Karman Holdings (NYSE:KRMN) has recently attracted attention as its stock saw shifts over the past month, with a decline of about 20%. Investors are now keeping a close eye on what this could mean for the company’s valuation in the future.

While the past month delivered a sharp 19.7% drop in Karman Holdings’ share price, that follows a spectacular year-to-date share price return of over 100%. This underscores how quickly momentum can shift when growth expectations or risk perceptions change.

With such significant price swings and ongoing revenue growth, is this recent pullback a rare value opportunity in Karman Holdings, or are investors simply factoring in all the future gains already?

Advertisement

Price-to-Sales Ratio of 18.6x: Is it justified?

Karman Holdings is trading at a price-to-sales ratio of 18.6x, which points to a significant premium over both its peers and the wider industry. With a last close price of $60.25, this elevated multiple stands out in comparison to other companies in the US Aerospace & Defense sector.

The price-to-sales ratio reflects how much investors are willing to pay for every dollar of sales. For a fast-growing company like Karman Holdings, a higher ratio can sometimes be justified by strong revenue prospects. In this case, revenues grew 29.4% in the past year, and forecasts remain robust.

However, Karman's price-to-sales multiple is much higher than the US Aerospace & Defense industry average of 2.9x and also far above the estimated fair price-to-sales ratio of 5.3x. This indicates the current market valuation may be overly optimistic compared to sector norms, and the market could eventually adjust closer to that lower level.

Result: Price-to-Sales Ratio of 18.6x (OVERVALUED)

However, ongoing market volatility and lofty valuation multiples remain risks. These factors could prompt further downside if growth momentum slows or sentiment shifts rapidly.

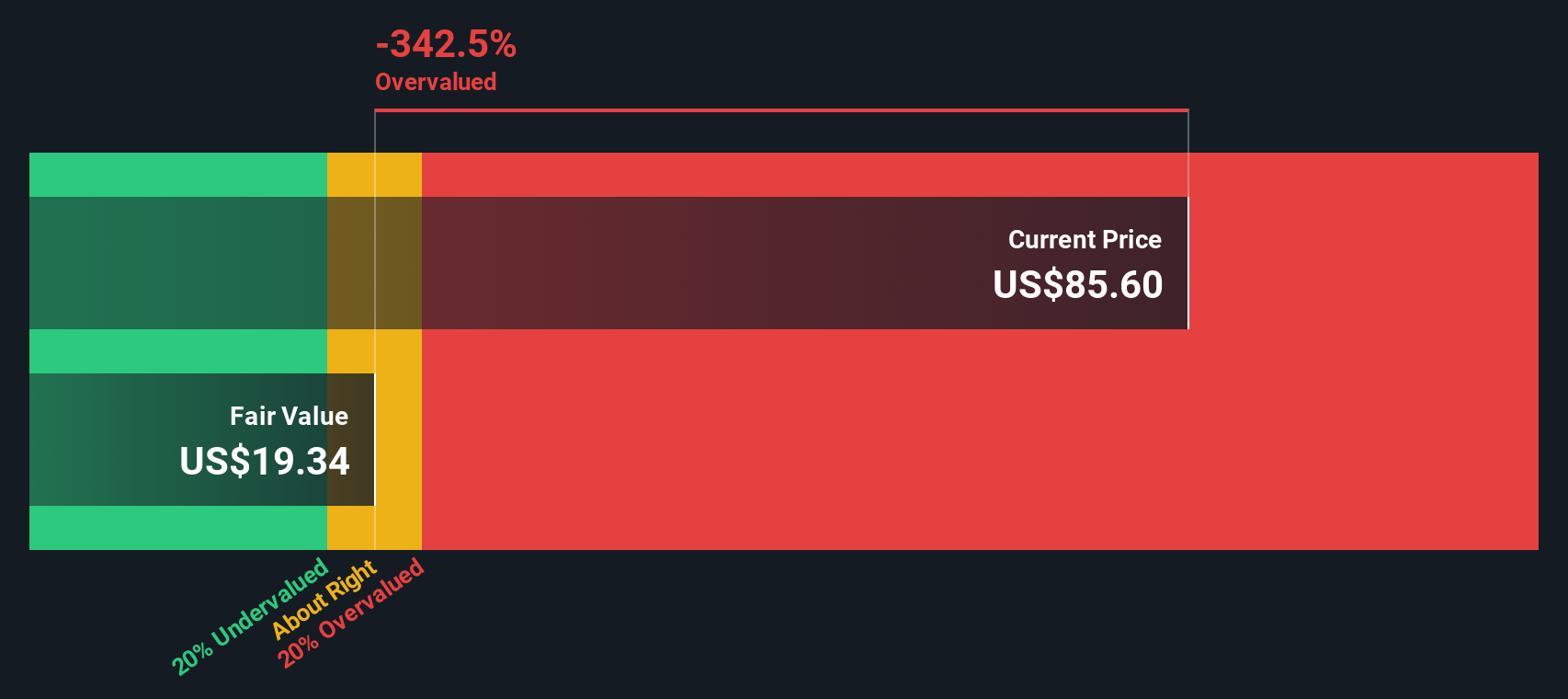

While multiples show Karman Holdings as expensive, the SWS DCF model paints an even starker picture. According to our DCF estimate, the fair value is $28.09, which is significantly below the current share price of $60.25. This suggests the market may be pricing in more growth than fundamentals support.

If you think there's another angle to this story, or you want to dive deeper into the data, you can quickly build your own narrative and see where the numbers take you. Do it your way

A great starting point for your Karman Holdings research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t limit yourself to just one stock story. Move quickly now to spot emerging trends and grab opportunities the market hasn’t fully noticed yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Karman Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.