Advertisement

- United States

- /

- Construction

- /

- NYSE:TPC

Will Q2 Earnings and Estimate Revisions Shift Tutor Perini's (TPC) Narrative?

Simply Wall St

Reviewed by Simply Wall St

- Tutor Perini Corporation announced it will release its second quarter 2025 earnings results and hold a conference call with company leadership on August 6, 2025, after the market closes.

- While analysts anticipate year-over-year earnings growth, recent downward revisions to earnings estimates and a Zacks Rank #4 (Sell) reflect mixed sentiment among investors ahead of the announcement.

- Now, we'll explore how these estimate revisions and upcoming results may influence Tutor Perini's outlook and the existing investment narrative.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Tutor Perini Investment Narrative Recap

Tutor Perini shareholders are typically betting on the company's ability to convert its record US$19.4 billion backlog and upcoming high-margin projects into sustained revenue and profit growth, despite historical volatility and execution risks. The recent announcement of estimate revisions and a Zacks Rank #4 (Sell) may not fundamentally alter the main short-term catalyst, ramp-ups on large new projects, but adds uncertainty to the most important risk: future margin pressure and possible project delays. Of the recent news, securing the US$1.871 billion contract from the Port Authority of New York and New Jersey stands out. This substantial project award directly supports the bullish narrative on backlog-driven growth, offering near-term visibility on revenue streams and enhancing the relevance of the upcoming earnings call for investors watching project ramp-up progress. However, it’s equally important to keep in mind the potential impact if project delays or lower-than-expected win rates materialize, as investors should be aware that...

Read the full narrative on Tutor Perini (it's free!)

Tutor Perini's narrative projects $6.9 billion revenue and $393.4 million earnings by 2028. This requires 15.2% yearly revenue growth and a $544.9 million increase in earnings from the current -$151.5 million.

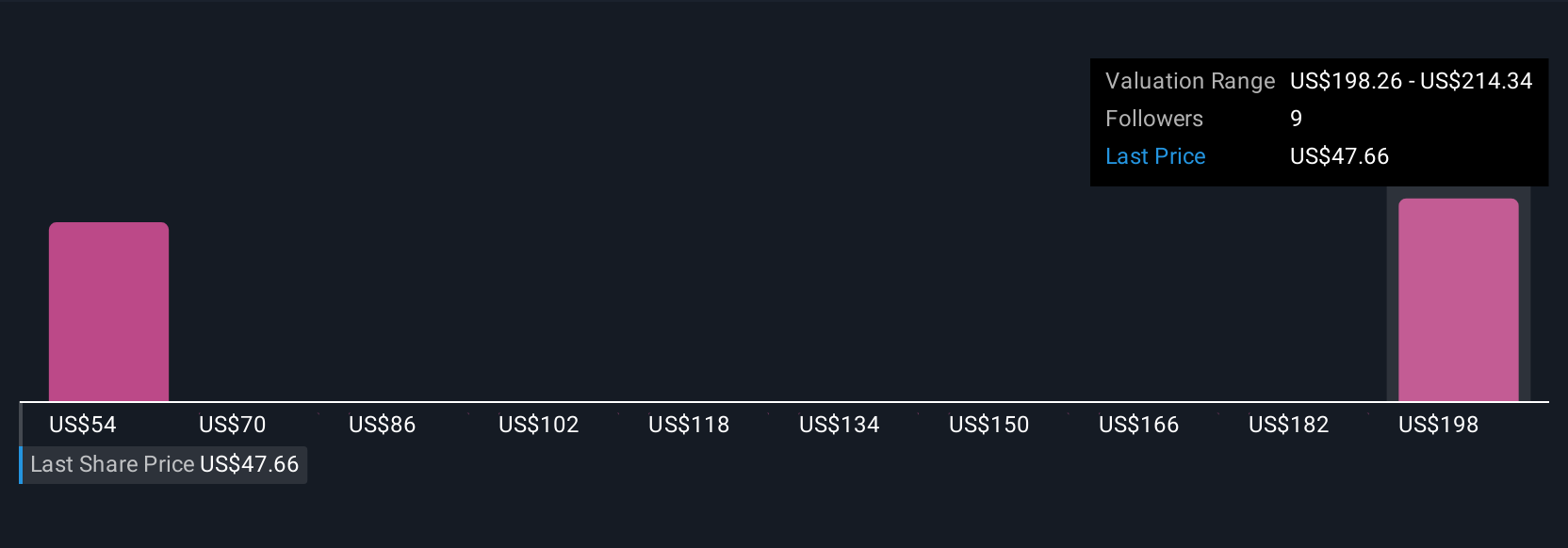

Uncover how Tutor Perini's forecasts yield a $53.50 fair value, a 11% upside to its current price.

Exploring Other Perspectives

Two separate fair value estimates from the Simply Wall St Community range widely between US$53.50 and US$233.34 per share. Despite these differences, concerns about project execution and possible delays remain closely tied to the company’s near-term performance, further underlining why you may want to compare multiple viewpoints.

Explore 2 other fair value estimates on Tutor Perini - why the stock might be worth just $53.50!

Build Your Own Tutor Perini Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Tutor Perini research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Tutor Perini research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tutor Perini's overall financial health at a glance.

Curious About Other Options?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- These 16 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 24 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tutor Perini might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TPC

Tutor Perini

A construction company, provides diversified general contracting, construction management, and design-build services to private customers and public agencies worldwide.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A Quality Compounder Marked Down on Overblown Fears

Fair Value US$120.72|59.6% undervalued

BA

Community Contributor

Wyndham Continues Global Expansion with 19% Ancillary Revenue Growth

Fair Value US$105.80|20.1% undervalued

ZW

Community Contributor