Advertisement

- United States

- /

- Construction

- /

- NYSE:FIX

Will Data Center-Driven HVAC Demand Transform Comfort Systems USA’s (FIX) Growth Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

- Recently, Comfort Systems USA was highlighted for its strong growth prospects, including an expected very large increase in EPS and increased demand for its specialized HVAC solutions from the booming data center sector driven by AI and cloud computing trends.

- An interesting insight is that advanced cooling requirements for new data center developments are positioning the company to benefit from high-margin opportunities and potential merger and acquisition interest.

- We'll explore how data center-driven demand growth supports Comfort Systems USA's overall investment narrative and shapes its future prospects.

Find companies with promising cash flow potential yet trading below their fair value.

Comfort Systems USA Investment Narrative Recap

To be a shareholder in Comfort Systems USA right now, you need to believe that technology-driven markets like data centers will continue fueling above-average earnings growth and project demand, while management keeps capitalizing on operational strengths and margin opportunities. The recent news reinforcing surging EPS projections and strong demand for specialized cooling solutions meaningfully supports the key near-term catalyst: sustained backlog expansion and profitability from tech-related projects. However, it does not materially reduce the biggest current risk, Comfort Systems’ heavy reliance on this sector, which increases vulnerability if tech buildouts slow down materially.

Of the recent company announcements, the October 2025 Q3 earnings release stands out as most relevant, showing significant year-over-year gains in both sales and net income, and highlighting growth in its data center-focused business. This financial performance gives clear context to the latest optimism around AI and cloud-driven demand, connecting the strong project pipeline to current revenue delivery and earnings momentum.

In contrast, investors should be alert to what happens if demand from technology clients unexpectedly cools, since …

Read the full narrative on Comfort Systems USA (it's free!)

Comfort Systems USA's outlook projects $10.5 billion in revenue and $1.3 billion in earnings by 2028. This is based on an annual revenue growth rate of 10.9% and a $607.8 million increase in earnings from the current $692.2 million.

Uncover how Comfort Systems USA's forecasts yield a $1133 fair value, a 23% upside to its current price.

Exploring Other Perspectives

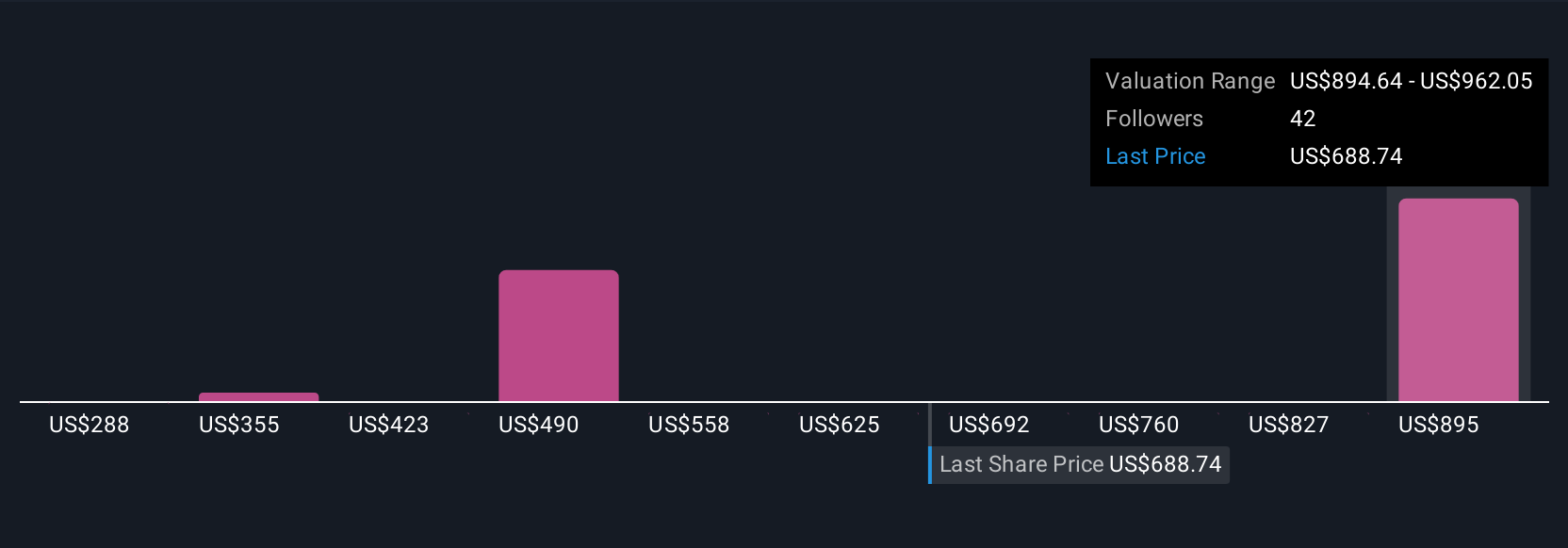

Simply Wall St Community members’ fair value estimates for Comfort Systems USA span from US$287.88 to US$1,487.18, with 11 different views included in this range. While most contributors see meaningful upside, keep in mind ongoing concentration risks as data center demand drives the narrative, market opinion around future growth potential clearly varies.

Explore 11 other fair value estimates on Comfort Systems USA - why the stock might be worth as much as 61% more than the current price!

Build Your Own Comfort Systems USA Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Comfort Systems USA research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Comfort Systems USA research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Comfort Systems USA's overall financial health at a glance.

Seeking Other Investments?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Outshine the giants: these 27 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FIX

Comfort Systems USA

Provides mechanical and electrical installation, renovation, maintenance, repair, and replacement services for the mechanical and electrical services industry in the United States.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.1% undervalued

TI

Community Contributor