded service capabilities, supporting future growth.

Curious how this fair value is calculated? The secret lies in the narrative’s focus on acquisition-driven growth, operational upgrades, and surprising future profit margins. Want to see which aggressive financial forecasts support this bullish price?

Result: Fair Value of $206.77 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, challenges such as reliance on acquisitions and volatile commodity-driven revenues could significantly alter Waste Connections’ growth outlook if conditions change.

Find out about the key risks to this Waste Connections narrative.

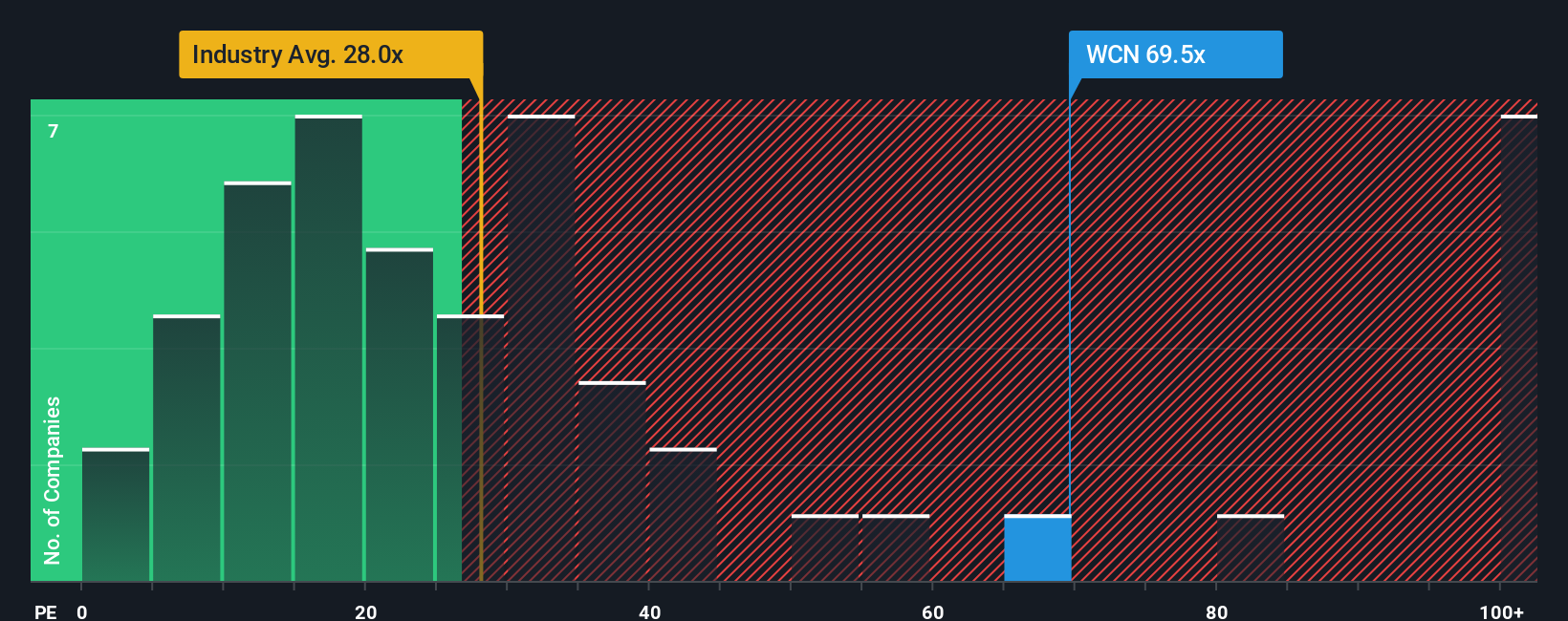

Another View: Expensive on Earnings Compared to Peers

While the main narrative values Waste Connections as significantly undervalued, a quick look at the actual price-to-earnings ratio tells a different story. At 69x, the company’s multiple is roughly double its industry average of 22.3x and well above the fair ratio of 34.2x. This signals notable valuation risk if peer sentiment prevails. Is this a premium worth paying, or could a re-rating close the gap?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Waste Connections Narrative

If you’re not convinced by the popular take or want to dive deeper into the numbers yourself, you can build your version in just minutes, and Do it your way

A great starting point for your Waste Connections research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Why settle for just one opportunity? Smart investors are tracking trends across multiple sectors. Take action today so you don’t miss out on tomorrow’s winners.

- Capitalize on overlooked markets by targeting these 3588 penny stocks with strong financials with strong fundamentals and untapped growth potential.

- Ride the wave of innovation by seeking out these 27 AI penny stocks at the forefront of artificial intelligence and automation advancements.

- Secure your portfolio's income with these 22 dividend stocks with yields > 3% offering robust yields that can deliver returns even in uncertain markets.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Waste Connections might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WCN

Waste Connections

Provides non-hazardous waste collection, transfer, disposal, and resource recovery services in the United States and Canada.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor