Bloom Energy (BE) shares have moved steadily in recent days, drawing attention from investors interested in its clean energy technology and consistent revenue growth. With the company’s strong results over the past year, the current valuation sparks ongoing debate.

Despite a volatile week, Bloom Energy's 90-day share price return of 84.56% and a remarkable year-to-date rise of 332.78% have fueled fresh momentum and caught the market’s attention. While short-term swings have challenged some nerves, long-term investors are enjoying standout total shareholder returns of 271.7% over twelve months and an impressive 375% over three years. These are signs that confidence in the company’s growth potential remains robust as debates swirl around its current valuation.

If Bloom’s accelerating momentum has you scanning for other tech-fueled growth stories, it could be the ideal time to see the full list of innovative opportunities with our See the full list for free.

With shares surging and strong results in tow, the big question now is whether Bloom Energy's current price factors in all its future promise or if there may still be a smart entry point for investors.

Advertisement

Most Popular Narrative: 9.6% Undervalued

Bloom Energy's current share price stands below its widely followed narrative fair value, highlighting a potential mispricing. This gap has led many investors to question whether the market truly appreciates the company's future revenue and profit potential.

Widespread grid constraints and long interconnection timelines for traditional utility-scale power provide a time-to-power advantage for Bloom's solutions. This boosts its competitive edge in mission-critical markets and is expected to expand the company's addressable market, positively impacting future top-line growth.

How does this narrative justify such an ambitious target? The key lies in forward-looking financial assumptions and a future profit multiple that turns industry heads. If you want to know the bold growth thesis, click through and uncover the drivers behind this surprising fair value estimate.

However, breakthroughs in zero-emission battery storage and regulatory shifts away from natural gas could quickly reduce Bloom Energy's competitive edge and growth prospects.

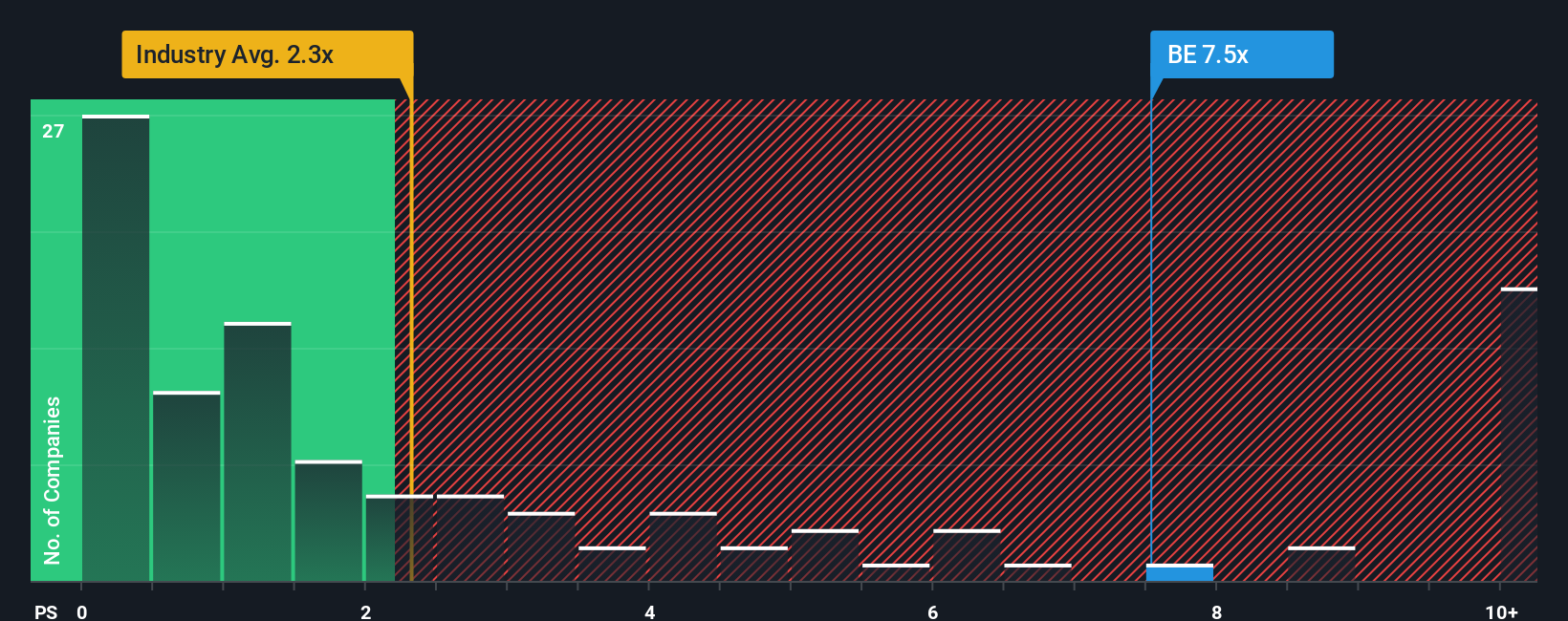

While Bloom Energy appears undervalued by narrative-driven fair value, a closer look at its sales ratio presents a different perspective. The company's price-to-sales ratio is 13.2 times, significantly higher than the US Electrical industry average of 1.9 times and the peer average of 2.8 times. Even when compared to the fair ratio of 9 times, Bloom appears expensive. This premium poses valuation risks if market sentiment shifts, but could it be justified by future performance?

If you want to challenge these views or dive even deeper, you can quickly shape your own narrative and make sense of the data in just a few minutes: Do it your way

Ready for Even More Smart Investment Opportunities?

Do not let your portfolio miss out on tomorrow’s winners. Seize your edge now by harnessing proven ideas tailored to unique trends and market strengths.

Unlock income potential with these 15 dividend stocks with yields > 3% as they consistently deliver attractive yields above 3% and can help power your long-term gains.

Ride the AI boom by tracking these 25 AI penny stocks which are setting the pace in artificial intelligence and revolutionizing entire industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bloom Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.