Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:LMT

Is Winning Germany’s Navy Deal Shaping the Investment Case for Lockheed Martin (LMT)?

Simply Wall St

Reviewed by Sasha Jovanovic

- Germany recently announced that its Navy has selected Lockheed Martin Canada’s CMS 330 combat management system in a deal valued at more than C$1 billion, further expanding Lockheed Martin's global naval presence.

- This contract win highlights both the increasing international demand for advanced defense technology and Lockheed Martin's ability to secure high-value government partnerships outside its core U.S. market.

- We'll now explore how landing the German Navy contract enhances Lockheed Martin's international order momentum and reinforces its investment narrative.

We've found 18 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Lockheed Martin Investment Narrative Recap

To believe in Lockheed Martin as a shareholder, you need to see continued global demand for advanced defense systems driving revenue growth and reinforcing its leadership in aerospace and defense. The recent German Navy contract is meaningful for international momentum, but current short-term catalysts still hinge on F-35 program order flows and managing cost overruns on legacy contracts; this news does not materially change those immediate catalysts or risks.

Among recent announcements, Lockheed Martin's agreement with Avio to build a US-based solid rocket motor facility stands out, as it aims to bolster supply chain resilience for critical propulsion systems. This initiative complements international contract wins and supports the operational stability that underpins the case for improving margin control and delivery on high-value government programs.

However, despite these positive developments, investors should be aware that persistent cost overruns on major legacy contracts remain a risk, especially if...

Read the full narrative on Lockheed Martin (it's free!)

Lockheed Martin's narrative projects $81.0 billion in revenue and $7.1 billion in earnings by 2028. This requires 4.1% annual revenue growth and a $2.9 billion increase in earnings from the current $4.2 billion.

Uncover how Lockheed Martin's forecasts yield a $526.88 fair value, a 11% upside to its current price.

Exploring Other Perspectives

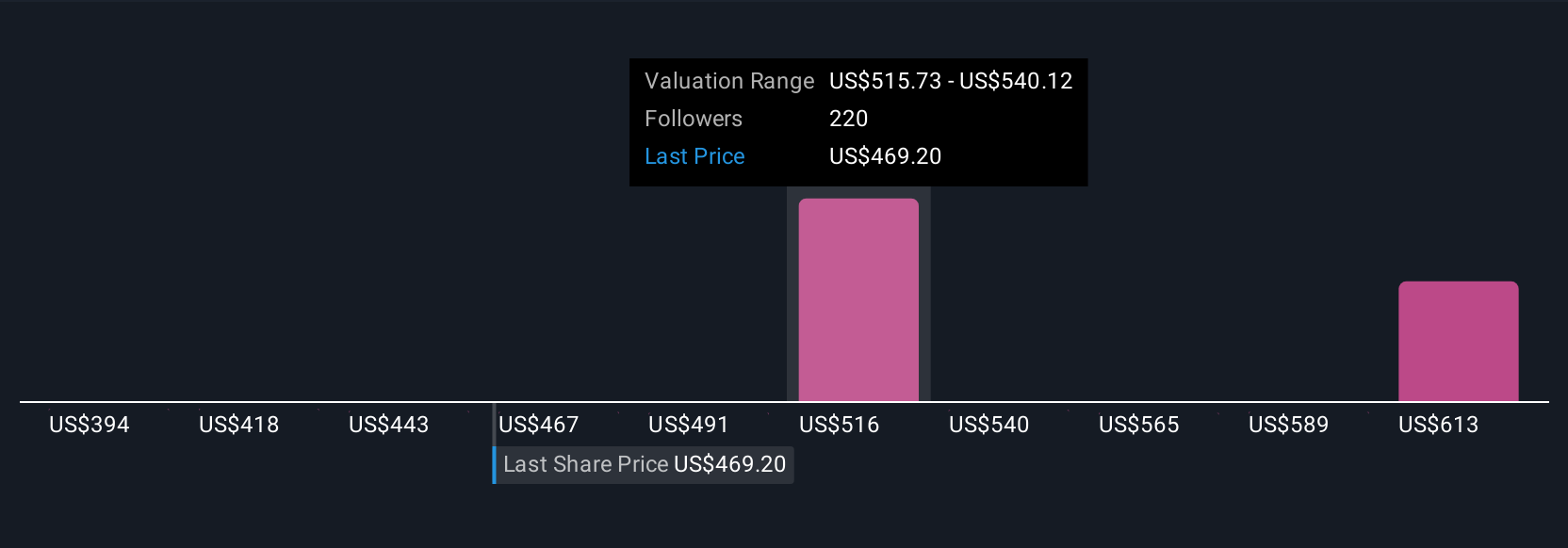

Twenty-five members of the Simply Wall St Community valued Lockheed Martin shares between US$389.28 and US$633.96, with estimates spanning nearly US$250. Amid this diversity of opinion, many remain focused on whether ongoing order wins can offset profit margin pressure from fixed-price contracts.

Explore 25 other fair value estimates on Lockheed Martin - why the stock might be worth as much as 34% more than the current price!

Build Your Own Lockheed Martin Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Lockheed Martin research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Lockheed Martin research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lockheed Martin's overall financial health at a glance.

Contemplating Other Strategies?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 27 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LMT

Lockheed Martin

An aerospace and defense company, engages in the research, design, development, manufacture, integration, and sustainment of technology systems, products, and services worldwide.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor