Advertisement

- United States

- /

- Commercial Services

- /

- NYSE:BCO

What Brink's (BCO)'s North America President Resignation Could Mean for Demand and Cash Flow Outlook

Simply Wall St

Reviewed by Simply Wall St

- On August 8, 2025, The Brink’s Company announced that Daniel J. Castillo, Executive Vice President and President of North America, had resigned effective August 29, 2025, to pursue another opportunity.

- This leadership change comes amid recent concerns around slowing demand and rising capital investment needs, as indicated by the company’s declining revenue growth and free cash flow margin.

- We’ll examine how executive turnover, alongside softness in demand, may influence Brink’s outlook and investment narrative.

This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

Brink's Investment Narrative Recap

Shareholders in Brink’s tend to believe in its ability to grow earnings through expansion in ATM Managed Services (AMS) and Digital Retail Solutions, boosting higher-margin recurring business. The recent resignation of the North America president comes at a delicate time, but unless this triggers a broader leadership disruption, it is unlikely to materially alter the current short-term catalyst, accelerating digital and international revenue, or the biggest risk, which remains execution of digital transformation against stiffer competition.

Among recent announcements, Brink’s buyback program stands out. The company has repurchased over 985,000 shares for US$121.4 million since April 1, 2025, exemplifying its capital return focus. This action is especially relevant given ongoing debates about whether capital would be better spent on technology upgrades, a discussion made more urgent as the AMS and DRS business lines become central to Brink’s growth narrative.

By contrast, investors should pay close attention to whether elevated capital expenditures for technology modernization could...

Read the full narrative on Brink's (it's free!)

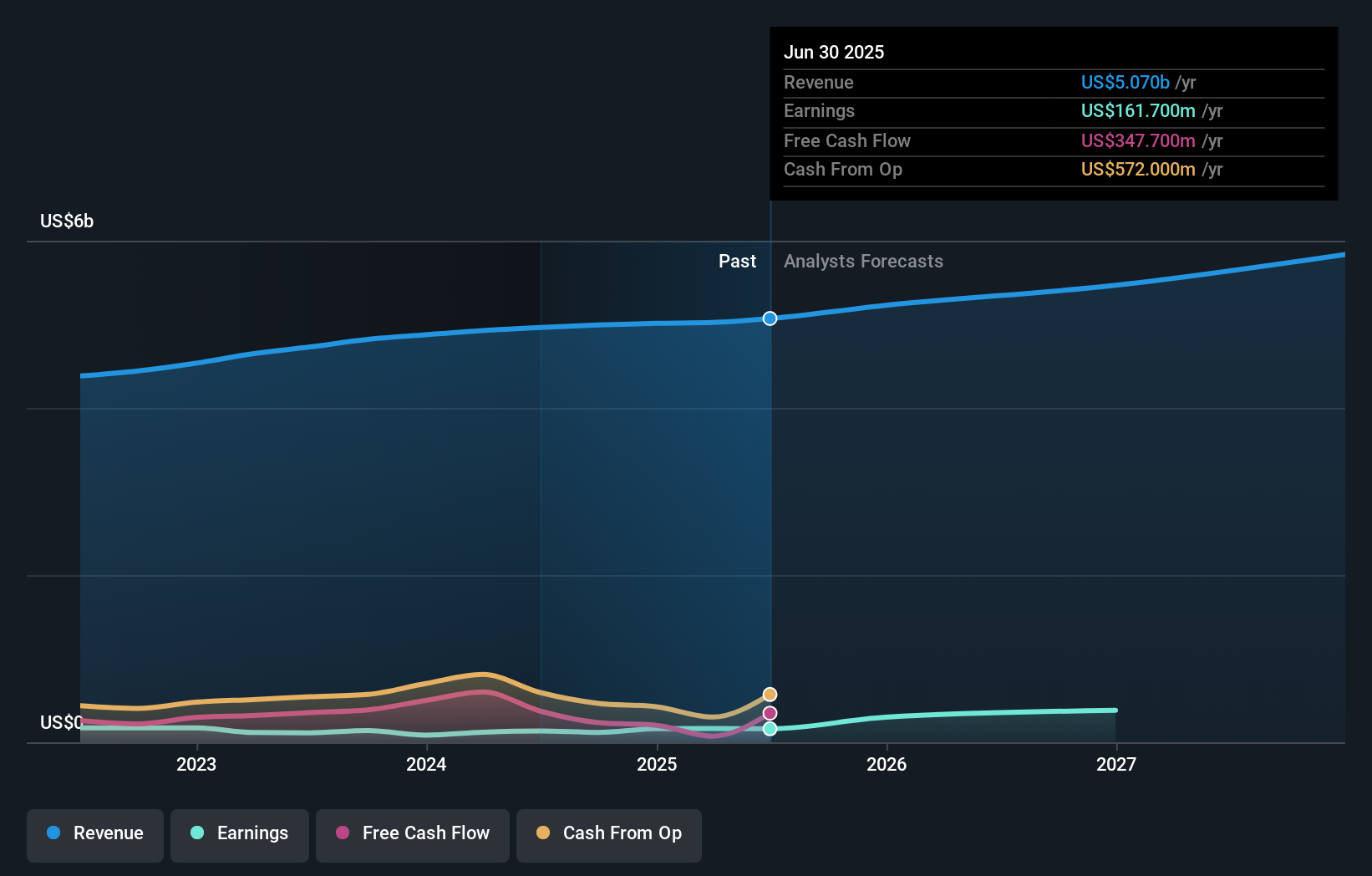

Brink's narrative projects $6.0 billion revenue and $755.1 million earnings by 2028. This requires 5.5% yearly revenue growth and a $593.4 million increase in earnings from $161.7 million currently.

Uncover how Brink's forecasts yield a $128.50 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community estimates for Brink’s fair value range from US$58.27 to US$128.50 across three different analyses. Against this backdrop, ongoing buybacks amid mounting tech investment needs raise further questions about long-term capital priorities and margin trends.

Explore 3 other fair value estimates on Brink's - why the stock might be worth 49% less than the current price!

Build Your Own Brink's Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Brink's research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Brink's research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Brink's overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- AI is about to change healthcare. These 28 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Brink's might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BCO

Brink's

Provides cash and valuables management, digital retail solutions, and automated teller machines (ATM) managed services in North America, Latin America, Europe, and internationally.

Proven track record average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|20.3% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|54.2% overvalued

RO

Community Contributor