Advertisement

- United States

- /

- Electrical

- /

- NYSE:ETN

Eaton (ETN): Exploring Valuation After Recent Pullback and Long-Term Shareholder Gains

Simply Wall St

Reviewed by Simply Wall St

Eaton (ETN) shares have seen some movement lately, with investors watching for fresh catalysts on the horizon. The company’s recent performance invites a closer look at how its fundamentals compare in the current environment.

See our latest analysis for Eaton.

Eaton’s share price has pulled back about 10% over the past month but is still up slightly for the year, which suggests some profit-taking after a lengthy rally. The contrast with a strong 3-year total shareholder return of 118% shows that long-term momentum has stayed firmly intact, even if recent sentiment has cooled a bit.

If you’re curious to see what else investors are watching beyond Eaton, consider widening your search and discover fast growing stocks with high insider ownership

With Eaton’s steady long-term gains and recent pullback, the key question for investors is whether this dip represents an undervalued entry point or if the market has already factored in all the company’s future growth prospects.

Most Popular Narrative: 16.8% Undervalued

With Eaton's last close at $341.69 and the most popular narrative assigning a fair value of $410.70, the narrative outlook sees meaningful upside from current levels. The rationale for this valuation is built around order momentum, aggressive expansion, and improvements in market mix.

Strategic wins and technology leadership in the rapidly expanding data center end market are deepening Eaton's penetration and raising content per megawatt, with major partnerships (for example, NVIDIA and Siemens Energy) and acquisitions (Fibrebond and Resilient Power) positioning Eaton as the go-to provider for next-generation high-density and AI-centric infrastructure. This supports outsized revenue growth and structurally higher margins due to richer, more sophisticated product mix.

Want to know the growth blueprint behind this high valuation? The key element of this narrative is a surge in margin expansion alongside bold projections for future profits and rapid sales increases. Intrigued which financial levers drive this number? Find out what targets analysts are betting on and what makes this pricing potentially justified.

Result: Fair Value of $410.70 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, continued weakness in Eaton's Vehicle segment or unexpected volatility in data center demand could challenge the positive outlook reflected in current valuations.

Find out about the key risks to this Eaton narrative.

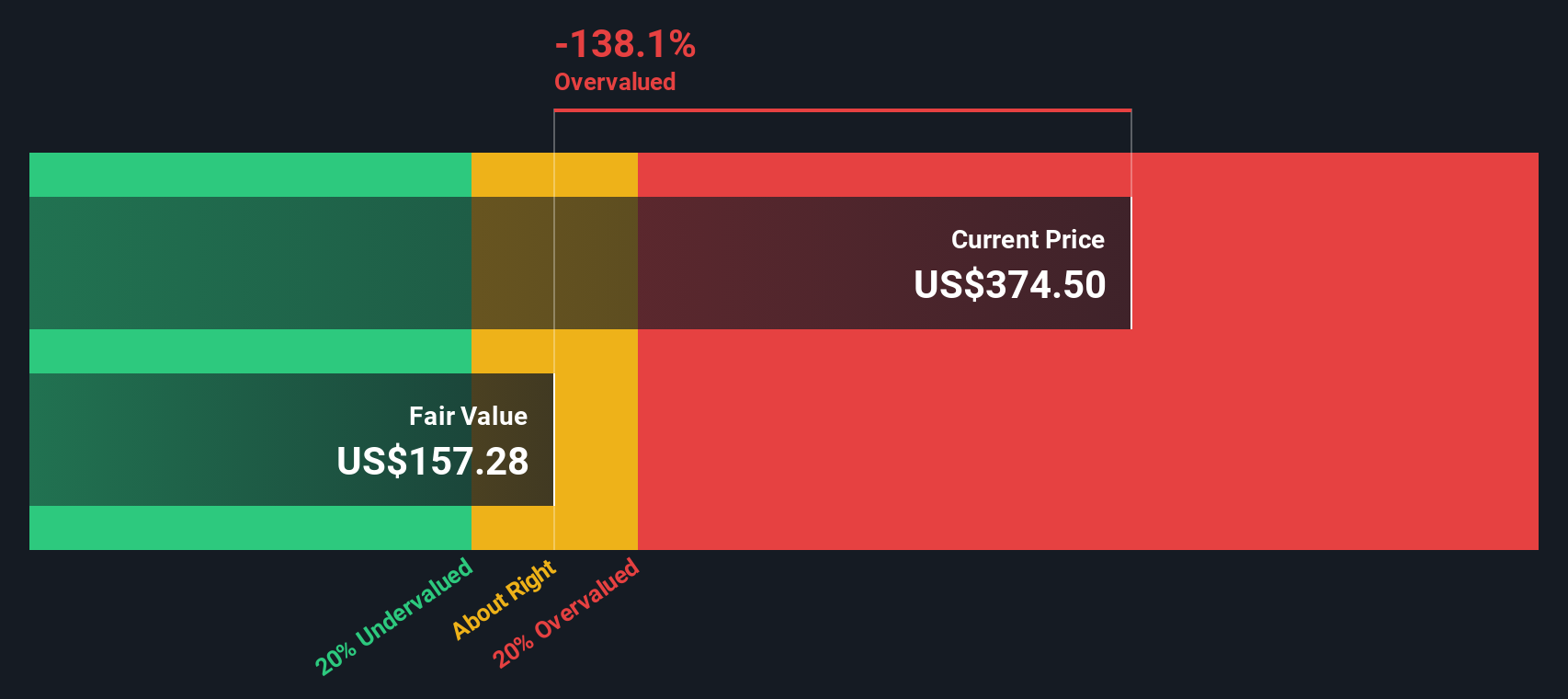

Another View: SWS DCF Model Signals Overvaluation

Taking a different approach, our SWS DCF model suggests that Eaton, at $341.69, is well above its estimated fair value of $154.15. This implies the current market price reflects a high degree of optimism, perhaps more than fundamentals warrant. Could this mean risk is skewed to the downside if growth falters?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Eaton for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 933 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Eaton Narrative

If you see things differently or want to dig into the details yourself, it’s easy to build your own view using our tools in just a few minutes. Do it your way

A great starting point for your Eaton research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Smart investing means staying ahead of the curve. Don’t let exceptional opportunities pass you by. Use the right tools to spot tomorrow’s winners today.

- Snag high yields and create a stream of passive income by checking out these 15 dividend stocks with yields > 3% with robust payouts above 3%.

- Target stocks harnessing artificial intelligence breakthroughs for the next wave of growth by starting with these 25 AI penny stocks.

- Capture value before the crowd moves in and uncover shares trading below intrinsic worth on these 933 undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Eaton might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ETN

Eaton

Operates as a power management company in the United States, Canada, Latin America, Europe, and the Asia Pacific.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

92 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative