Advertisement

- United States

- /

- Trade Distributors

- /

- NasdaqGS:DXPE

What DXP Enterprises (DXPE)'s Record Q3 Revenue Growth Reveals About Its Segment Strengths

Simply Wall St

Reviewed by Sasha Jovanovic

- DXP Enterprises recently reported record sales for the third quarter of 2025, achieving an 8.6% year-over-year revenue increase driven by strong performance in its Innovative Pumping Solutions segment, especially in energy and water-related projects.

- While the Supply Chain Services segment experienced a 5% decline in sales, the company’s ability to deliver record total revenue highlights the resilience of its diversified business model amid varying market conditions.

- We'll explore how robust growth in Innovative Pumping Solutions could influence DXP Enterprises' overall investment outlook and segment trends.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

DXP Enterprises Investment Narrative Recap

For shareholders in DXP Enterprises, the core thesis relies on the company's ability to leverage its diversified industrial distribution model, while the most important short-term catalyst remains ongoing strength in Innovative Pumping Solutions, especially in energy and water projects. The recent record Q3 sales, driven by this segment, reinforce the near-term growth story, but the 5% decline in Supply Chain Services highlights a key risk: inconsistent revenue from core segments. However, the impact of the latest results on short-term catalysts and risks appears modest, with the business still showing resilience despite mixed segment trends.

Among recent announcements, DXP’s August update on acquisition plans stands out amid the discussion of segment growth. With $219 million in liquidity and an aim to close multiple deals in the second half of 2025, management's focus on growth by acquisition complements momentum in Innovative Pumping Solutions, potentially enhancing long-term diversification yet also elevating integration and expense risks if targets underperform. That interplay makes segment performance and new business integration essential watchpoints for investors.

By contrast, investors should be aware that the resilience shown in this quarter does not eliminate concerns about uneven profitability caused by underperforming segments and rising expense pressures...

Read the full narrative on DXP Enterprises (it's free!)

DXP Enterprises' outlook anticipates $2.2 billion in revenue and $122.9 million in earnings by 2028. This is based on a projected annual revenue growth rate of 4.7% and a $36.3 million increase in earnings from the current $86.6 million.

Uncover how DXP Enterprises' forecasts yield a $136.50 fair value, a 58% upside to its current price.

Exploring Other Perspectives

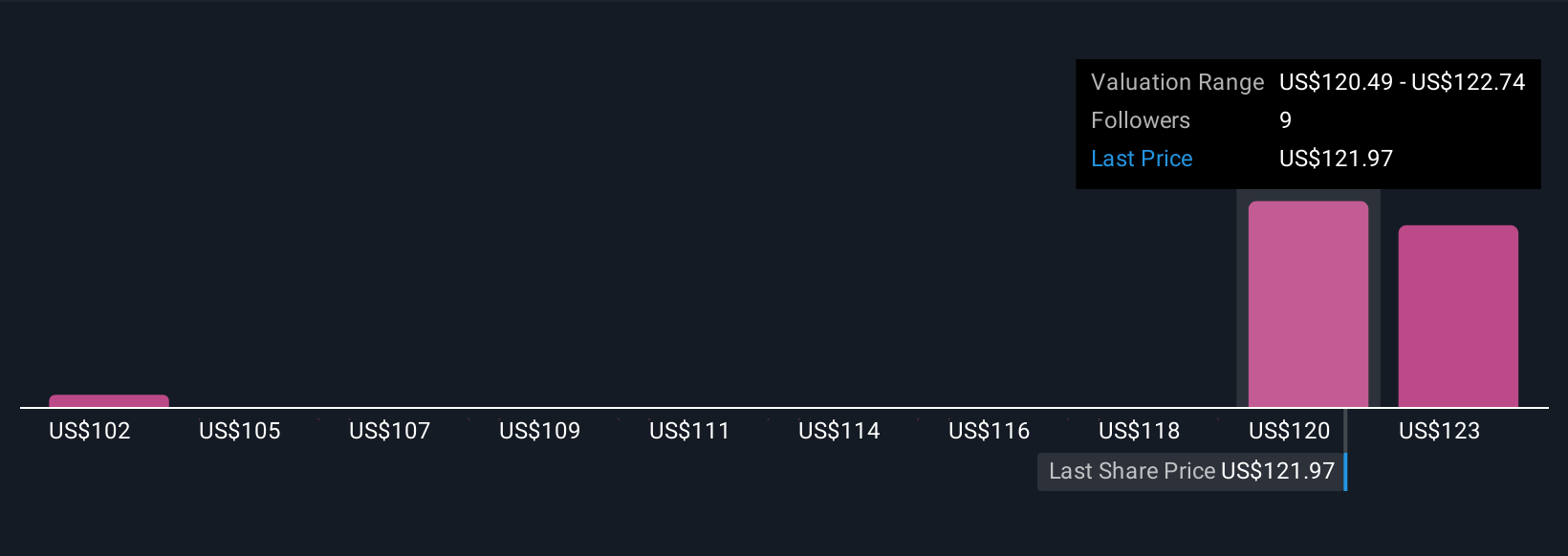

Simply Wall St Community members submitted 3 fair value targets for DXP Enterprises, ranging from US$102.44 to US$164.74 per share. These differing viewpoints reflect both optimism around segment growth and caution regarding profitability risk, inviting you to compare a spectrum of investor perspectives.

Explore 3 other fair value estimates on DXP Enterprises - why the stock might be worth just $102.44!

Build Your Own DXP Enterprises Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your DXP Enterprises research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free DXP Enterprises research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate DXP Enterprises' overall financial health at a glance.

Searching For A Fresh Perspective?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Find companies with promising cash flow potential yet trading below their fair value.

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DXPE

DXP Enterprises

Engages in distributing maintenance, repair, and operating (MRO) products, equipment, and services in the United States, Canada, and internationally.

Good value with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

80 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

91 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative