Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:WCC

WESCO International (WCC): Evaluating Valuation After Upbeat Q3 Results and Upgraded Sales Outlook

Simply Wall St

Reviewed by Simply Wall St

WESCO International (WCC) jumped into focus after outperforming in the third quarter of 2025 and raising its full-year sales outlook, highlighting momentum in segments such as data centers and electrification.

See our latest analysis for WESCO International.

WESCO International’s strong third-quarter results and upgraded growth outlook have reignited investor enthusiasm, reflected in a 25.4% one-month share price return and a 50% gain year-to-date. With a 30.3% total shareholder return over the past year, performance momentum is clearly building as strategic buybacks and rising demand in key business segments take the spotlight.

If you’re watching how rapidly shifting business trends drive outperformance, now is a great opportunity to broaden your search and discover fast growing stocks with high insider ownership

With such a strong run behind it and analyst price targets just a few percent above the current share price, investors now face a familiar question: is WESCO International still undervalued, or is future growth already priced in?

Price-to-Earnings of 20.6x: Is it justified?

Despite a surge in recent returns for WESCO International, the stock’s price-to-earnings (P/E) ratio currently stands at 20.6x, which positions it as more expensive than both its industry peers and the broader sector. At the last close of $267.15, investors are paying a premium compared to similar companies.

The price-to-earnings ratio measures what investors are willing to pay for each dollar of earnings, and a higher number often signals market confidence in future profit growth. For a trade distributor like WESCO International, this ratio helps the market weigh current results against anticipated financial momentum, sector trends, and company-specific catalysts.

With WESCO’s P/E exceeding the peer average (19.7x) and the US Trade Distributors industry average (19.9x), the market appears eager to price in continued growth or outperformance. However, relative to the estimated fair P/E ratio of 29.3x, WESCO actually trades at a discount. This creates a valuation gap that could close if the company delivers on its profit forecasts and strategic ambitions.

Explore the SWS fair ratio for WESCO International

Result: Price-to-Earnings of 20.6x (ABOUT RIGHT)

However, persistent sector volatility or unexpected shifts in demand could quickly alter WESCO International’s outlook and challenge its current growth narrative.

Find out about the key risks to this WESCO International narrative.

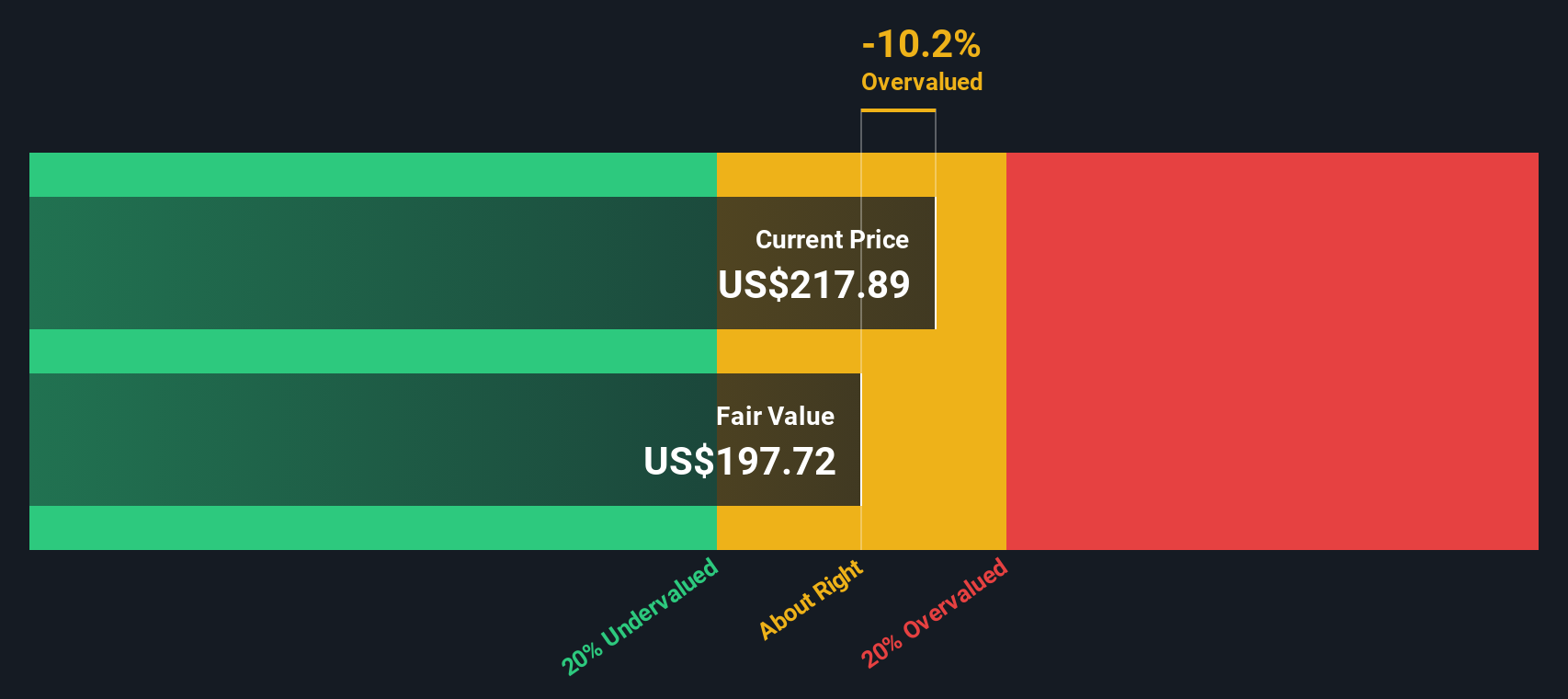

Another View: What Does the SWS DCF Model Suggest?

While multiples point to WESCO International trading at a premium to peers, our DCF model offers a different perspective. It estimates fair value at $285.87, about 6.6% above the current price. This suggests the stock is undervalued. Could the market be overlooking future earnings potential?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out WESCO International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 862 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own WESCO International Narrative

If you want to dig deeper or believe your perspective could lead to a different conclusion, it takes just a few minutes to build your own view. Do it your way

A great starting point for your WESCO International research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let big opportunities pass you by. Use the Simply Wall Street Screener to pinpoint stocks that fit your strategy and capture tomorrow’s winners before others do.

- Capture steady income and reliable returns by tapping into these 14 dividend stocks with yields > 3% with high yields and strong fundamentals.

- Unlock the future of medicine and patient care by searching these 32 healthcare AI stocks that are revolutionizing healthcare through artificial intelligence.

- Ride the potential wave of digital assets when you browse these 82 cryptocurrency and blockchain stocks making headlines in blockchain and cryptocurrency innovation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if WESCO International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WCC

WESCO International

Provides business-to-business distribution, logistics services, and supply chain solutions in the United States, Canada, and internationally.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor