Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:WCC

How Surging Data Center Demand and Share Buybacks Could Reshape WESCO International’s (WCC) Growth Narrative

Simply Wall St

Reviewed by Sasha Jovanovic

- WESCO International reported stronger-than-expected third-quarter 2025 earnings, featuring US$6.20 billion in sales and increased full-year guidance for organic sales growth and profitability.

- The company highlighted significant growth in the data center segment and completed a major share buyback program totaling over 3.4 million shares for US$587.39 million.

- We'll explore how WESCO's raised sales outlook, driven by robust data center demand, influences the company's current investment narrative.

This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

What Is WESCO International's Investment Narrative?

WESCO International's recent third-quarter results give investors new context for weighing the company’s trajectory. The stronger-than-expected US$6.20 billion in quarterly sales and raised full-year guidance for organic sales growth signal that robust demand in the data center segment is pushing performance forward. Completed buybacks of over 3.4 million shares for nearly US$590 million show capital returned to shareholders, supporting confidence in management’s outlook. These catalysts shift the short-term story: raised sales targets and sector momentum could prove material, especially with analyst upgrades following the news. However, earnings slipped year on year, and net profit margins remain slim, so operational execution and margin improvement remain under the spotlight. Management’s experience and sectoral positioning are strengths, but any disruption to technology demand or further margin compression could present fresh risks despite recent positive sentiment.

On the flip side, recent insider selling is something investors shouldn’t ignore when weighing risks.

Exploring Other Perspectives

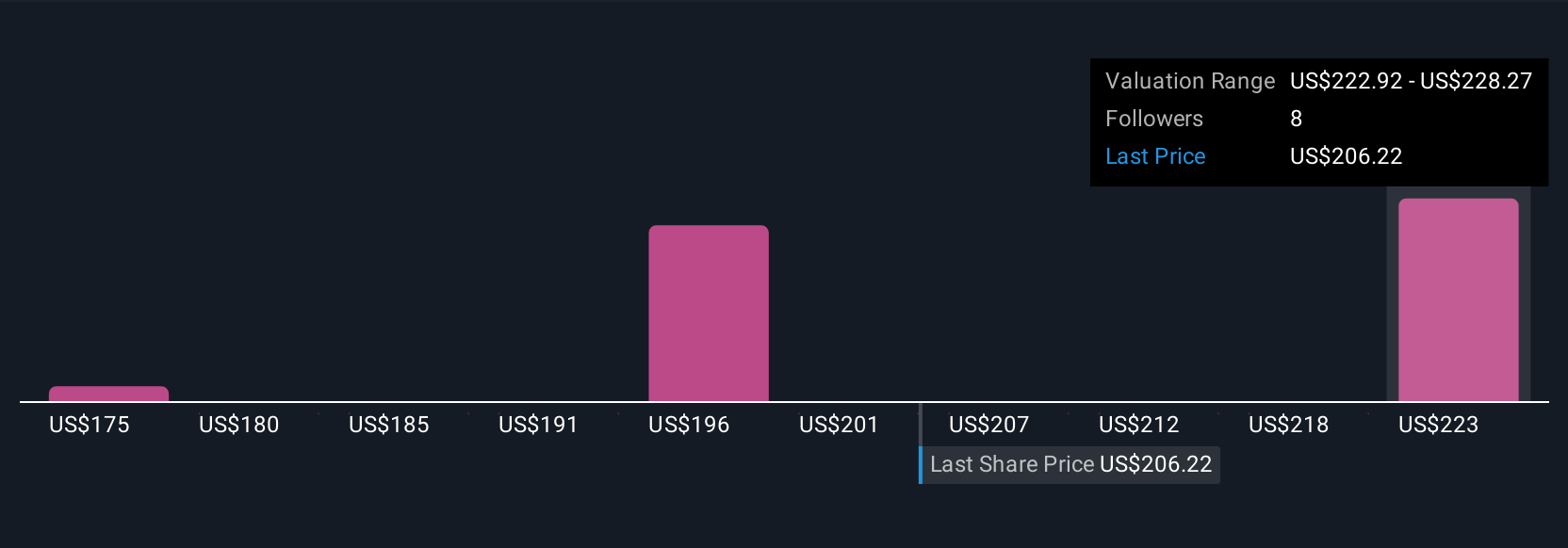

Explore 3 other fair value estimates on WESCO International - why the stock might be worth 32% less than the current price!

Build Your Own WESCO International Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your WESCO International research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free WESCO International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate WESCO International's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if WESCO International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WCC

WESCO International

Provides business-to-business distribution, logistics services, and supply chain solutions in the United States, Canada, and internationally.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor