Advertisement

- United States

- /

- Professional Services

- /

- NYSE:FVRR

Fiverr (FVRR): Exploring Valuation After Strong Q3 Results and Updated Revenue Guidance

Simply Wall St

Reviewed by Simply Wall St

Fiverr International (FVRR) posted stronger financial results for the third quarter, reporting higher revenue and net income compared to last year. The company also shared new guidance for the next quarter and full year.

See our latest analysis for Fiverr International.

Fiverr International’s share price has faced pressure this year, with a year-to-date decline of 34.8%. Even with recent upgrades to revenue guidance and strong third quarter results, momentum has remained weak, and the one-year total shareholder return stands at -29.6%. These swings reflect ongoing questions about growth potential and market positioning, even though the company’s fundamentals are improving.

If you’re weighing what else might offer compelling upside, it’s a great time to broaden your search and discover fast growing stocks with high insider ownership

With shares trading at a steep discount to analyst targets and new earnings guidance announced, investors are left to wonder: is Fiverr now undervalued, or is the market already factoring in the company’s forward growth prospects?

Most Popular Narrative: 39.3% Undervalued

According to Bejgal, the most widely followed narrative sees Fiverr International's fair value significantly above the recent close. Investors are now questioning if projected growth and AI-driven expansion genuinely justify this higher valuation.

Fiverr International’s introduction of AI-powered tools such as Dynamic Matching and Neo (AI-powered smart matching) is expected to significantly enhance sales and earnings. These tools cater to businesses requiring tailored and complex projects, leading to larger transactions. For instance, projects utilizing these tools are reported to be several times larger than typical projects on the platform. Additionally, Fiverr Pro has been instrumental in capturing enterprise budgets, with buyers spending over $10,000 annually continuing to grow, contributing to an overall 9% year-over-year increase in spend per buyer, which reached $296 in Q3 2024.

Curious about the math behind this lofty price tag? The narrative hints at a bold path with rapid profit expansion and a major leap in revenue quality. Uncover which strategic business shifts and financial projections may be driving this potent value estimate. Discover the full calculation that backs this outlook.

Result: Fair Value of $34.41 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, slower adoption of Fiverr’s new AI tools or continued weakness among small business clients could undermine the optimistic outlook for robust long-term growth.

Find out about the key risks to this Fiverr International narrative.

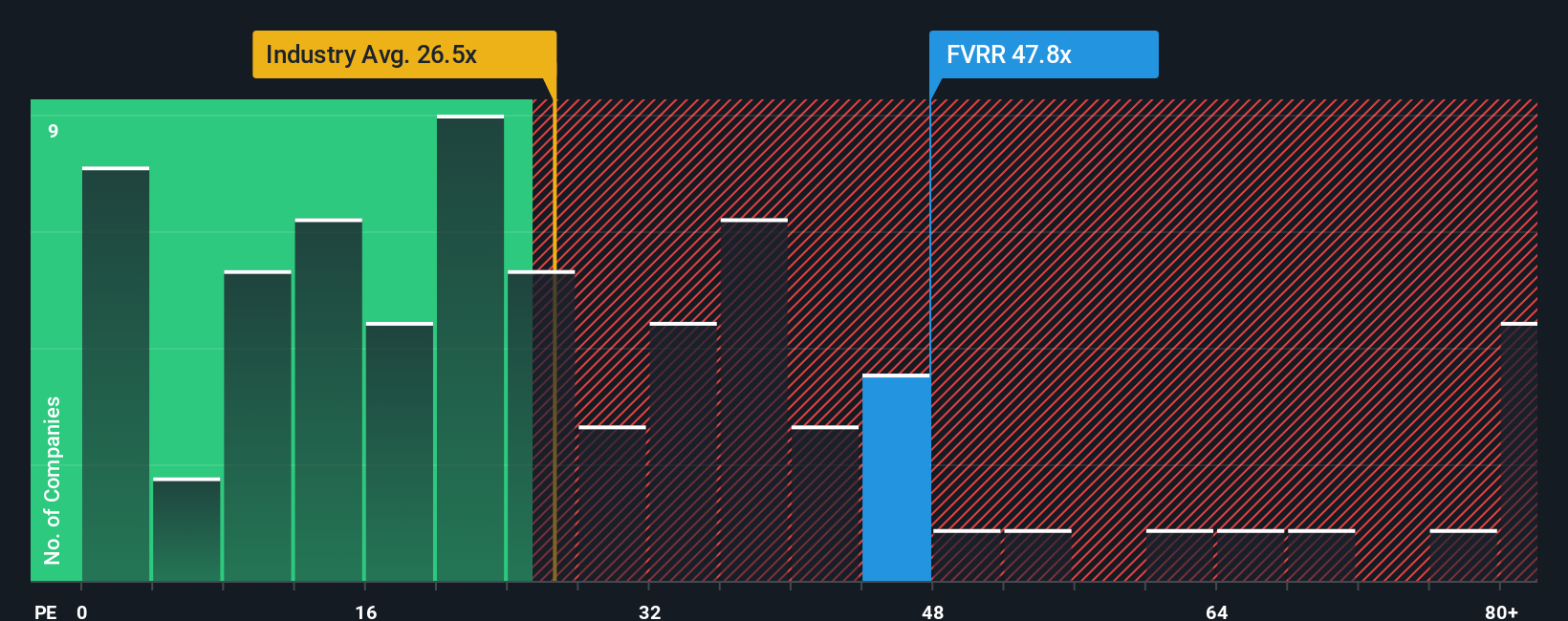

Another View: Price-To-Earnings Tells a Different Story

Looking at Fiverr International’s valuation through the lens of earnings multiples brings some doubts. The company trades at a price-to-earnings ratio of 34.5x, noticeably higher than both the US Professional Services industry average of 24.5x and the peer average of 33.2x. Even compared to its own fair ratio of 33.7x, shares appear a bit expensive. This raises questions about whether the market is betting too much on future growth or if there is real substance behind the optimism.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Fiverr International Narrative

If you see things differently or want to dive deeper into the numbers on your own, you can develop your own take in just a few minutes. Do it your way

A great starting point for your Fiverr International research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don’t limit yourself to just one opportunity. Give yourself a head start by checking out fast-moving stocks and emerging trends investors are buzzing about right now.

- Start building income for your future as you browse these 16 dividend stocks with yields > 3%, which consistently pay yields above 3% and help boost your long-term returns.

- Get ahead of the market by checking out these 24 AI penny stocks, featuring companies at the forefront of artificial intelligence with game-changing growth potential.

- Find compelling bargains and position yourself for upside by screening through these 870 undervalued stocks based on cash flows based on powerful cash flow metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FVRR

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.8% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor