Parsons (PSN) shares have seen a handful of ups and downs, with the stock still sitting well above its price three years ago. Investors eye the current valuation after recent movements, as they weigh longer-term growth against shorter-term swings.

This year, Parsons’ share price has been choppy, managing a 7.97% lift over the past 90 days but giving up ground overall with a -24.15% total shareholder return over the last twelve months. Although momentum has cooled recently, the company’s three- and five-year total shareholder returns of 68% and 164% respectively suggest considerable long-term growth potential.

With shares recently retreating from previous highs, but long-term returns remaining robust, is Parsons now trading below its true worth, or has the market already priced in the company’s anticipated growth trajectory?

Advertisement

Most Popular Narrative: 7.6% Undervalued

With Parsons closing at $83.14, the most widely followed narrative sets a fair value of $90 per share, implying a meaningful upside from current levels. This narrative is shaped by expectations for ongoing revenue growth and higher future profit margins, set against industry dynamics and company developments.

Parsons is poised to benefit from ongoing multi-year increases in global and U.S. infrastructure investment, particularly in hard infrastructure like roads, bridges, airports, and transit. This trend is driven by bipartisan government support and major legislation (IIJA, Surface Transportation Reauthorization), with revenue visibility and growth supported by an $8.9 billion backlog and substantial unbooked pipeline. This positions revenue to accelerate through at least 2028 and beyond.

Want to know what kind of rapid contract wins and ambitious margin expansion drive this high-value call? The real story is hidden behind unprecedented project backlogs and bold future growth bets. Curious about the financial forecasts that set this valuation apart? Click through to see the narrative’s surprisingly aggressive assumptions in detail.

However, a heavy reliance on U.S. government funding and challenges with integrating acquisitions may quickly undermine these optimistic growth assumptions.

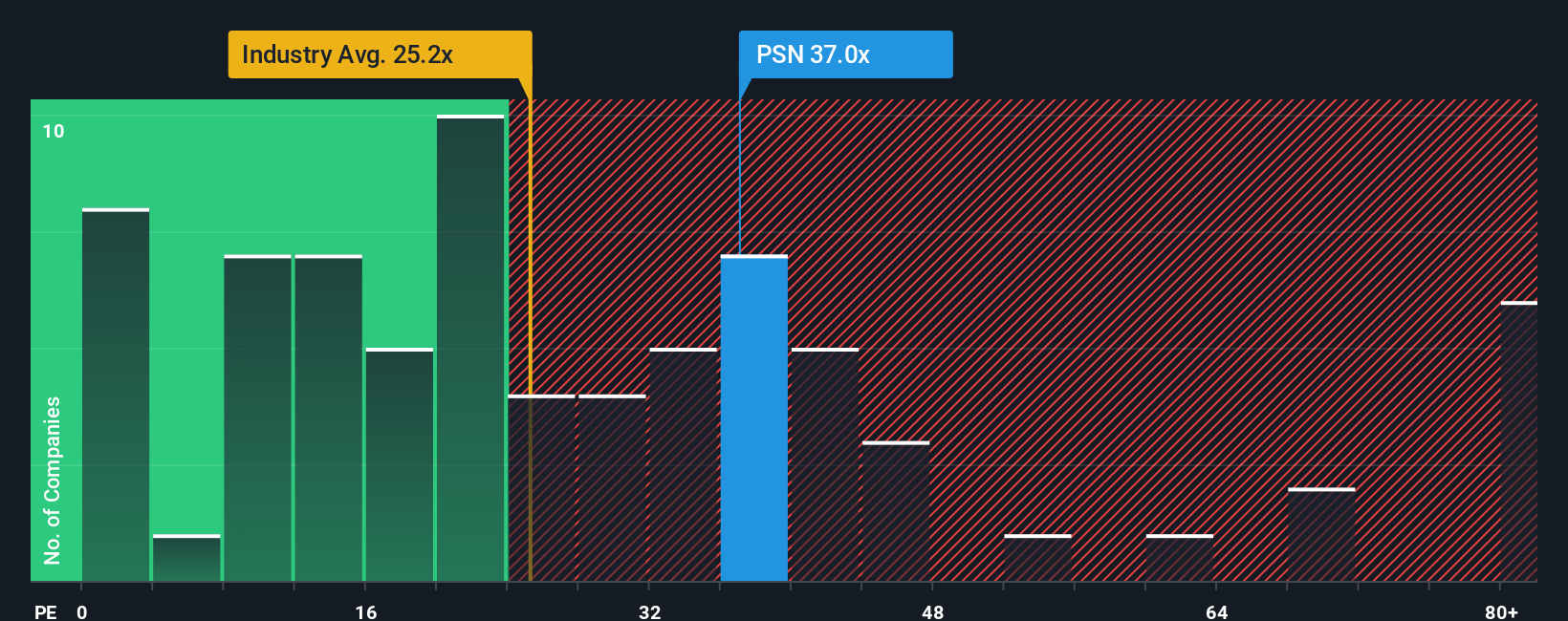

Looking at Parsons through a different lens, its price-to-earnings ratio of 35.9x stands noticeably higher than the industry average of 25.4x and above the fair ratio of 24.8x that the market could move towards. This suggests the stock is expensive by this measure, hinting at valuation risk if market sentiment shifts. Could investor confidence alone keep this premium afloat?

If you see things differently or want to dive deeper into the data yourself, you can craft your own Parsons narrative in just a few minutes. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Parsons.

Looking for more investment ideas?

Uncover unique opportunities by using the Simply Wall Street Screener. Give yourself the edge and don’t let smart moves pass you by. Your next great stock could be just a click away.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Provides integrated solutions and services in the defense, intelligence, and critical infrastructure markets in North America, the Middle East, and internationally.