Advertisement

- United States

- /

- Aerospace & Defense

- /

- NYSE:BA

Boeing (BA) Is Down 7.5% After Record 777X Charge and Operational Losses – Has The Bull Case Changed?

Simply Wall St

Reviewed by Sasha Jovanovic

- Boeing recently reported third-quarter 2025 earnings, revealing revenue of US$23.27 billion and a net loss of US$5.34 billion, mainly due to a larger-than-expected charge on the 777X program and continued operational challenges.

- This quarterly result marked the largest loss for Boeing's Commercial Airplanes segment since December 2021, highlighting ongoing hurdles in program execution and manufacturing stability.

- We'll examine how these unexpected financial setbacks and the significant 777X charge may alter Boeing's investment narrative and future outlook.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Boeing Investment Narrative Recap

To be a Boeing shareholder today, you need conviction in the company's ability to bring its commercial airplane segment back to sustained profitability, driven by its large aircraft backlog and eventual stabilization of key programs. The third-quarter results, particularly the 777X-related charges, put added focus on Boeing's execution risk, but they have not materially changed the critical near-term catalyst: the ramp-up of 737 MAX and 787 production. The biggest risk remains the pace of margin recovery amid persistent program delays and operational hurdles.

Among recent announcements, the FAA's approval for Boeing to increase 737 MAX production from 38 to 42 planes per month is highly relevant. This move directly supports the main catalyst for Boeing, higher output of its most in-demand commercial jet, while putting renewed attention on whether Boeing can overcome manufacturing and supply chain challenges to deliver consistent results.

In contrast, what investors may underestimate is the degree to which persistent negative margins at Boeing’s commercial airplane division could ...

Read the full narrative on Boeing (it's free!)

Boeing's outlook anticipates $114.4 billion in revenue and $7.1 billion in earnings by 2028. This projection assumes 14.9% annual revenue growth and a $18.0 billion increase in earnings from the current -$10.9 billion.

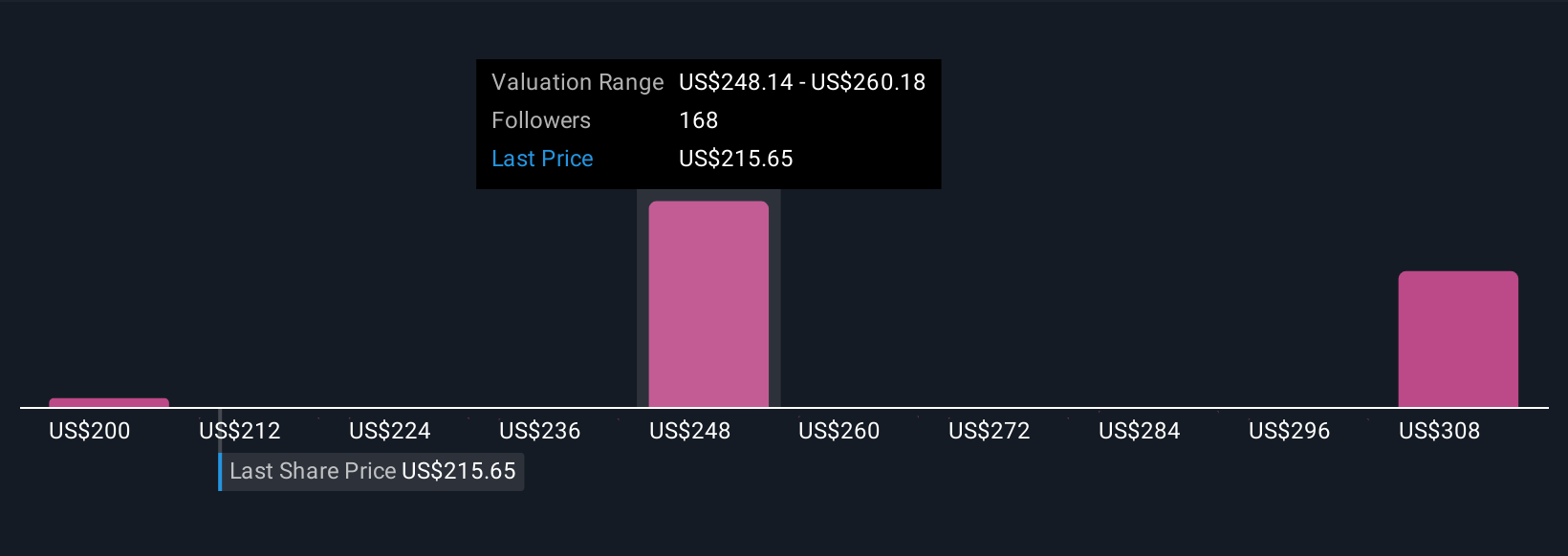

Uncover how Boeing's forecasts yield a $252.57 fair value, a 28% upside to its current price.

Exploring Other Perspectives

Twenty one forecasts from the Simply Wall St Community suggest Boeing’s fair value could be anywhere from US$206.79 to US$374.59 per share. With commercial airplane margins still negative, your own outlook on operational recovery may lead you to a different conclusion.

Explore 21 other fair value estimates on Boeing - why the stock might be worth as much as 90% more than the current price!

Build Your Own Boeing Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Boeing research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Boeing research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Boeing's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- The latest GPUs need a type of rare earth metal called Terbium and there are only 37 companies in the world exploring or producing it. Find the list for free.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Boeing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BA

Boeing

Designs, develops, manufactures, sells, services, and supports commercial jetliners, military aircraft, satellites, missile defense, human space flight and launch systems, and services worldwide.

Very undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor