Advertisement

- United States

- /

- Trade Distributors

- /

- NYSE:GWW

Is Grainger Fairly Priced After Digital Expansion and Recent Share Price Movements in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if W.W. Grainger is undervalued, fairly priced, or possibly even a hidden gem? You are not alone. Many investors are questioning whether the stock deserves a spot in their portfolio right now.

- The stock has seen plenty of action lately, rising 2.4% over the past week but still down 3.4% for the last month and 9.3% so far this year. This reminds us that even long-term out-performers can face periods of volatility.

- Much of the recent price movement tracks with broader market shifts and sector rotation within industrials, as investors weigh resilience in supply chain trends against updates in global infrastructure and reshoring ambitions. News highlighting Grainger’s focus on digital transformation and expansion of its distribution capabilities has kept the company in the spotlight among both growth fans and risk-watchers.

- When you look at the traditional value score for W.W. Grainger, it registers just 1 out of 6 on our in-depth valuation checks. However, crunching the numbers is only half the story. As we walk through various approaches to valuation in the next sections, keep an eye out for a more insightful way to gauge the company’s real worth coming up at the end.

W.W. Grainger scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: W.W. Grainger Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s intrinsic value by projecting its future cash flows and then discounting them back to today’s values. This approach is widely used because it focuses strictly on the cash a business actually generates, rather than accounting profits or market mood swings.

For W.W. Grainger, the current Free Cash Flow stands at $1.49 billion. Analysts forecast that the company’s annual cash flows will continue to grow, reaching a projected $2.24 billion by 2029. Further projections suggest total free cash flow could exceed $2.9 billion a decade from now. While only the next five years have analyst estimates, Simply Wall St extrapolates beyond that period to offer a full ten-year outlook on the company’s ability to generate cash.

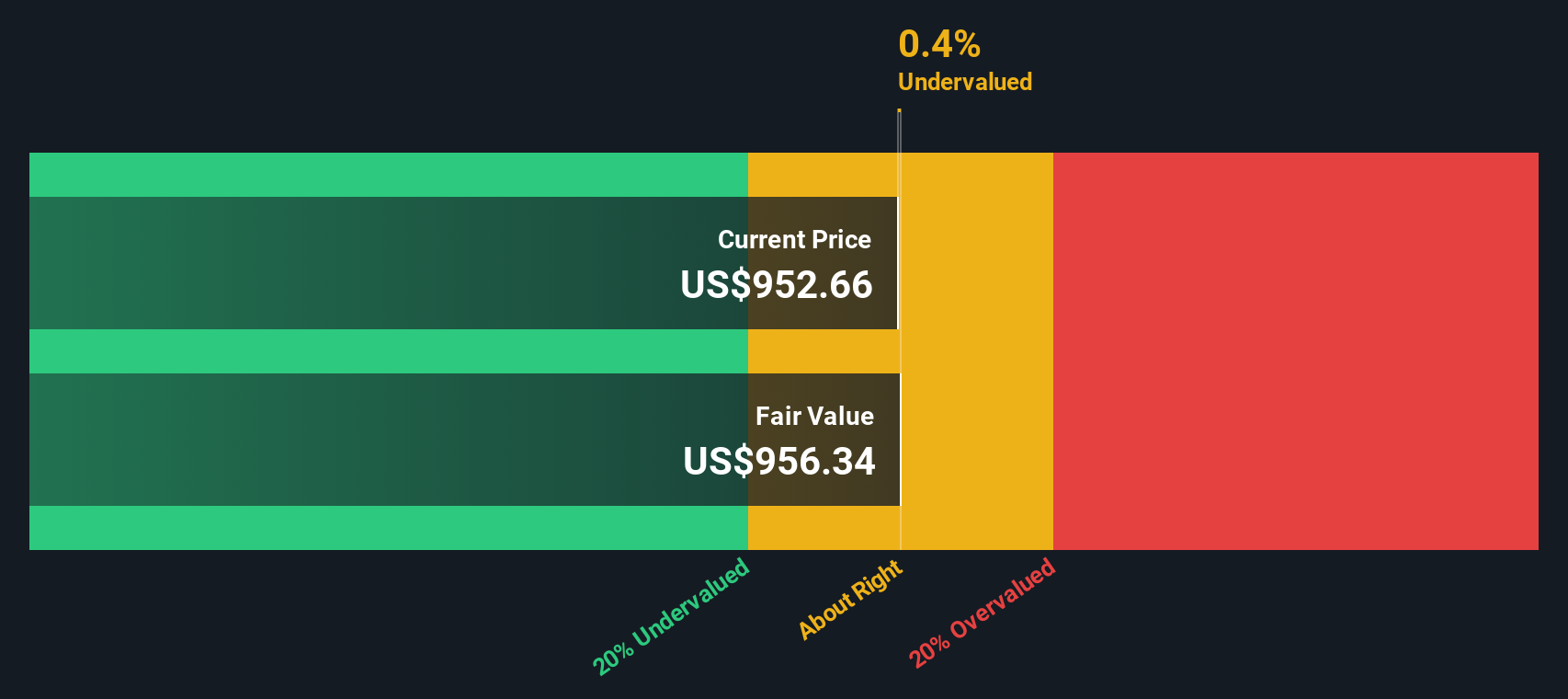

Using this 2 Stage Free Cash Flow to Equity DCF model, the estimated intrinsic value for W.W. Grainger comes out to $942 per share. When compared to the current share price, this value suggests the stock is about 0.3% above its fair value. This puts the stock essentially in line with where it should trade based on future cash potential.

Result: ABOUT RIGHT

W.W. Grainger is fairly valued according to our Discounted Cash Flow (DCF), but this can change at a moment's notice. Track the value in your watchlist or portfolio and be alerted on when to act.

Approach 2: W.W. Grainger Price vs Earnings

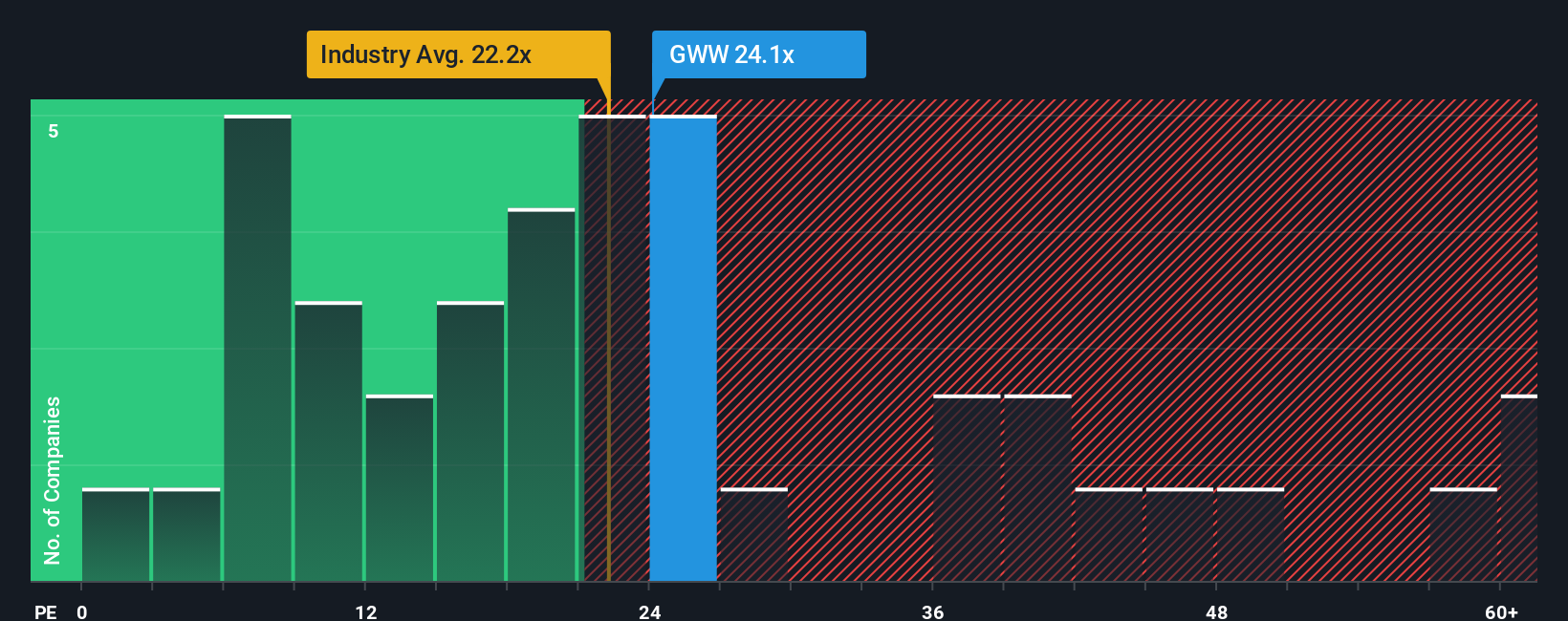

The price-to-earnings (PE) ratio is a widely used metric for valuing profitable companies like W.W. Grainger, because it links the company’s current share price to how much profit it generates. For established businesses with steady earnings, the PE ratio provides a straightforward snapshot of how the market values every dollar of profit today.

However, deciding what makes a “normal” PE ratio can be tricky. High growth prospects often justify a higher PE, as investors expect bigger profits in the future. Conversely, businesses facing risks or slower growth usually trade at lower PEs to reflect those uncertainties.

Right now, W.W. Grainger is trading at a PE ratio of 26x. Compare this to the Trade Distributors industry average of 19x and a peer average of 23x, and Grainger appears to command a premium. But surface-level comparisons can be misleading. This is where Simply Wall St’s proprietary "Fair Ratio" is used. For Grainger, the Fair Ratio is 27x. This metric adjusts for unique factors like earnings growth, industry dynamics, profitability, market cap, and risk profile, providing a more tailored benchmark than general industry or peer averages.

Because the Fair Ratio is just slightly above the actual PE, this suggests Grainger is trading very close to its calculated fair value based on fundamentals. In other words, the stock is neither notably undervalued nor expensive relative to what you would expect, given its quality and prospects.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1432 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your W.W. Grainger Narrative

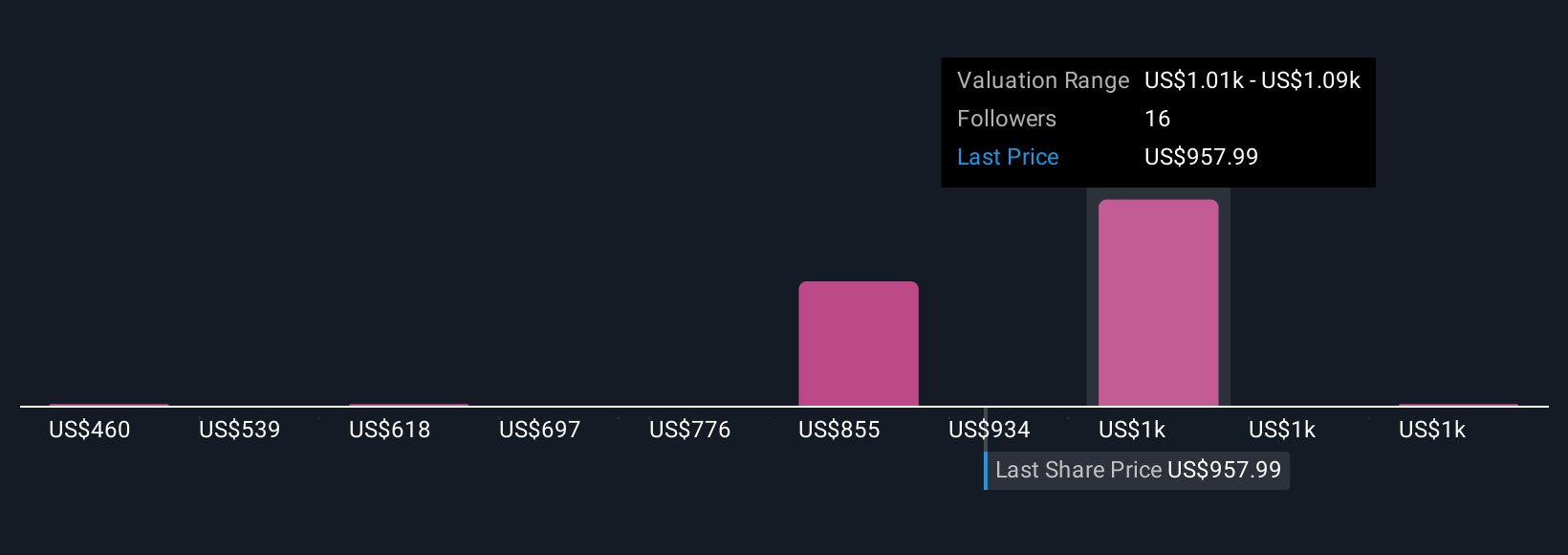

Earlier we mentioned that there is an even better way to understand valuation, so now let’s introduce you to Narratives. A Narrative is simply your perspective on what’s driving a company’s future. It connects your story about W.W. Grainger with your assumptions for revenue, earnings, and fair value, giving your investment decisions both numbers and meaning. Narratives tie together what you see unfolding for the business, your outlook for key metrics, and a resulting fair value, transforming investing from a guessing game into a rational process.

On Simply Wall St, Narratives are an easy, accessible tool available in the Community page, used by millions of investors worldwide. You can set your own view, compare it with others, and clearly see when your fair value suggests it might be time to buy or sell by tracking how your Narrative’s value stacks up against the current market price. Best of all, Narratives update dynamically with new data like earnings, news, or analyst forecasts, making sure your outlook always reflects the latest facts.

For example, some investors believe W.W. Grainger’s digital growth and operational execution justify a high fair value of $1,213 per share, while those more cautious about margin and growth risks see fair value closer to $930. This shows how the same stock can inspire different, actionable stories.

Do you think there's more to the story for W.W. Grainger? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if W.W. Grainger might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:GWW

W.W. Grainger

Distributes maintenance, repair, and operating products and services primarily in North America, Japan, and the United Kingdom.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative