Advertisement

- United States

- /

- Electrical

- /

- NYSE:ETN

Are Eaton Shares Now Attractive After Recent 7.7% Drop in 2025?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if Eaton is actually a bargain or if all that buzz is just noise? Let's unpack what the numbers are really telling us about value.

- After years of strong gains, Eaton's share price has dipped recently, down 5.7% over the last week and 7.7% over the past month, even though it's still up 6.2% year-to-date.

- Much of this movement has been sparked by broad market volatility and fresh attention on infrastructure investment, with analysts spotlighting Eaton's role in the electrification push. Investors are trying to figure out if these shifts signal a temporary hiccup or set the stage for future growth.

- When it comes to value, Eaton currently scores a 2 out of 6 on our valuation checks, meaning it's undervalued in only a couple of areas. We'll break down those traditional ways of valuing Eaton in a moment, but stick around because there is an even smarter way to look at the big picture coming up at the end of the article.

Eaton scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Eaton Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's true value by forecasting its future cash flows and discounting them back to today's dollars. In other words, it asks how much all the cash Eaton is expected to generate in the years ahead is worth in present terms.

Currently, Eaton has generated $3.27 Billion in free cash flow over the last twelve months. Analysts expect Eaton's free cash flow to continue growing, with projections reaching $5.49 Billion by 2029. Beyond the analyst estimates, additional out-year projections extrapolated by Simply Wall St anticipate free cash flows staying above $4.5 Billion annually for the following years.

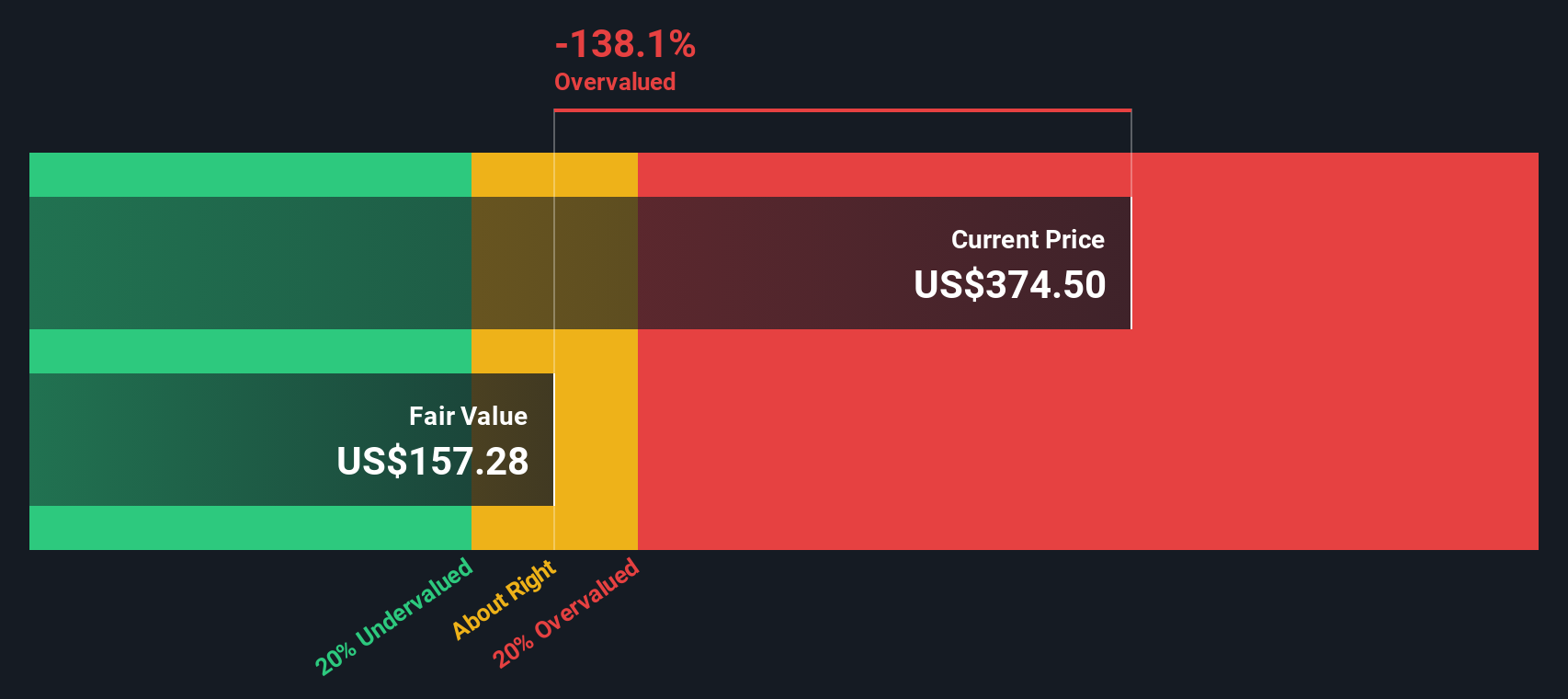

Based on these projections and using a two-stage free cash flow to equity model, the DCF analysis estimates Eaton's fair value at $150.17 per share. This suggests the stock is trading 134.7% above its intrinsic value right now, meaning it is significantly overvalued based on its expected future cash generation.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Eaton may be overvalued by 134.7%. Discover 879 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Eaton Price vs Earnings (PE)

For companies like Eaton that are consistently profitable, the price-to-earnings (PE) ratio is a popular and effective way to gauge whether a stock is trading at a sensible value. The PE ratio reflects how much investors are willing to pay for each dollar of a company’s earnings. What counts as a “normal” or “fair” PE depends on growth prospects and perceived risk. Companies with higher expected growth and lower risk typically command higher PE multiples, while slower-growth or riskier businesses trade at lower ones.

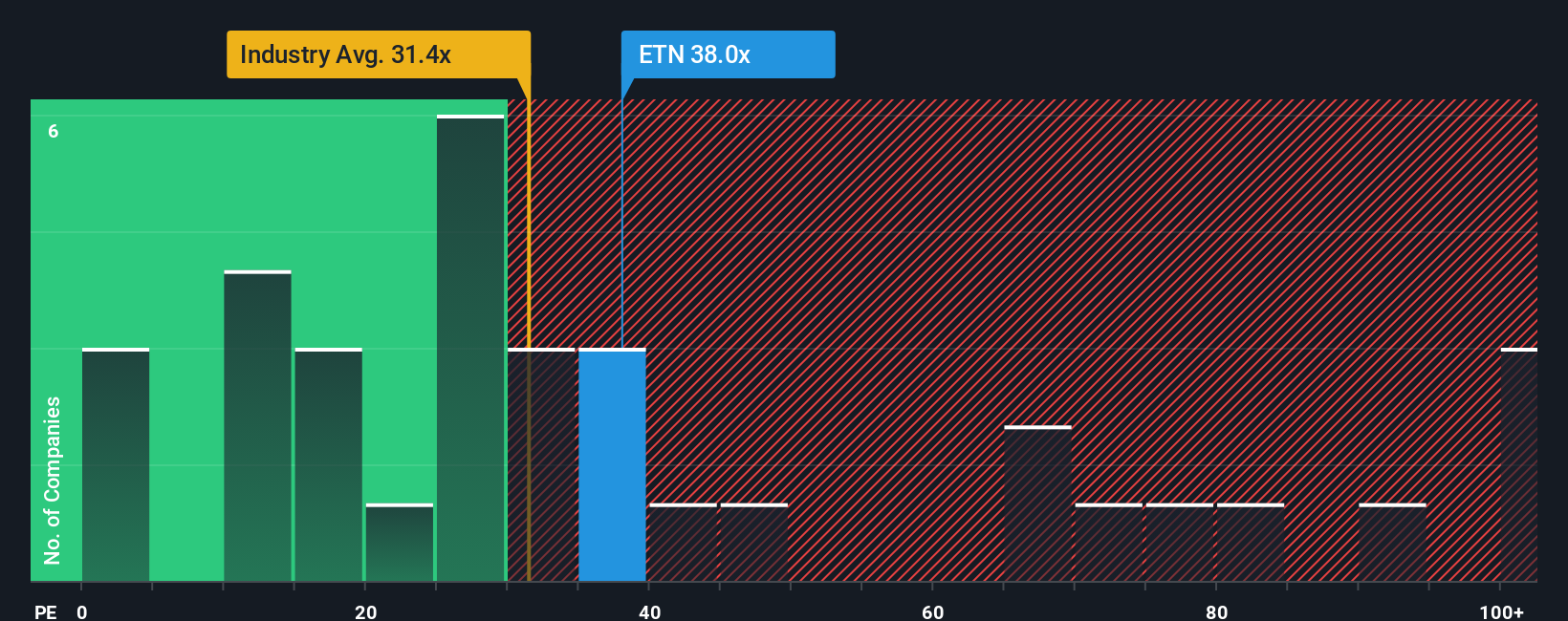

Currently, Eaton trades at a PE ratio of 34.9x. That is higher than the Electrical industry average of 28.7x, but still below its peer group average of 43.4x. On the surface, this might look somewhat pricey compared to the broader industry, but less so relative to its direct competitors.

However, Simply Wall St’s “Fair Ratio” takes this analysis a step further. Rather than just comparing to industry or peers, the Fair Ratio (for Eaton, 38.4x) pins down an appropriate PE by factoring in Eaton’s earnings growth outlook, margins, market cap, and unique risk profile. This gives a more tailored benchmark and helps filter out misleading comparisons. In this case, Eaton’s actual PE is just below its Fair Ratio, suggesting the stock is roughly in line with its fundamentals given its growth, profitability and risk characteristics.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1405 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Eaton Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is much more than just a number; it’s your own story about Eaton’s future, based on what you believe about its growth, profitability, and risks, which then gets linked to a detailed financial forecast and an estimated fair value.

This approach goes beyond traditional metrics by letting you connect real business developments and your perspective to concrete financial outcomes. Narratives are easy to create and explore right on Simply Wall St’s Community page, where millions of investors share ideas and debate different outlooks.

By comparing your Narrative’s fair value to today’s share price, you can decide if Eaton is a buy, hold, or sell based on your personal view. And because Narratives update automatically when new news, earnings, or market shifts come in, you always see the latest picture.

For example, one investor might be optimistic, predicting upside to $440 per share if data center demand and electrification really take off. A more cautious investor sees downside to $288 if margins disappoint or cyclical end-markets weaken. This proves there is no single “correct” value, just stories shaped by what you think will happen next.

Do you think there's more to the story for Eaton? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Eaton might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ETN

Eaton

Operates as a power management company in the United States, Canada, Latin America, Europe, and the Asia Pacific.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor