Advertisement

- United States

- /

- Industrials

- /

- NYSE:MMM

Does 3M’s Recent PFAS Settlement Signal Opportunity for Investors in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Curious whether 3M stock is truly a bargain or just looks cheap? If you want to catch a good value buy, you need to know what’s under the hood.

- 3M’s share price has gained 2.5% in the last week and has risen 31.7% so far this year, sending a clear signal that investors are paying attention to its potential.

- Recent headlines have focused on 3M’s legal settlement over PFAS “forever chemicals” along with the ongoing spin-off of its healthcare business. Both developments have played a role in driving recent price movements. Investors are closely watching to see how these changes affect the company’s risk and growth outlook.

- Currently, 3M scores just 2 out of 6 on our undervaluation checks. We are taking a closer look at what this means for value-focused investors, and there may be an even more effective way to assess valuation detailed at the end of this article.

3M scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: 3M Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by forecasting future cash flows and then discounting these amounts back to today’s dollars. This method offers a forward-looking view of what 3M’s business is worth based on actual cash generated over time, rather than simply relying on current profits or accounting measures.

For 3M, its trailing twelve-month Free Cash Flow stands at around $1.25 Billion. Analysts project annual cash flow will grow significantly in the years ahead, reaching approximately $4.90 Billion by 2029. While analyst estimates are only provided for up to five years, further projections adopted by Simply Wall St extrapolate ongoing performance, placing projected Free Cash Flow in 2035 at just above $6.1 Billion. All cash flows are reported in US dollars.

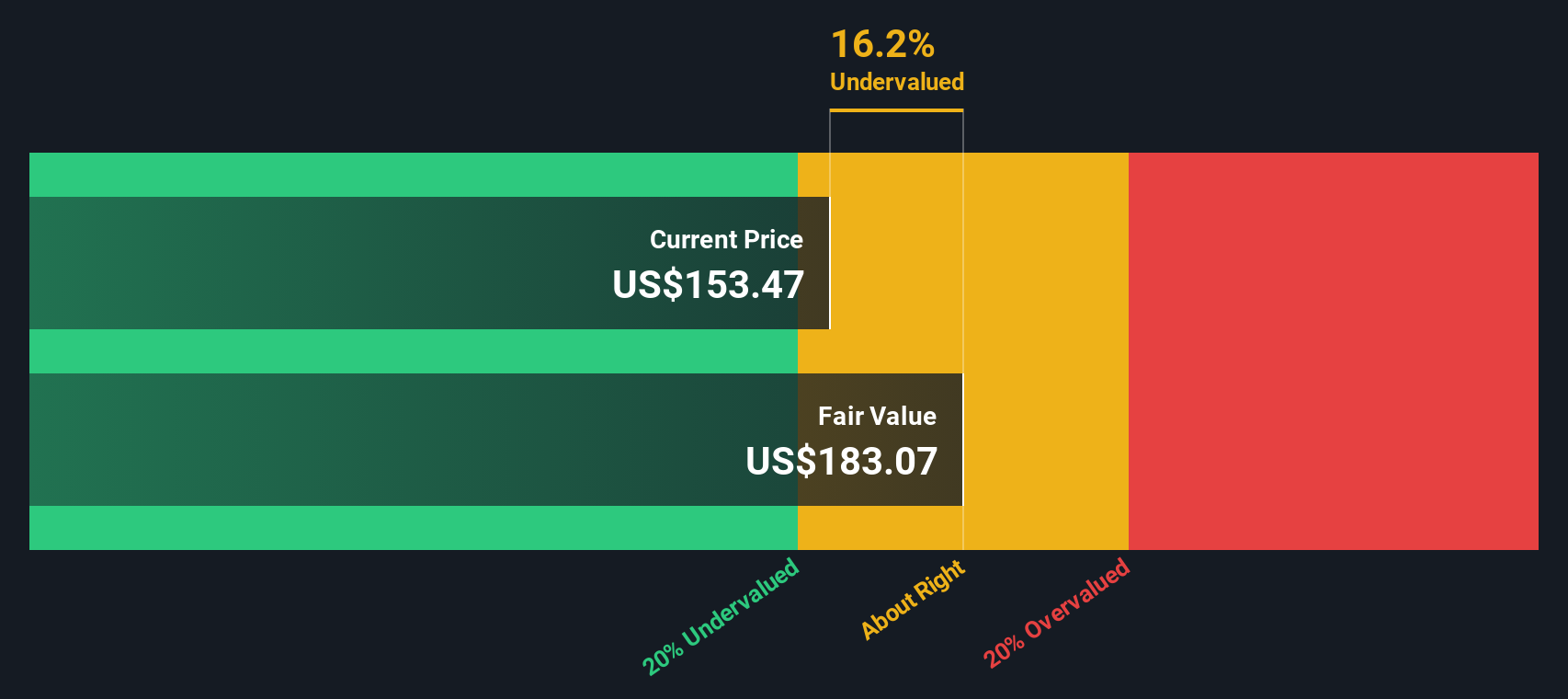

Based on these forecasts, the DCF model calculates an estimated intrinsic value per share of $192.94. This suggests the stock is currently trading at an 11.5% discount to its fair value, indicating it is undervalued according to this analysis.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests 3M is undervalued by 11.5%. Track this in your watchlist or portfolio, or discover 932 more undervalued stocks based on cash flows.

Approach 2: 3M Price vs Earnings (PE)

The price-to-earnings (PE) ratio is a helpful way to judge if a profitable company like 3M is trading at an attractive valuation. For established businesses generating steady profits, the PE ratio provides a simple comparison of what investors are paying per dollar of earnings.

However, what counts as a "normal" or "fair" PE ratio is influenced by more than just profits. Companies with faster growth or lower risk can justify a higher PE, while those facing headwinds, slow growth, or greater uncertainty typically see valuations settle at lower multiples.

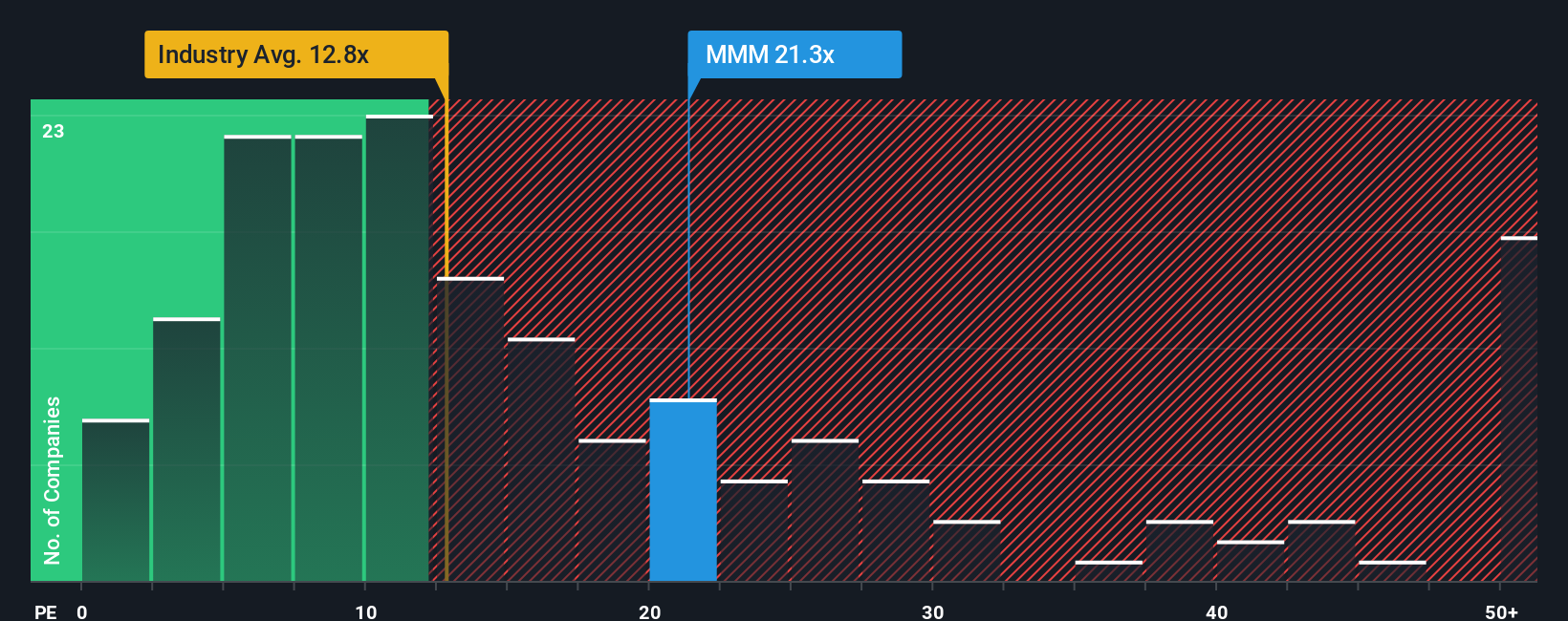

3M’s current PE ratio sits at 26.7x. To put this in context, the average PE ratio of companies in the Industrials sector is just 12.1x. 3M’s closest peers are trading at a comparable 26.2x. This shows that investors are pricing 3M on par with other mature, profitable companies in its peer group, yet at a significant premium to the broader industry average.

Simply Wall St’s “Fair Ratio” goes a step further than standard benchmarks. It is a proprietary measure that reflects not only the company’s sector and profit margins but also its unique earnings growth profile, size, and risk factors. For 3M, the Fair Ratio is calculated at 32.4x, higher than both its current PE and the peer average.

The advantage of using the Fair Ratio is that it adjusts for the nuances that simple peer or industry comparisons can miss. It gives investors a tailored benchmark, considering the realities of 3M’s growth trajectory, risk environment, and financial health. This approach offers a more detailed picture of underlying value.

With 3M’s actual PE ratio below its Fair Ratio, the stock appears to be undervalued on this measure. This may indicate potential upside for investors seeking reasonable value in a quality company.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your 3M Narrative

Earlier we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is a simple yet powerful framework that lets you attach your own story, your perspective on a company’s strategy, risks, and opportunity, to the numbers behind 3M, including your assumptions for fair value, future revenue, earnings, and profit margins.

Narratives bridge the gap between the company’s story and the financial forecast, then link these directly to an estimate of fair value. Rather than relying solely on static numbers, Narratives help you clarify why you believe 3M should be worth more or less by providing context around your expectations, the business outlook, and evolving market events.

On Simply Wall St’s Community page, you’ll find Narratives used by millions of investors. These tools are easy and accessible if you want to build or compare your own investment case. Narratives are updated dynamically whenever important news or company events (like earnings reports) are released, helping you stay responsive in your decision-making process.

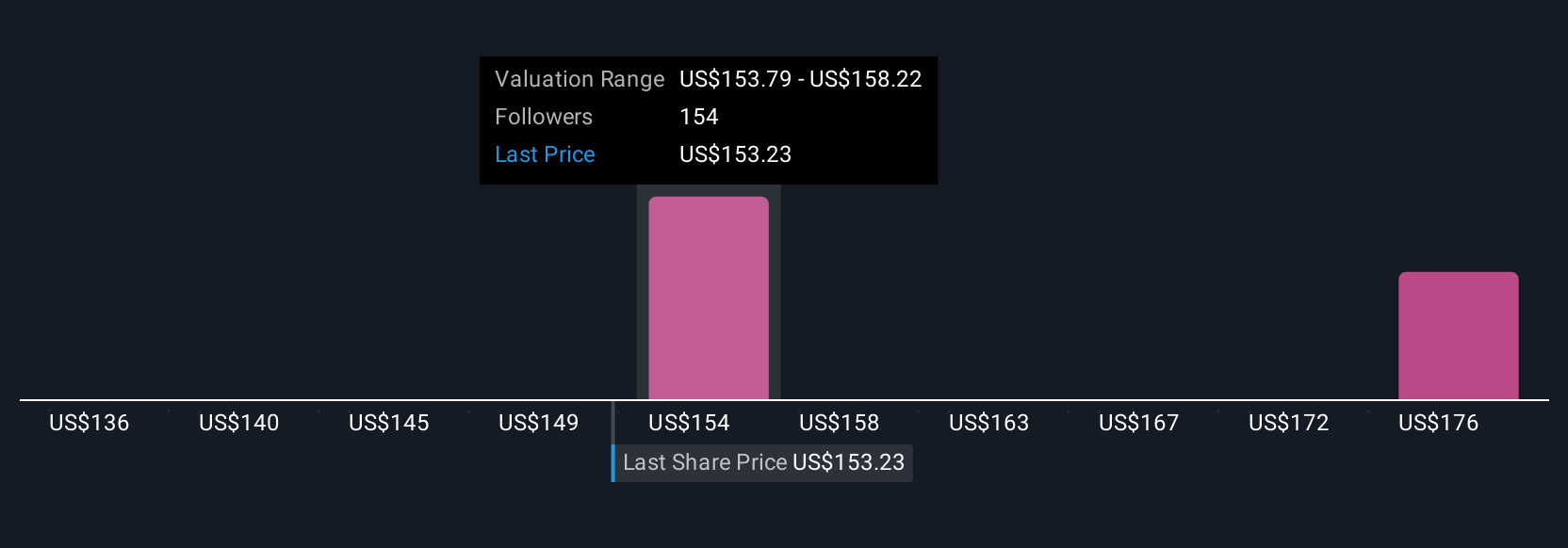

With Narratives, you can clearly see how your estimated Fair Value compares to the current Price, and use this dynamic signal to decide when to buy or sell. For example, if you believe 3M will continue to boost profits through innovation and operational improvement, like the most optimistic analysts projecting a fair value of $187, your outlook might be bullish. Alternatively, if you are concerned about litigation risks and see long-term challenges, your Narrative may align with the most cautious estimate of $101. This demonstrates how Narratives can reflect a wide range of investor views at any time.

Do you think there's more to the story for 3M? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if 3M might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MMM

3M

Provides diversified technology services in the Americas, the Asia Pacific, Europe, the Middle East, Africa, and internationally.

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

92 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative