Stock Analysis

- United States

- /

- Construction

- /

- NasdaqGS:STRL

Investors in Sterling Infrastructure (NASDAQ:STRL) have seen massive returns of 971% over the past five years

For many, the main point of investing in the stock market is to achieve spectacular returns. While the best companies are hard to find, but they can generate massive returns over long periods. Don't believe it? Then look at the Sterling Infrastructure, Inc. (NASDAQ:STRL) share price. It's 971% higher than it was five years ago. This just goes to show the value creation that some businesses can achieve. On top of that, the share price is up 57% in about a quarter. The company reported its financial results recently; you can catch up on the latest numbers by reading our company report. We love happy stories like this one. The company should be really proud of that performance!

Let's take a look at the underlying fundamentals over the longer term, and see if they've been consistent with shareholders returns.

View our latest analysis for Sterling Infrastructure

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

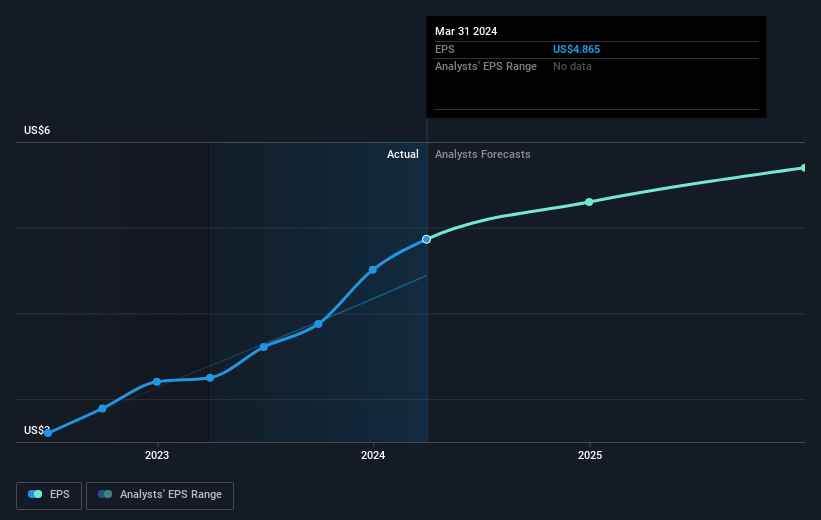

Over half a decade, Sterling Infrastructure managed to grow its earnings per share at 40% a year. This EPS growth is lower than the 61% average annual increase in the share price. This suggests that market participants hold the company in higher regard, these days. And that's hardly shocking given the track record of growth.

You can see below how EPS has changed over time (discover the exact values by clicking on the image).

It is of course excellent to see how Sterling Infrastructure has grown profits over the years, but the future is more important for shareholders. Take a more thorough look at Sterling Infrastructure's financial health with this free report on its balance sheet.

A Different Perspective

It's good to see that Sterling Infrastructure has rewarded shareholders with a total shareholder return of 189% in the last twelve months. That's better than the annualised return of 61% over half a decade, implying that the company is doing better recently. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider risks, for instance. Every company has them, and we've spotted 1 warning sign for Sterling Infrastructure you should know about.

But note: Sterling Infrastructure may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Valuation is complex, but we're helping make it simple.

Find out whether Sterling Infrastructure is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:STRL

Sterling Infrastructure

Engages in the provision of e-infrastructure, transportation, and building solutions primarily in the United States.

Outstanding track record with excellent balance sheet.