- United States

- /

- Trade Distributors

- /

- NYSE:WSO

Watsco (NYSE:WSO) Reports Lower Q1 Earnings With Sales Of US$1,531 Million

Reviewed by Simply Wall St

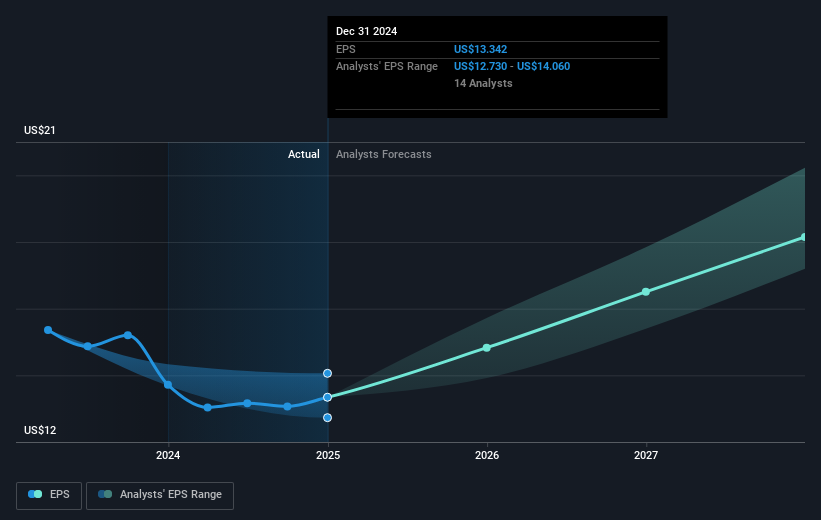

Watsco (NYSE:WSO) recently reported a decline in its first-quarter 2025 financial results, with sales dropping to USD 1,531 million from USD 1,565 million, and net income decreasing to USD 80 million from USD 87 million compared to the same period last year. This negative earnings report coincides with a 10% price decline over the past week, a movement significantly different from broader market trends which showed a 2.3% increase. Despite positive market sentiment fueled by major companies' earnings and tariff development anticipation, the company's disappointing quarterly results understandably weighed on its stock performance.

Buy, Hold or Sell Watsco? View our complete analysis and fair value estimate and you decide.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

The recent decline in Watsco's first-quarter 2025 financial results, with sales down to US$1.53 billion and net income decreasing to US$80 million, casts a spotlight on the company's ongoing challenges. This comes at a time when its shares have seen a 10% decline over the past week, diverging from broader market trends that reflected a 2.3% increase. This disappointing performance may create further headwinds for Watsco's anticipated transition to A2L products, which are crucial for future revenue and margin improvements. Furthermore, the reported figures could impact analysts' current revenue and earnings forecasts, highlighting potential adjustments to the anticipated growth rates and profit margins.

Over the past five years, Watsco's total shareholder return rose 215%, underscoring a robust long-term performance against the backdrop of recent challenges. However, over the past year, its market performance was not as strong, particularly as it underperformed the US market, which returned 3.6%. The company's price movement, with its current share price at US$503.16, appears relatively close to the analyst's consensus price target of US$484.18, indicating that many analysts view the stock as fairly valued at present. However, the recent negative earnings results could lead to reassessments, affecting perceived fair value and investor sentiment.

Unlock comprehensive insights into our analysis of Watsco stock in this financial health report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Watsco might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WSO

Watsco

Engages in the distribution of air conditioning, heating, and refrigeration equipment, and related parts and supplies in the United States, Canada, Latin America, and the Caribbean.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives