Advertisement

- United States

- /

- Professional Services

- /

- NYSE:MAN

ManpowerGroup Inc. (NYSE:MAN) is Cheap, but Possibly for Good Reason

ManpowerGroup Inc. (NYSE:MAN), received a lot of attention from a substantial price movement on the NYSE over the last few months, increasing to US$124 at one point, and dropping to the lows of US$101. The new earnings report, and the updated guidance, put downward pressure on the price. We will examine why investors might have mixed sentiment on the stock.

Starting with the latest results, the third quarter showed improvement, but the low profit margin can be off-putting for many investors:

- Revenue: US$5.14b (up 12% from 3Q 2020).

- Net income: US$97.7m (up US$87.4m from 3Q 2020).

- Profit margin: 1.9% (up from 0.2% in 3Q 2020).

Some share price movements can give investors a better opportunity to enter into the stock, and potentially buy at a lower price. A question to answer is whether ManpowerGroup's current trading price of US$101 reflective of the actual value of the mid-cap?

View our latest analysis for ManpowerGroup

What is ManpowerGroup worth?

ManpowerGroup is still a bargain right now according to how current earnings are priced.

We can compare the company's price-to-earnings ratio to the industry average. The stock’s ratio of 15.81x is currently well-below the industry average of 26.54x, meaning that it is trading at a cheaper price relative to its peers.

We should know that we are working with a highly volatile company, as ManpowerGroup’s beta of 2.11 (a measure of share price volatility) is high, meaning its price movements will be exaggerated relative to the rest of the market. If the market is bearish, the company’s shares will likely fall by more than the rest of the market, providing a prime buying opportunity.

Taking into account both the beta and the P/E metrics, we see that the company is both meaningfully underpriced, and has the ability to generate high price movements coming from small changes in expectations.

This leads us to ask ourselves, what are the potential risks for investing?

We can observe a few possible obstacles to future development and long-term potential:

- The company is in a mature phase of its development, however it operates in a very dynamic industry that favors flexibility and innovation. Specifically, the cost of creating the HR infrastructure software is considerably lower and new disruptor apps may present significant competition in this space. At the same time, the mature structure of the company makes it harder to implement fresh, fast-paced changes to their application side of the business.

- The job market is in a cyclical phase, where workers are harder to find, and companies have a hiring problem, which makes Manpower's services less valuable in contrast to when companies need selection services because of higher unemployment.

- Competitors like LinkedIn - Microsoft (NASDAQ:MSFT), and Coursera (NYSE:COUR) are taking on multiple aspects of the business: such as: hiring, training, certification, review, selection.

Further, we should consider, how analysts view the future financial performance of the company, in order to get both a qualitative and qualitative picture for the company.

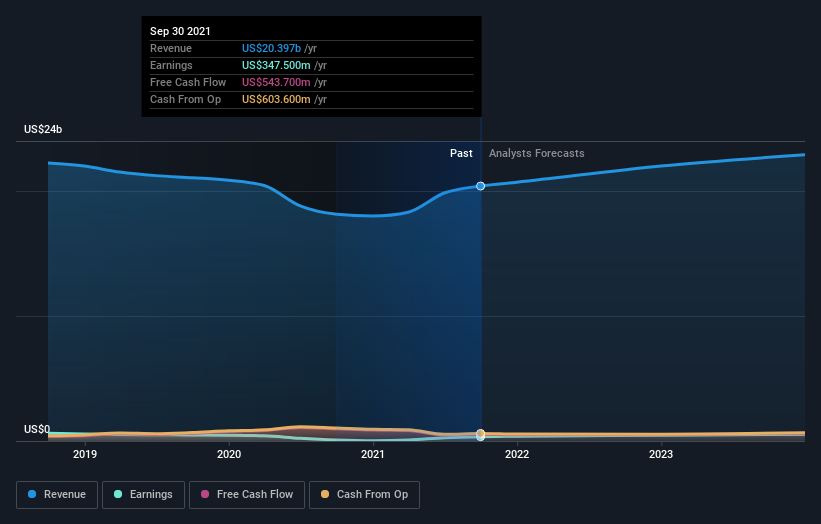

What kind of growth will ManpowerGroup generate?

In the chart below, we can see that analysts are optimistic on the rebound of growth for Manpower, in the very least, this can give investors some sense of stability.

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio.

With profit expected to grow by 72% over the next couple of years, the future seems bright for ManpowerGroup. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What this means for you:

The company seems to be fundamentally underpriced, however is having difficulties keeping up with competitors and technological developments, which might be the reason why it is trading with a high measure of risk.

Are you a shareholder? Since MAN is currently below the industry PE ratio, it may be a great time to hold on to your stock. With a positive outlook on the horizon, it seems like this growth has not yet been fully factored into the share price. However, there are other factors such as capital structure to consider, which could explain the current price multiple.

Are you a potential investor? Its prosperous future profit outlook isn’t fully reflected in the current share price yet, which means it’s not too late to buy MAN. But before you make any investment decisions, consider other factors such as the track record of its management team, in order to make a well-informed investment decision.

If you'd like to know more about ManpowerGroup as a business, it's important to be aware of any risks it's facing. Case in point: We've spotted 1 warning sign for ManpowerGroup you should be aware of.

If you are no longer interested in ManpowerGroup, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NYSE:MAN

ManpowerGroup

Provides workforce solutions and services under the Talent Solutions, Manpower, and Experis brands worldwide.

Very undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor