Advertisement

- United States

- /

- Aerospace & Defense

- /

- NasdaqGS:VSEC

Evaluating VSE Shares After Major Aviation Contract and 94% Price Surge in 2025

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if VSE’s impressive run means the stock is now overvalued, or if there is still room for smart investors to get in at a fair price?

- VSE’s share price has soared, jumping 6.6% over the past week and 94.4% year-to-date, which has certainly caught the market’s attention.

- Recent news has highlighted VSE’s major contract wins in the aviation services sector and a strategic acquisition in its distribution unit, both of which have sparked renewed optimism. These moves have shifted investor sentiment and have painted a broader growth story for the company.

- Despite this excitement, VSE currently scores just 1 out of 6 on our undervaluation checks, a key fact that may surprise value-focused investors. We will explore what goes into this score and compare it to other valuation tools, and offer a different approach to understanding value that could make all the difference.

VSE scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: VSE Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a common valuation approach that estimates a company's intrinsic value by projecting its future cash flows and discounting them back to today’s value using a required rate of return. This is meant to reflect the present worth of the business given its future earning potential.

For VSE, the most recent reported Free Cash Flow (FCF) stands at $18.4 million. Analysts forecast robust growth with projected FCF reaching $103.1 million by 2028. For years beyond 2028, further increases are extrapolated by Simply Wall St, leading to estimates above $140 million by 2035. These projections use a two-stage Free Cash Flow to Equity model, a method that accounts for varying growth rates over different time periods.

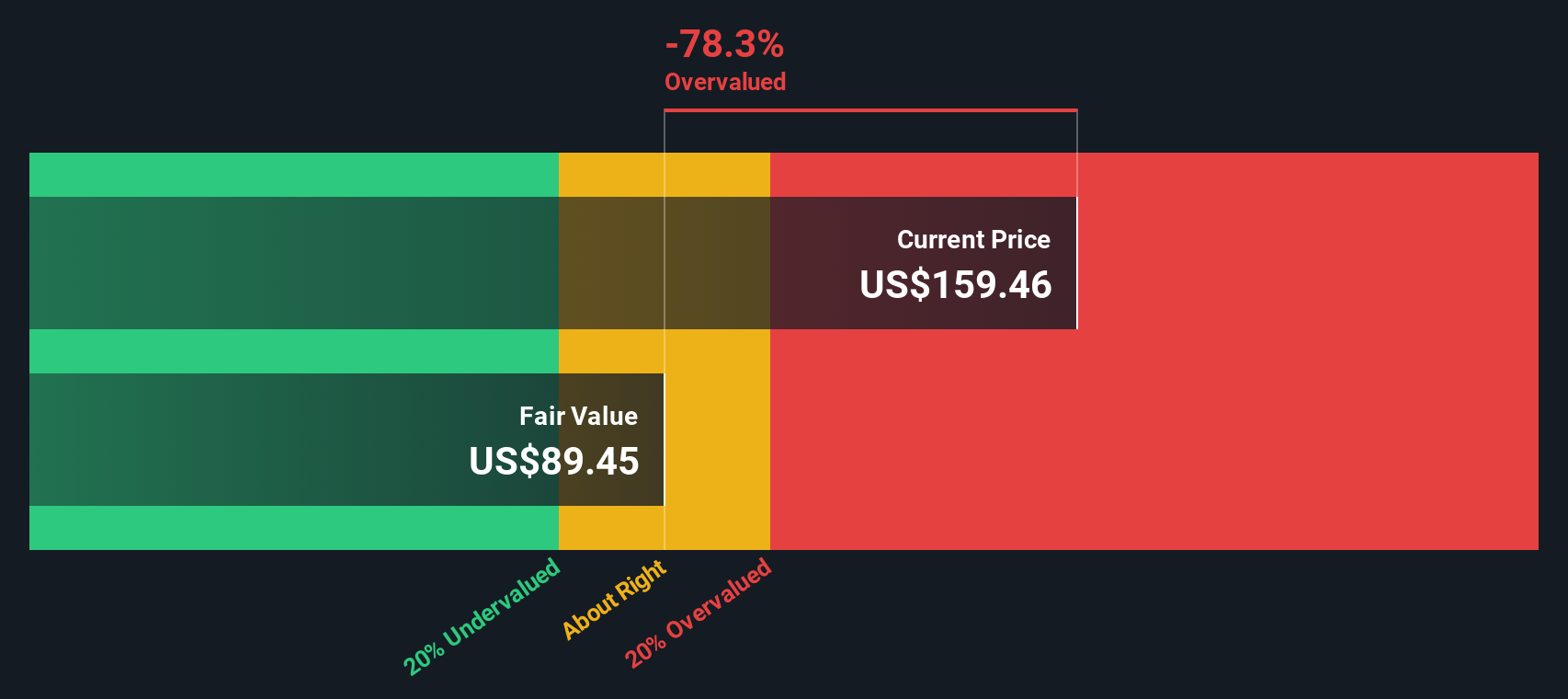

Based on the current DCF analysis, the estimated fair value of VSE’s shares is $99.51. This implies that the shares are trading at an 81.5% premium over their DCF-based intrinsic value, which suggests the stock is significantly overvalued by this measure.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests VSE may be overvalued by 81.5%. Discover 927 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: VSE Price vs Earnings (P/E)

The Price-to-Earnings (P/E) ratio is a popular metric for valuing profitable companies because it shows how much investors are willing to pay today for a dollar of current earnings. For established businesses generating steady profits, the P/E ratio is an effective way to set expectations about future growth, quality, and overall market sentiment.

Growth prospects and risk play major roles in what is considered a “fair” P/E ratio for any stock. Companies expected to grow quickly usually command higher P/E ratios, since investors believe future earnings will be significantly greater. Conversely, those with uncertain futures or higher risks tend to trade at lower P/E ratios as a cushion for potential downside.

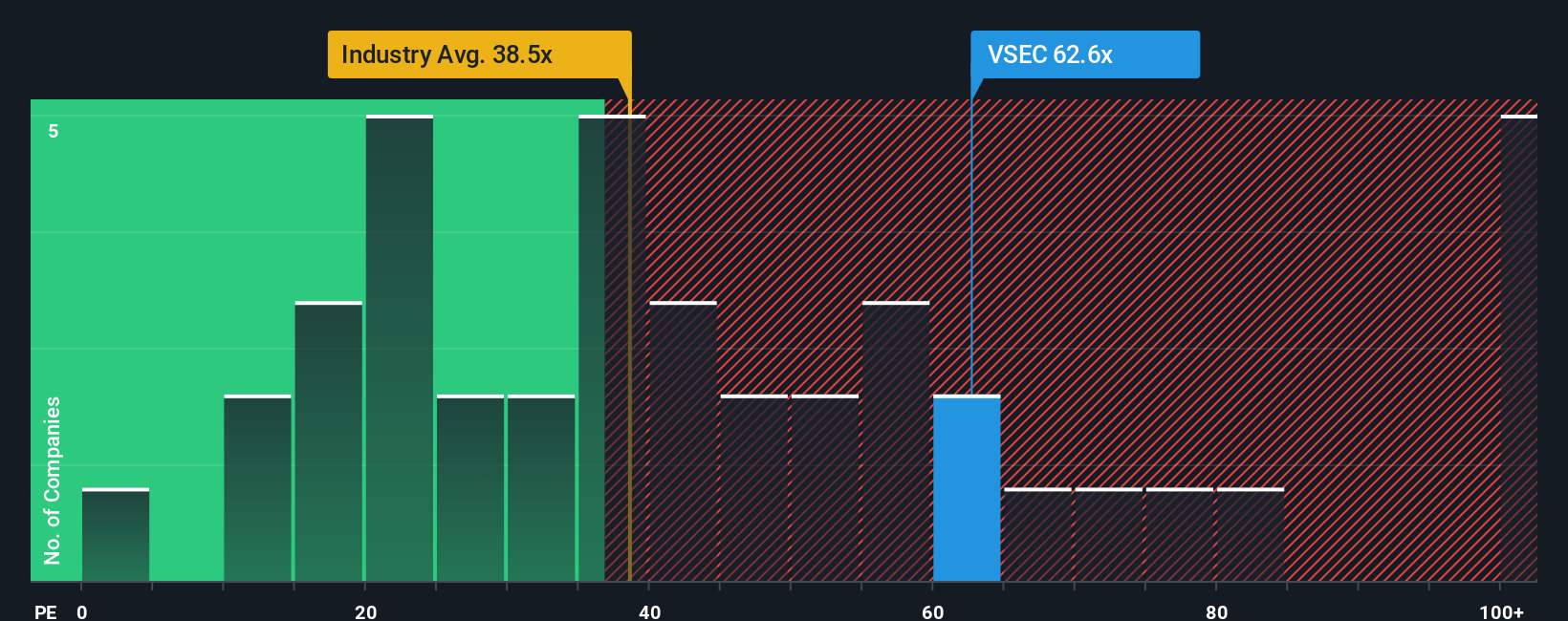

Currently, VSE is trading at a P/E ratio of 72x. This is well above both the aerospace and defense industry average of 38.4x and its listed peer average of 83.1x. While these benchmarks can offer useful context, they do not always provide the full picture since they lack nuance around company-specific factors.

This is where Simply Wall St's proprietary “Fair Ratio” comes in. Calculated from a blend of factors including VSE’s earnings growth prospects, profit margins, industry dynamics, company size, and unique risk profile, the Fair Ratio for VSE stands at 41.7x. This tailored approach offers investors a smarter benchmark than just the broad industry or peer comparison, helping you see where VSE should be valued given all it brings to the table.

Since VSE’s actual P/E of 72x is dramatically higher than its Fair Ratio of 41.7x, the evidence suggests the stock is overvalued when viewed through this lens.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1433 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your VSE Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is an investor’s own story or perspective about a company’s future, describing what you believe about its growth drivers, risks, strengths, and market conditions, then translating that into financial forecasts like fair value, future revenue, earnings, and margins.

With Narratives, you connect the dots between your understanding of VSE’s business and the numbers that underpin its value. This makes investing more accessible, as Narratives on Simply Wall St’s Community page let millions of investors build and share clear, transparent stories alongside their fair value estimate. You can see which assumptions drive each outlook and decide which one matches your own beliefs.

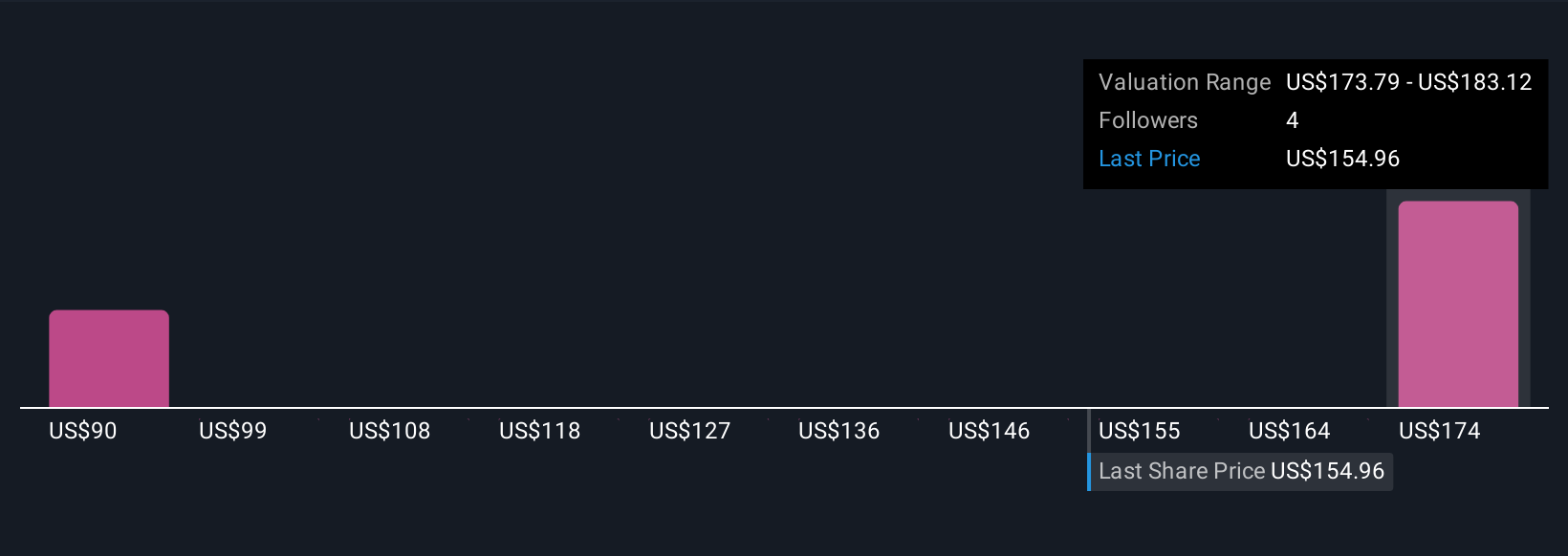

Narratives are especially powerful because they update automatically as new information, such as earnings releases or breaking news, is published, keeping your fair value aligned with the latest developments. For example, some investors may believe VSE’s profit margins will expand rapidly and set a fair value as high as $207 per share, while others might see competitive risks or slower growth and prefer a value closer to $142. This range of perspectives helps you decide whether VSE’s current price is attractive given your own expectations.

Do you think there's more to the story for VSE? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VSEC

VSE

Provides aviation aftermarket parts distribution and maintenance, repair, and overhaul services for air transportation assets for commercial and government markets.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

76 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

90 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

928 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative