Steelcase (SCS) shares have climbed over the past three months, with the stock returning more than 54% during that period. This comes as investors focus on the company’s steady annual revenue and solid net income gains.

Steelcase’s momentum has really picked up, not just in the last quarter, but across the past year as a whole. With a 90-day share price return of nearly 55% and a robust total shareholder return of 39% over the past year, confidence in the company’s growth prospects is clearly on the rise among investors.

With shares trading just shy of their analyst price target and healthy financial growth on record, investors are left to ask: Is Steelcase still undervalued, or is the current stock price already factoring in all future gains?

Advertisement

Most Popular Narrative: 7.6% Overvalued

According to codabat, Steelcase’s intrinsic value per share stands slightly below the current market price, suggesting that recent share gains may have outpaced underlying fundamentals. The narrative points to a business with appealing valuation signals, yet not without significant caveats regarding sustainability and future growth.

Based on sector-relative P/E analysis, Steelcase appears moderately undervalued. Using TTM EPS of $1.04 and applying the furniture industry average P/E multiple of 15x, the intrinsic fair value equals $15.60 per share. Key assumptions include a normalized P/E of 15x, reflecting the furniture industry median. The maintainability of current TTM earnings of $1.04 is also assumed. Additionally, it is expected that the SCS multiple will align with furniture peers, and that office furniture demand will stabilize as part of a cyclical recovery.

Ready for the full story? Codabat’s valuation depends on a handful of critical accounting decisions and industry comparisons that could shift the narrative considerably. What subtle forecast changes are behind this number? Don’t miss the eye-opening details fueling this controversial call.

However, persistent margin pressure or a slower office real estate recovery could quickly undermine this outlook. This highlights real risks behind the current optimism.

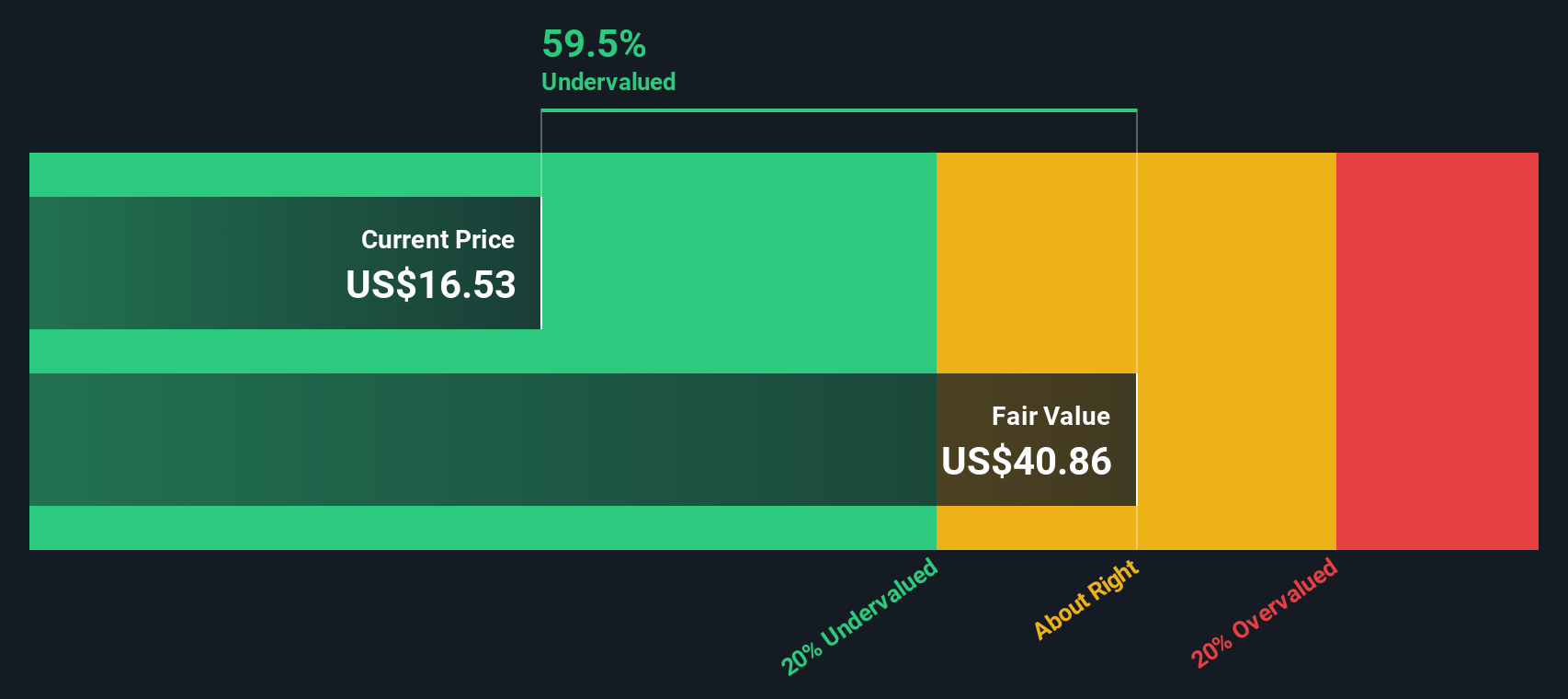

Another View: Discounted Cash Flow Tells a Different Story

While the narrative above leans on a price-to-earnings approach, the SWS DCF model points in a different direction. This model suggests Steelcase is trading at nearly 60% below its fair value, which indicates far more upside than a multiples analysis implies. So, can you trust the DCF outlook, or is this a classic value trap?

If you have your own perspective or favor hands-on research, you can dive into the numbers and build your own view in just a few minutes, or simply Do it your way.

The smartest investors never stop at just one opportunity. Don’t sit on the sidelines while market leaders shape tomorrow’s financial landscape. These handpicked screeners can help you seize your advantage right now:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks