Rollins (ROL) continues to draw steady attention from investors as its stock performance trends higher this month. Over the past month, shares have gained around 3%, which adds to a strong year-to-date return.

The momentum behind Rollins is not just a short-term story. The share price has climbed steadily this year, building on recent gains and resulting in a robust year-to-date share price return of 27.3 percent. Looking further out, total shareholder return over the past three and five years stands at 46.1 percent and 58.6 percent respectively. This illustrates that investors who remained with Rollins have seen rewards for their patience, even through periods of short-term volatility.

With such impressive momentum, the key question becomes whether Rollins’s current price still reflects a potential bargain, or if the market has already factored in every bit of expected future growth. Could there be more upside for new investors?

Advertisement

Most Popular Narrative: 3% Undervalued

With Rollins' fair value estimated at $60.42, slightly above its last close of $58.61, the narrative points to a modest upside. Investors are watching closely to see if the company can live up to these expectations.

The acquisition of Saela Pest Control is expected to add between $45 million to $50 million in revenue in 2025 and is anticipated to be accretive to earnings, signaling potential revenue growth and earnings enhancement. Continued strategic investments in sales staffing and marketing are expected to drive organic growth, particularly as the pest control season ramps up, which could lead to increased revenue.

Curious how Rollins’s growth story stacks up? The narrative behind this fair value hinges on aggressive top-line expansion, margin improvement, and a future profit multiple that sets a high bar. Want to see what assumptions underpin these bold projections? Unlock the full narrative to dig into the surprising drivers fueling this price target.

However, risks remain, including increased competition and the potential for market volatility, which could challenge Rollins's growth momentum in the months ahead.

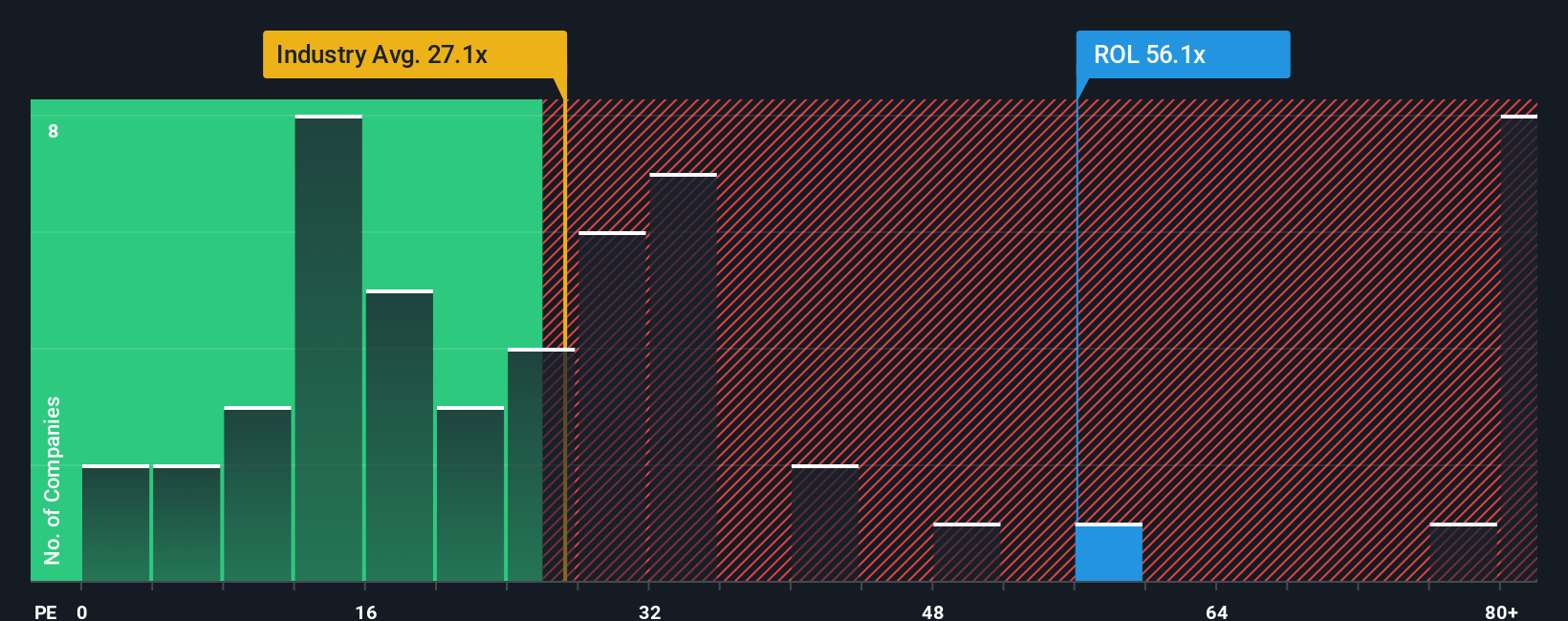

Looking at Rollins through the lens of valuation multiples reveals a different perspective. Its price-to-earnings ratio stands at 55.1x, which is notably higher than the US Commercial Services industry average of 22.2x and the peer average of 38.5x. Even compared to its fair ratio of 27.5x, Rollins trades at a significant premium. This elevated multiple suggests the market expects exceptional growth, but it also exposes investors to more downside risk if those expectations fall short. Does this premium truly reflect Rollins’ future potential, or is the bar set too high?

If you would like to chart your own course or dig deeper into the numbers, you can develop your own view on Rollins in just a few minutes, and Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Rollins.

Ready for More Investment Opportunities?

Smart investors always keep their options open. Don’t let the next breakout stock or sector trend slip past you. Find your edge with these powerful tools from Simply Wall Street:

Capitalize on rapid technological change by targeting tomorrow’s disruptors through these 25 AI penny stocks, unlocking access to companies at the forefront of artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Through its subsidiaries, provides pest and wildlife control services to residential and commercial customers in the United States and internationally.