BrightView Holdings (BV) has seen its stock move in recent weeks, capturing some renewed attention from investors looking at the company's performance. With a range of landscaping services across the US, questions continue around its current valuation.

BrightView's share price has seen some ups and downs lately, with a 3.61% gain over the past week and a modest 2.44% rise in the last month. However, the stock is still trending lower for the year, with a -20.38% year-to-date share price return and a -26.2% total shareholder return over twelve months. Momentum appears to be fading compared to the company's impressive 86.4% total return over three years. This puts the recent slip in perspective as investors weigh long-term growth potential against near-term valuation concerns.

With recent gains but a longer-term downward trend, investors are left to wonder if BrightView is trading at a discount to its true value or if the market has already factored in all of its future growth prospects.

Advertisement

Most Popular Narrative: 26% Undervalued

BrightView Holdings is trading at $12.62, noticeably below the narrative’s fair value estimate of $17.06. This prompts a compelling debate over whether the market is overlooking the long-term catalysts described by analysts.

The company’s focus on expanding development operations into new markets where they already have a maintenance presence, aiming to open 10 branches over the next 24 months and capitalize on its $1.2 billion project backlog, positions BrightView to benefit from continued urban growth and rising demand for green spaces. This may support significant future revenue growth.

Want to know what’s powering this bullish view? The real story centers on bold projections for growth, margin expansion, and a future profit multiple that stands out against industry norms. Find out which assumptions drive this fair value and whether the numbers really support such optimism.

However, continued headwinds in project conversions and persistent labor pressures could challenge BrightView’s ability to sustain its growth and margin expansion story.

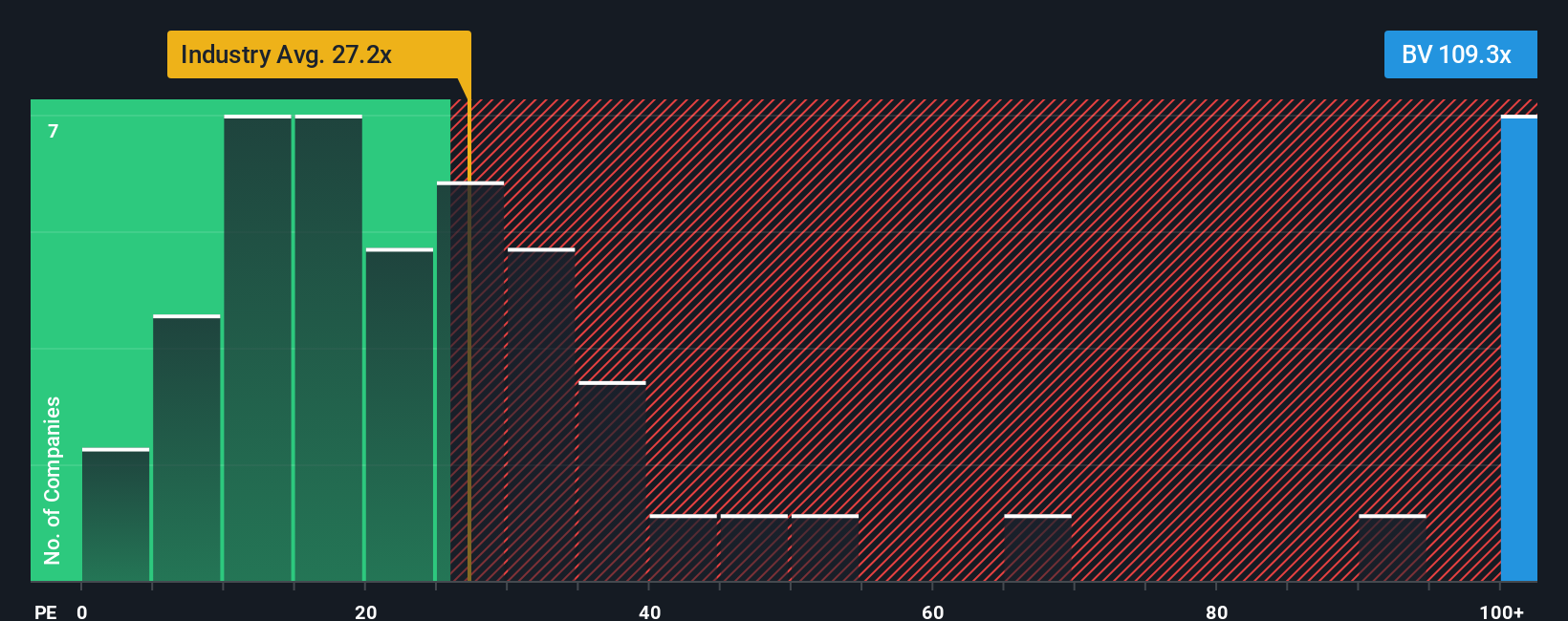

While BrightView may look undervalued based on fair value estimates, using the market’s price-to-earnings ratio paints a different picture. At 93.4x, its ratio is far higher than both the industry average of 22.6x and its peer average of 29.5x. Even compared to a fair ratio of 46.2x, the stock appears expensive. This suggests investors are paying a premium for future growth, but also face meaningful downside risk if growth stumbles. Is the optimism justified, or could expectations be running ahead of reality?

If you have your own perspective or want to dig deeper into the numbers, you can shape your own outlook on BrightView in just a few minutes, and Do it your way.

A great starting point for your BrightView Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Smart investors jump on fresh opportunities early. Check out these standout stock ideas, hand-selected for growth, innovation, and real-world impact. Do not let these slip past you.

Capitalize on the future of medicine by targeting these 30 healthcare AI stocks that are transforming patient care and driving advances in health technology.

Position yourself at the forefront of digital finance with these 81 cryptocurrency and blockchain stocks that are set to benefit from the momentum of blockchain and cryptocurrencies.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BrightView Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.