Advertisement

- United States

- /

- Machinery

- /

- NasdaqCM:LIQT

Is LiqTech International (NASDAQ:LIQT) Weighed On By Its Debt Load?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, LiqTech International, Inc. (NASDAQ:LIQT) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for LiqTech International

What Is LiqTech International's Net Debt?

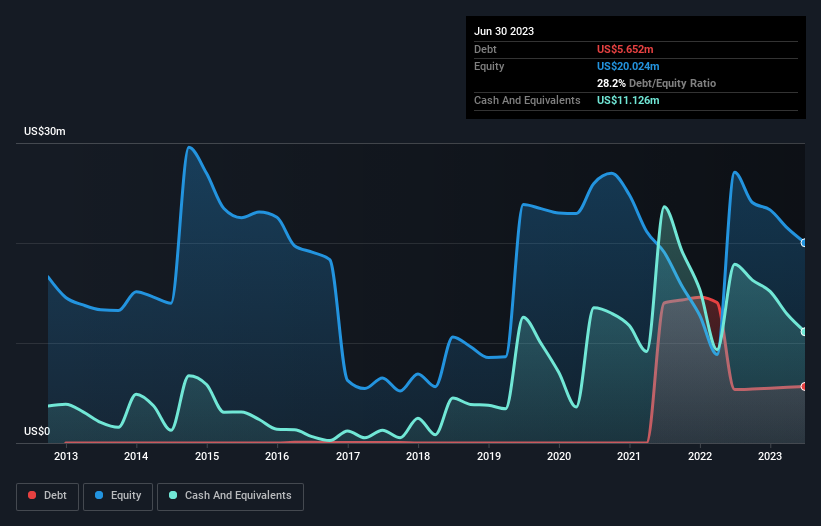

As you can see below, at the end of June 2023, LiqTech International had US$5.65m of debt, up from US$5.34m a year ago. Click the image for more detail. However, it does have US$11.1m in cash offsetting this, leading to net cash of US$5.47m.

How Healthy Is LiqTech International's Balance Sheet?

The latest balance sheet data shows that LiqTech International had liabilities of US$6.84m due within a year, and liabilities of US$10.5m falling due after that. Offsetting these obligations, it had cash of US$11.1m as well as receivables valued at US$5.37m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$804.8k.

Of course, LiqTech International has a market capitalization of US$20.0m, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. Despite its noteworthy liabilities, LiqTech International boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if LiqTech International can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, LiqTech International made a loss at the EBIT level, and saw its revenue drop to US$16m, which is a fall of 14%. That's not what we would hope to see.

So How Risky Is LiqTech International?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that LiqTech International had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through US$6.5m of cash and made a loss of US$7.9m. Given it only has net cash of US$5.47m, the company may need to raise more capital if it doesn't reach break-even soon. Summing up, we're a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 2 warning signs for LiqTech International that you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:LIQT

LiqTech International

A clean technology company, manufactures and markets specialized filtration products and systems in the Americas, the Asia-Pacific, Europe, the Middle East, and Africa.

Moderate risk with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor