Advertisement

- United States

- /

- Construction

- /

- NYSE:PRIM

Why Is Primoris Services (PRIM) Up After Raising Guidance and Posting Strong Quarterly Results?

Simply Wall St

Reviewed by Sasha Jovanovic

- Primoris Services Corporation recently raised its earnings guidance for 2025, announced a quarterly dividend, and reported higher third-quarter sales and net income compared to the same period last year.

- Significantly improved financials and the updated earnings outlook highlight growing momentum across Primoris's core infrastructure and renewables segments.

- We’ll explore how Primoris’s raised earnings guidance and robust earnings results could influence its future growth expectations and investment narrative.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Primoris Services Investment Narrative Recap

To be a Primoris Services shareholder, you need to believe in the company’s ability to maintain double-digit earnings growth by capitalizing on robust demand across renewables and data center infrastructure, while navigating margin pressures and the competitive nature of these markets. The recent boost in 2025 earnings guidance, combined with outperformance in Q3, reinforces the current growth catalyst but does not remove the risk of significant margin headwinds in renewables, which remains the key threat to near-term profitability.

Among the recent developments, the raised corporate earnings guidance is particularly relevant. By targeting net income of US$260.5 million to US$271.5 million, management is signaling confidence in sustained momentum from its renewables and infrastructure pipeline, which could extend the company’s earnings trajectory and reinforce investor expectations tied to sector growth drivers.

But despite these tailwinds, investors should be mindful that persistent margin pressures in renewables could still...

Read the full narrative on Primoris Services (it's free!)

Primoris Services is projected to reach $8.7 billion in revenue and $358.2 million in earnings by 2028. This outlook assumes 7.7% annual revenue growth and a $117.2 million increase in earnings from the current $241.0 million.

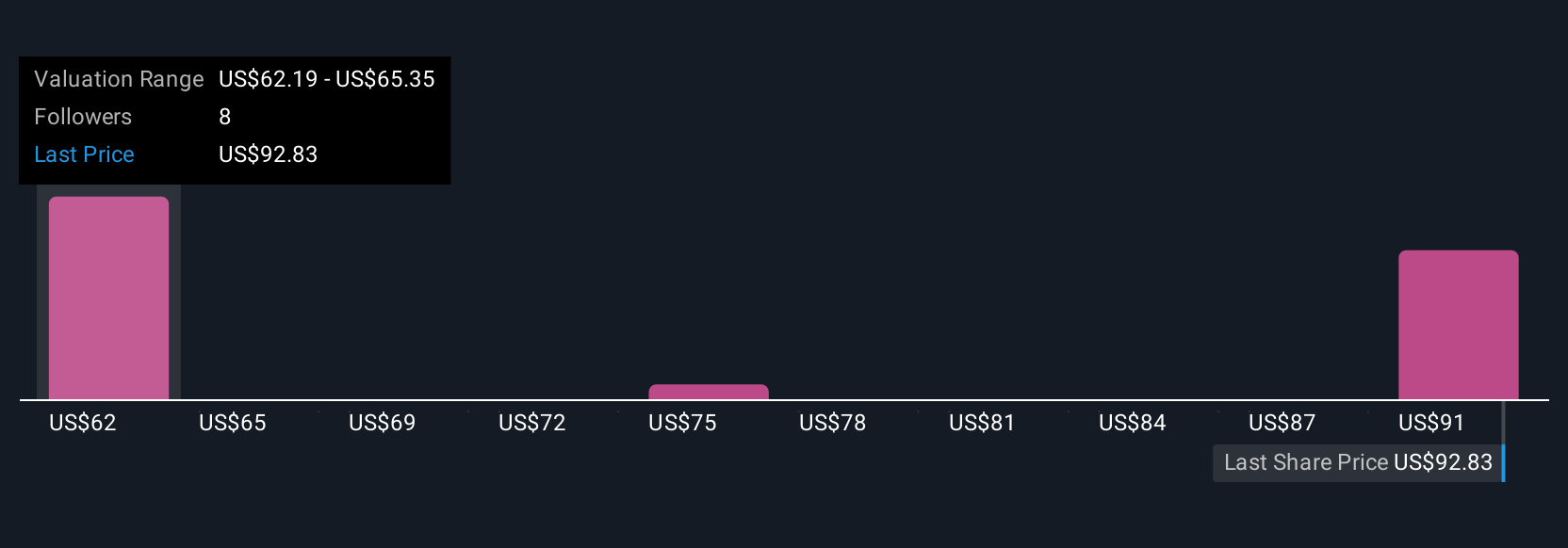

Uncover how Primoris Services' forecasts yield a $153.36 fair value, a 30% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community’s fair value estimates for Primoris Services range from US$77.76 to US$153.36, based on four independent forecasts. Given ongoing competitive risks in renewables, you’ll find a wide range of market views worth considering as you shape your outlook on the company’s performance.

Explore 4 other fair value estimates on Primoris Services - why the stock might be worth as much as 30% more than the current price!

Build Your Own Primoris Services Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Primoris Services research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Primoris Services research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Primoris Services' overall financial health at a glance.

Searching For A Fresh Perspective?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 37 best rare earth metal stocks of the very few that mine this essential strategic resource.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PRIM

Primoris Services

Provides infrastructure services primarily in the United States and Canada.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor