Advertisement

- United States

- /

- Machinery

- /

- NYSE:TNC

Could Tennant’s (TNC) New Scrubber Highlight a Shift in Its Long-Term Innovation Strategy?

Simply Wall St

Reviewed by Sasha Jovanovic

- Tennant Company recently launched the T360 mid-sized scrubber, designed for ease of use, efficient cleaning, and simplified maintenance, with features such as a one-button Stop-Start control and maintenance-free GEL battery for up to three hours of operation.

- This product introduction highlights Tennant's ongoing focus on user-friendly, productivity-oriented design and underscores its commitment to meeting evolving facility maintenance needs.

- We'll explore how the T360's efficiency-driven features may influence Tennant's broader investment narrative and future growth outlook.

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Tennant Investment Narrative Recap

To be a Tennant shareholder, you need to believe the company can sustain growth by innovating in cleaning technology while managing cyclical demand and cost pressures in key regions. The launch of the T360 mid-sized scrubber reinforces Tennant’s productivity-focused strategy, but by itself, it is unlikely to materially alter near-term catalysts, the most important being expansion in equipment-as-a-service and autonomous solutions against a backdrop of slowing sales growth. The primary risk remains vulnerability to regional slowdowns and ongoing competitive threats, which can pressure margins and revenue, especially if new products do not drive meaningful share gains.

Of recent announcements, the introduction of Tennant's Z50 Citadel Outdoor Sweeper stands out, as it broadens the company’s product reach and total addressable market, a relevant development when considering how new launches like the T360 may fit into the wider growth narrative. Both releases emphasize operational efficiency, but whether they can offset slowing demand and drive accelerated adoption in underpenetrated segments will be closely watched by the market.

However, investors should also keep in mind the ongoing challenge of aggressive low-price competition in international markets, something that remains crucially important for anyone looking to...

Read the full narrative on Tennant (it's free!)

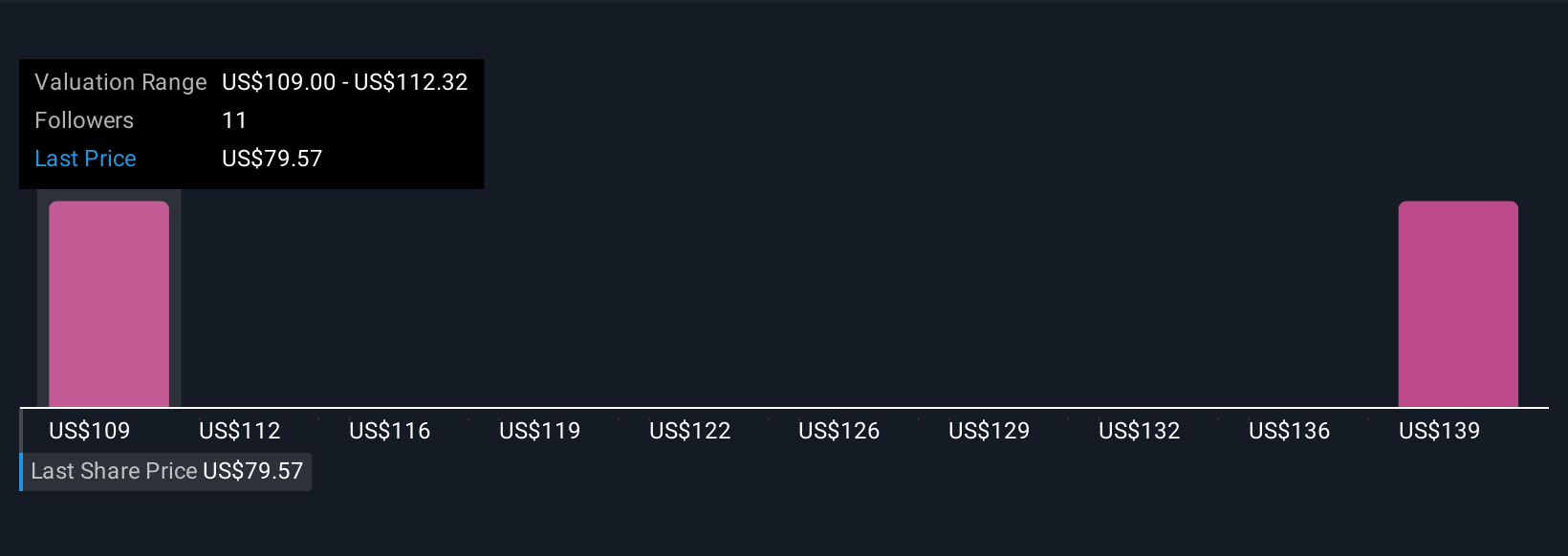

Tennant's outlook suggests revenues of $1.5 billion and earnings of $138.4 million by 2028. This is based on a 5.2% annual revenue growth rate and an increase in earnings of $77.7 million from the current $60.7 million level.

Uncover how Tennant's forecasts yield a $109.00 fair value, a 37% upside to its current price.

Exploring Other Perspectives

Fair value estimates from the Simply Wall St Community all stand at US$109, based on a single perspective before the latest product news. While analyst consensus highlights Tennant’s expansion in new offerings, slower sales and competitive concerns still set the tone for broader performance. Compare these viewpoints to expand your own outlook.

Explore another fair value estimate on Tennant - why the stock might be worth as much as 37% more than the current price!

Build Your Own Tennant Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Tennant research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Tennant research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Tennant's overall financial health at a glance.

Interested In Other Possibilities?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tennant might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TNC

Tennant

Designs, manufactures, and markets floor cleaning equipment in the Americas, Europe, the Middle East, Africa, and the Asia Pacific.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor