- United States

- /

- Electrical

- /

- NYSE:AME

Ametek (AME) Valuation Check After SkyBitz Unveils New SmartTank ST705 Industrial Sensor

Reviewed by Simply Wall St

AMETEK (AME) just gave investors another reason to watch its industrial tech pipeline, with SkyBitz launching the SmartTank ST705 Radar Monitor, a C1D1 certified, non contact sensor aimed at tightening real time fluid monitoring.

See our latest analysis for AMETEK.

That steady rollout of smarter sensors lines up with AMETEK’s strong momentum, with a roughly 13 percent year to date share price return and a five year total shareholder return above 75 percent, suggesting investors are still rewarding its consistent growth story.

If this kind of industrial innovation has your attention, it could be worth seeing what else is out there through fast growing stocks with high insider ownership.

But with AMETEK trading near record highs, showing only modest upside to analyst targets, and carrying rich quality premiums, is the stock still undervalued on its long runway of sensor driven growth, or is the market already pricing in the next leg?

Most Popular Narrative Narrative: 8.3% Undervalued

With AMETEK last closing at $201.96 against a narrative fair value of about $220, the market is being asked to believe in a long runway of profitable growth powered by both organic demand and acquisitions.

Ongoing successful execution of a disciplined M&A strategy, leveraging a robust acquisition pipeline and significant balance sheet capacity, provides a catalyst for compounding top line and EPS growth, while integration synergies and operational excellence drive expansion of operating and EBITDA margins.

Curious what kind of growth and margin path needs to materialize to back that higher valuation, and how much richer the earnings multiple must get to make it all add up? The narrative lays out a detailed roadmap of rising profitability, expanding revenues, and a future PE profile that hinges on execution across several shifting end markets. Want to see exactly which levers have to fire together for that fair value to hold?

Result: Fair Value of $220.24 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent semiconductor and research end market weakness, or missteps in acquisition integration, could quickly challenge the market’s confidence in AMETEK’s premium valuation.

Find out about the key risks to this AMETEK narrative.

Another Lens on Valuation

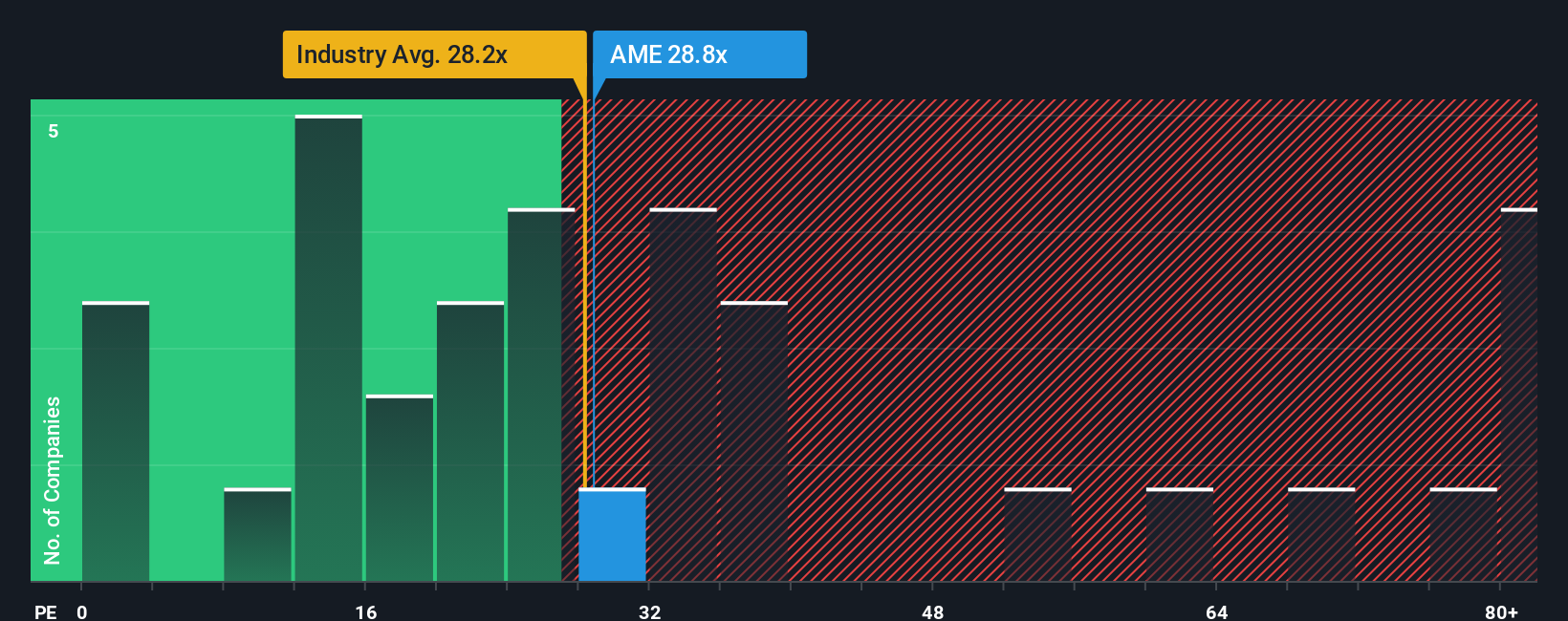

While the narrative suggests AMETEK is about 8 percent undervalued, a simple price to earnings check tells a different story. The shares trade at roughly 31.7 times earnings versus a fair ratio closer to 26 times, and even slightly above the US Electrical industry at 31.2 times. That points to a premium that could compress if growth underwhelms, or expand further if execution keeps beating the cautious assumptions baked into forecasts. Which side of that trade do you believe?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own AMETEK Narrative

If this perspective does not quite match your own view, or you would rather dig into the numbers yourself, you can build a custom take in just a few minutes: Do it your way.

A great starting point for your AMETEK research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, give yourself an edge by scanning targeted stock ideas from our screeners so you are not leaving potential winners on the table.

- Capture mispriced opportunities by reviewing these 918 undervalued stocks based on cash flows that pair solid fundamentals with attractive valuations.

- Ride structural growth trends by focusing on these 29 healthcare AI stocks transforming diagnostics, treatments, and medical workflows.

- Capitalize on income potential by targeting these 13 dividend stocks with yields > 3% that can strengthen your portfolio’s cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AME

AMETEK

Manufactures and sells electronic instruments (EIG) and electromechanical (EMG) devices in the United States and internationally.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion