Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:URI

What United Rentals (URI)'s Raised Guidance and Margin Pressures Mean for Shareholders

Simply Wall St

Reviewed by Sasha Jovanovic

- United Rentals recently reported third quarter 2025 earnings with quarterly revenue of US$4.23 billion and net income of US$701 million, alongside the declaration of a US$1.79 per share dividend and completion of a US$1.03 billion share buyback tranche.

- Although the company raised its full-year revenue guidance, higher fleet repositioning and delivery expenses affected margins, while robust demand from infrastructure and nonresidential construction supported revenue growth.

- We'll examine how United Rentals' increased full-year revenue outlook and expense pressures factor into its current investment narrative.

Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

United Rentals Investment Narrative Recap

To be a United Rentals shareholder, you need to believe in the company’s ability to capitalize on strong infrastructure and nonresidential construction demand while managing cost pressures that impact profitability. The recent news, including a raised full-year revenue outlook and ongoing margin compression from fleet and delivery expenses, does not appear to materially change the most important catalyst, robust project-driven equipment rental demand, or alter the key short-term risk of further margin pressure. Among recent company actions, the completed US$1.03 billion share buyback is most relevant, as it supports earnings per share through share count reduction and highlights ongoing capital return initiatives. This capital allocation move comes as the company continues its focus on balancing growth investments with shareholder returns, linking directly to ongoing investor interest in both profitability and value creation. But even with rising demand, investors should be aware that further increases in repositioning and delivery costs could...

Read the full narrative on United Rentals (it's free!)

United Rentals is projected to reach $18.8 billion in revenue and $3.5 billion in earnings by 2028. This outlook assumes annual revenue growth of 6.1% and a $1.0 billion increase in earnings from the current $2.5 billion.

Uncover how United Rentals' forecasts yield a $1029 fair value, a 18% upside to its current price.

Exploring Other Perspectives

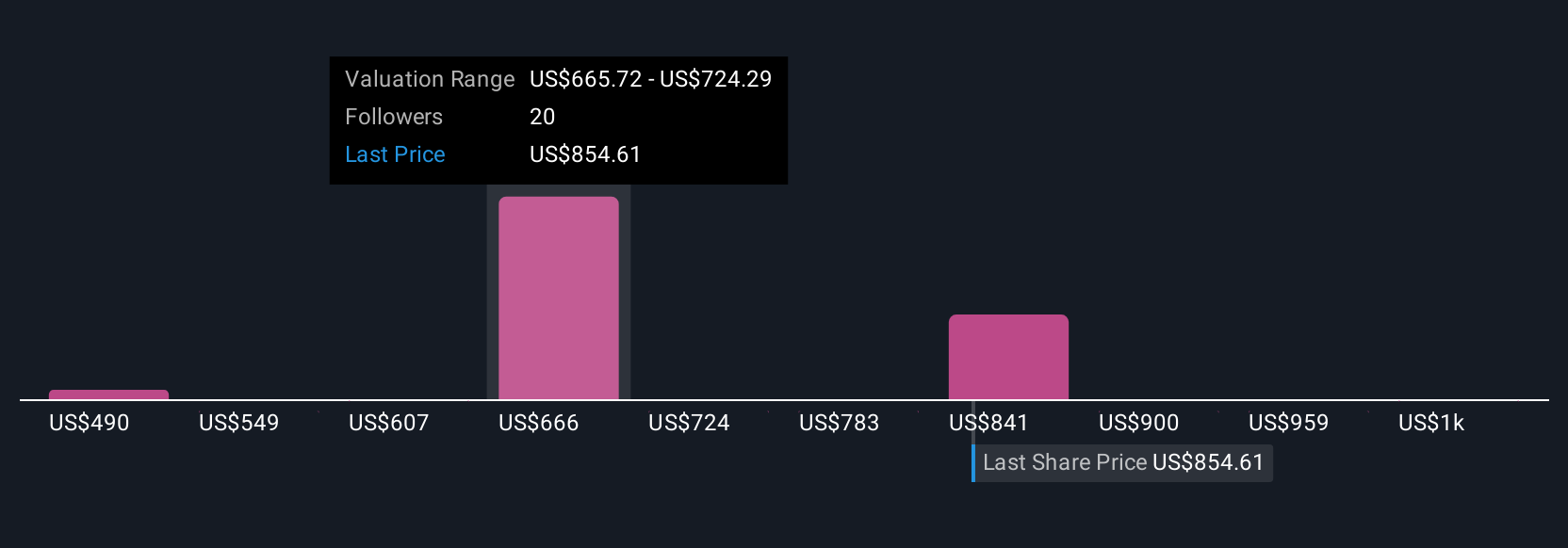

Five Simply Wall St Community fair value estimates for United Rentals range from US$532.90 to US$1,157.42. While these private investor views vary widely, recent margin pressures may give some pause to the company’s future earnings potential.

Explore 5 other fair value estimates on United Rentals - why the stock might be worth as much as 33% more than the current price!

Build Your Own United Rentals Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your United Rentals research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free United Rentals research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate United Rentals' overall financial health at a glance.

Ready For A Different Approach?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- Rare earth metals are the new gold rush. Find out which 37 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:URI

United Rentals

Through its subsidiaries, operates as an equipment rental company.

Good value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor