- United States

- /

- Aerospace & Defense

- /

- NYSE:HWM

Howmet Aerospace (HWM): Valuation Check as Short Interest Climbs Above Peers

Reviewed by Simply Wall St

Short interest in Howmet Aerospace (HWM) has ticked higher, with 10.47 million shares now sold short, or about 3% of the float. This level tops its peer average and may hint at growing skepticism.

See our latest analysis for Howmet Aerospace.

Even with short interest creeping up, the recent 1 day share price gain of 3.56% sits against a powerful backdrop. A year to date share price return of 78.72% and a five year total shareholder return of 633.05% suggest momentum is still very much on Howmet Aerospace’s side.

If this kind of move has you thinking more broadly about the sector, it could be worth exploring other aerospace and defense stocks that might be setting up for their next leg higher.

With growth in both revenue and earnings, a multi year share price surge, and the stock still trading below the average analyst target, investors now face a key question: Is there more upside ahead, or is future growth already priced in?

Most Popular Narrative Narrative: 14.7% Undervalued

The most followed narrative sees Howmet Aerospace’s fair value well above the last close of $198, framing today’s rally within a longer runway for upside.

Strategic investments in automation and digital manufacturing, combined with cost rationalization and product mix optimization, are driving underlying productivity improvements and gross margin expansion, supporting robust long term earnings growth.

Want to see what kind of revenue engine and profit profile could justify this richer future multiple over today’s? The narrative’s model leans on steadily rising top line, expanding margins, and a bold earnings trajectory out to 2028. Curious how those moving parts compound into that higher fair value, and what discount rate they need to get there?

Result: Fair Value of $232.15 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, elevated capital spending and reliance on major OEMs mean that any demand slowdown or contract shifts could quickly pressure margins and challenge the upside case.

Find out about the key risks to this Howmet Aerospace narrative.

Another Lens on Valuation

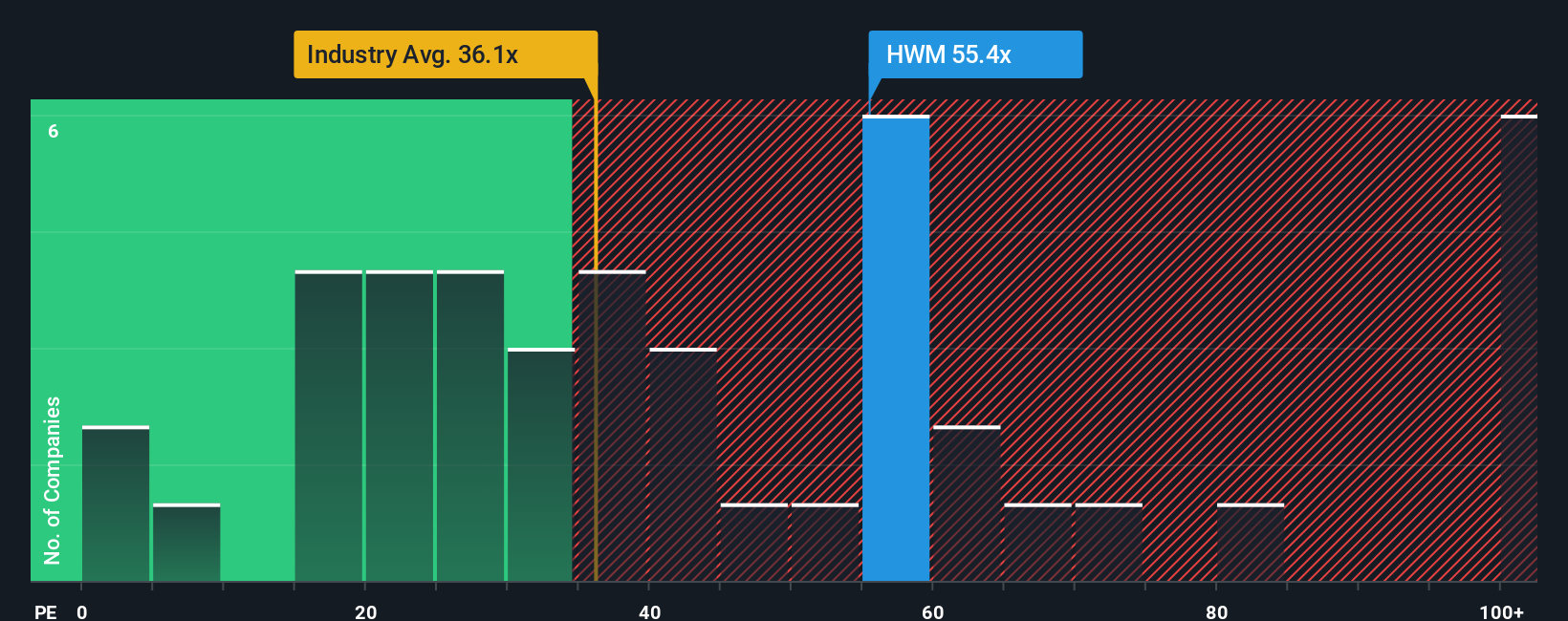

Our valuation checks using the price to earnings ratio paint a very different picture. At about 55 times earnings, Howmet trades far richer than both the US Aerospace and Defense industry at 36.5 times and its peer average at 27.4 times, and also above a fair ratio of 35.3 times. That kind of premium can work while growth stays flawless, but it leaves little room for execution slips or macro shocks.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Howmet Aerospace Narrative

If you want to dive into the numbers yourself and challenge these assumptions, you can build a customized view of Howmet in under three minutes: Do it your way.

A great starting point for your Howmet Aerospace research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Use the Simply Wall St Screener today to uncover fresh opportunities, sharpen your edge, and avoid leaving potential returns on the table while others move first.

- Capture early stage potential by scanning these 3628 penny stocks with strong financials that already back their stories with solid financials and real business traction.

- Ride structural growth trends by zeroing in on these 29 healthcare AI stocks transforming diagnostics, treatment, and efficiency across global health systems.

- Strengthen your income strategy by targeting these 13 dividend stocks with yields > 3% that may help support returns even when markets turn choppy.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Howmet Aerospace might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HWM

Howmet Aerospace

Provides advanced engineered solutions for the aerospace and transportation industries in the United States, Japan, France, Germany, the United Kingdom, Mexico, Italy, Canada, Poland, China, and internationally.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion